Bước sang tháng 7, giá trong chuỗi ngành công nghiệp vonfram vẫn ảm đạm. Một doanh nghiệp vonfram lớn đã hạ báo giá thu mua hợp đồng dài hạn trong nửa đầu tháng 7, trong khi Hiệp hội Vonfram Cám Châu đồng thời hạ giá dự báo trung bình tháng cho tất cả các loại sản phẩm vonfram, với tất cả các loại giá đều giảm so với tháng trước. Thị trường giao ngay cũng theo xu hướng đó và chịu áp lực. Theo báo giá của SMM, tinh quặng wolframit (≥65%) đã giảm yếu kể từ giữa đến cuối tháng 6. Nhìn lại diễn biến thị trường năm nay, giá vonfram đã trải qua những biến động dữ dội. So sánh hai chu kỳ giảm, mức giảm chung trong đợt điều chỉnh này bắt đầu từ giữa tháng 6 đã được thu hẹp so với đợt điều chỉnh đầu tiên từ tháng 3 đến tháng 5. Hiện tại, ảnh hưởng của mùa thấp điểm truyền thống rõ rệt. Các yếu tố như nhu cầu hạ nguồn yếu và tồn kho nguyên liệu chờ tiêu thụ tiếp tục đè nặng lên diễn biến giá vonfram; tuy nhiên, sự khan hiếm nguồn cung quặng cao cấp giá thấp sẽ hỗ trợ phần nào cho giá vonfram.

Giá Chào Hợp Đồng Dài Hạn Ngành và Giá Dự Báo Hàng Tháng Của Hiệp Hội Đều Giảm

Một doanh nghiệp vonfram đã hạ giá chào hợp đồng dài hạn trong nửa đầu tháng 7, như sau:

Theo Công ty TNHH Vonfram Chongyi Zhangyuan vào ngày 6 tháng 7, báo giá thu mua hợp đồng dài hạn nửa đầu tháng 7 là: 1. Tinh quặng wolframit 55%: 448.000 nhân dân tệ/tấn tiêu chuẩn (cơ sở 65% WO3), giảm 72.000 nhân dân tệ/tấn tiêu chuẩn so với kỳ báo giá trước; 2. Tinh quặng scheelit 55%: 447.000 nhân dân tệ/tấn tiêu chuẩn, giảm 72.000 nhân dân tệ/tấn tiêu chuẩn; 3. APT (Cấp GB 0): 660.000 nhân dân tệ/tấn, giảm 120.000 nhân dân tệ/tấn so với kỳ báo giá trước.

Hiệp hội Vonfram Cám Châu đã công bố giá dự báo trung bình tháng cho các sản phẩm vonfram tháng 7 năm 2026, với tinh quặng wolframit 55% ở mức 448.000 nhân dân tệ/tấn tiêu chuẩn, giảm 57.000 nhân dân tệ/tấn so với tháng 6; APT ở mức 660.000 nhân dân tệ/tấn, giảm 100.000 nhân dân tệ/tấn; và bột vonfram hạt trung bình ở mức 1.100 nhân dân tệ/kg, giảm 200 nhân dân tệ/kg.

