SMM News, July 7:

Metals market:

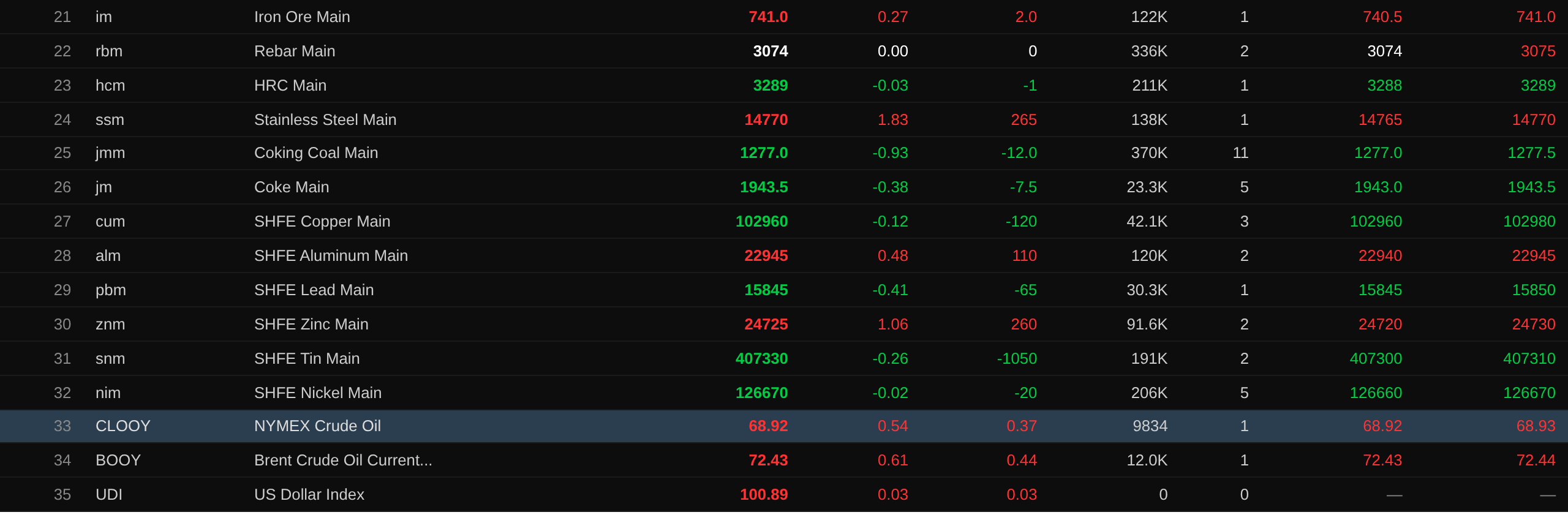

As of the midday close, base metals in the domestic market mostly fell, with SHFE copper down 0.12% and SHFE aluminum up 0.48%. SHFE lead fell 0.41%. SHFE zinc rose 1.06%. SHFE tin fell 0.26%. SHFE nickel fell 0.02%.

In addition, the most-traded casting aluminum futures contract rose 0.42%, while the most-traded alumina contract fell 0.44%. The most-traded lithium carbonate contract fell 2.22%. The most-traded silicon metal contract fell 0.24%. The most-traded polysilicon futures contract edged down.

Ferrous metals were mostly in the red. Iron ore rose 0.27%, rebar was flat at 3,074 yuan/mt, and hot-rolled coil edged down. Stainless steel rose 1.83%. For coking coal and coke: the most-traded coking coal contract fell 0.93%, and the most-traded coke contract fell 0.38%.

Overseas base metals: as of 11:42, LME metals mostly fell. LME copper fell 0.32%, LME aluminum rose 0.22%, and LME lead fell 0.19%. LME zinc rose 0.25%, LME tin fell 0.92%, and LME nickel fell 0.79%.

Precious metals: as of 11:42, COMEX gold fell 0.57% and COMEX silver fell 1.48%. Domestic precious metals: SHFE gold fell 0.83%, and the most-traded SHFE silver contract fell 2.3%.

In addition, as of the midday close, the most-traded platinum futures contract fell 1.72%, and the most-traded palladium futures contract fell 0.98%.

As of the midday close, the most-traded European shipping container futures contract extended the previous trading day’s decline, falling a further 5.03% to 2,446.5 points.

As of 11:42 on July 7, midday moves in some futures:

Spot and Fundamentals

Aluminum: Today, futures continued to rise, while