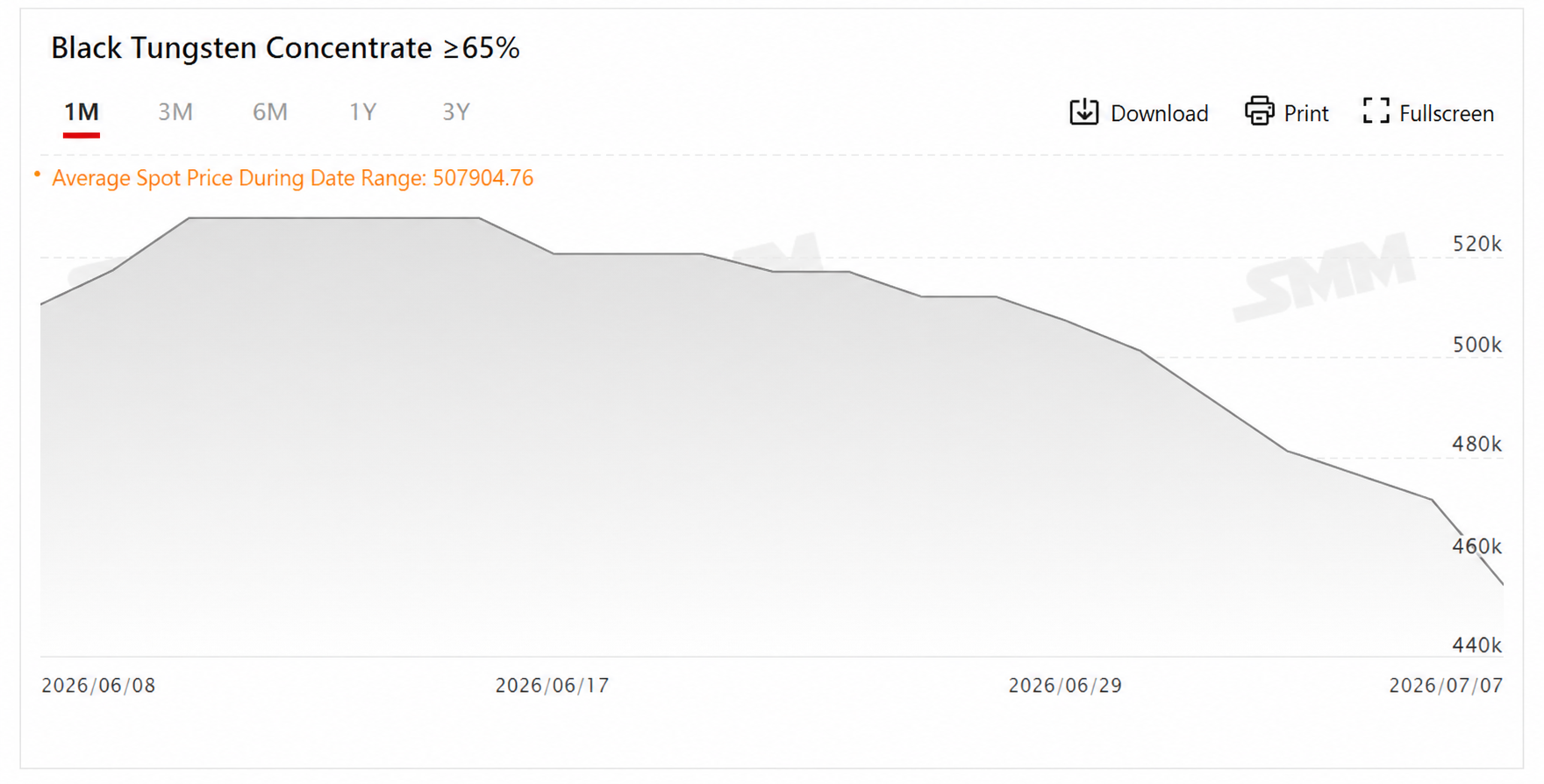

Tinh Quặng Wolframit Giảm 13,93% Trong Chưa Đầy Một Tháng

Theo báo giá của SMM, giá tinh quặng wolframit (≥65%) vào ngày 7 tháng 7 là 453.000-455.000 nhân dân tệ/tấn tiêu chuẩn, với giá trung bình 454.000 nhân dân tệ/tấn tiêu chuẩn, giảm 3,61% so với ngày giao dịch trước.

Nhìn lại xu hướng ngắn hạn, sau khi giá trung bình tinh quặng vonfram phục hồi lên mức cao trước đó là 527.500 nhân dân tệ/tấn tiêu chuẩn vào đầu đến giữa tháng 6, nhu cầu hạ nguồn yếu cùng với thực tế lượng tồn kho nguyên liệu thô tích tụ từ hoạt động tích trữ tập trung trước đó của các doanh nghiệp vẫn đang trong chu kỳ tiêu thụ đã làm suy yếu hỗ trợ thị trường, và giá vonfram bắt đầu điều chỉnh giảm nhẹ trên diện rộng từ ngày 17 tháng 6. So với giá trung bình 527.500 nhân dân tệ/tấn vào ngày 16 tháng 6, mức giá trung bình 454.000 nhân dân tệ/tấn vào ngày 7 tháng 7 thể hiện mức giảm 73.500 nhân dân tệ/tấn trong chưa đầy một tháng, tức giảm 13,93%.

Xét trong dài hạn, bước sang tháng 7, xu hướng giá trung bình của tinh quặng vonfram (≥65%) từ đầu năm đến nay đã như một chuyến tàu lượn siêu tốc đầy kịch tính. Được hỗ trợ bởi nguồn cung nguyên liệu thô thắt chặt vào đầu năm, tinh quặng vonfram (≥65%) khởi điểm ở mức 453.500 nhân dân tệ/tấn vào ngày 5 tháng 1, trước khi tăng vọt lên mức cao kỷ lục 1.050.500 nhân dân tệ/tấn vào ngày 13 tháng 3. Ở mức giá cao như vậy, tâm lý thận trọng và lo ngại giá cao trên thị trường dần gia tăng, cùng với mức chấp nhận hạn chế từ nhu cầu sử dụng cuối cùng, giá vonfram bắt đầu xu hướng giảm trên diện rộng, cuối cùng chạm mức thấp nhất trong năm là 400.500 nhân dân tệ/tấn vào ngày 25 tháng 5. Sau đợt điều chỉnh sâu trước đó, thị trường có nhu cầu phục hồi sau tình trạng bán quá mức. Cùng với sự bùng nổ tập trung của nhu cầu bổ sung hàng tồn kho theo giai đoạn, giá vonfram bắt đầu phục hồi từ ngày 27 tháng 5, tăng lên 527.500 nhân dân tệ/tấn vào ngày 10 tháng 6.

So sánh hai chu kỳ giảm giá hoàn chỉnh từ đầu năm đến nay cho thấy, đợt điều chỉnh đầu tiên sau cú tăng hồi đầu năm có biên độ dao động rộng hơn, trong khi đợt điều chỉnh hiện tại bắt đầu từ giữa tháng 6 có mức giảm tổng thể hẹp hơn so với đợt điều chỉnh trước. Tổng hợp các giai đoạn giá quan trọng, có thể thấy rõ thị trường tinh quặng vonfram năm nay đã trải qua những biến động mạnh với đặc điểm biến động rõ rệt.

Triển vọng

Nhìn về phía trước, trong ngắn hạn, tháng 7 đánh dấu thời điểm bắt đầu mùa tiêu thụ thấp điểm truyền thống của hạ nguồn. Nhu cầu mua hàng từ các doanh nghiệp cacbua xi măng và gia công cơ khí yếu, và nhu cầu thị trường ở mức trung bình yếu. Tuy nhiên, nguồn cung lưu thông quặng vonfram cao cấp tương đối khan hiếm. Với các yếu tố tăng và giảm giá kiềm chế lẫn nhau, giá vonfram được dự báo sẽ duy trì dao động đi ngang trong biên độ hẹp. Tiến độ cải thiện từ phía cầu hạ nguồn vẫn là trọng tâm theo dõi trong thời gian tới.

Trong trung và dài hạn, quy định trong nước về khai thác vonfram sơ cấp liên tục được siết chặt, nhu cầu cứng từ lĩnh vực cacbua xi măng hỗ trợ, quy mô xuất khẩu ròng sản phẩm vonfram tăng trưởng ổn định, tạo ra khoảng hụt cung-cầu kim loại vonfram trong cả năm. Trong quý 3, sự chưa phù hợp của chỉ tiêu khai thác sẽ tạo kỳ vọng thắt chặt nguồn cung nguyên liệu thô, trong khi "mùa cao điểm tháng 9-10" truyền thống sẽ thúc đẩy phục hồi nhu cầu bổ sung hàng tồn kho của doanh nghiệp. Đồng thời, nhu cầu cứng trong các lĩnh vực quân sự, thiết bị cao cấp và năng lượng mới tiếp tục mở rộng, chênh lệch giá giữa thị trường Trung Quốc và nước ngoài cũng sẽ liên tục thúc đẩy đơn hàng xuất khẩu. Nhiều yếu tố thuận lợi hỗ trợ mạnh mẽ cho phạm vi giá trung tâm trung và dài hạn của vonfram. Tuy nhiên, cần cảnh giác rủi ro thị trường tăng nhanh gây siết lợi nhuận của doanh nghiệp gia công hạ nguồn, dẫn tới cắt giảm sản lượng cuối cùng và phản hồi tiêu cực. Nhìn chung, thị trường vonfram được dự báo sẽ theo quỹ đạo tăng nhẹ nhàng và có trật tự sau đó.

Đọc thêm: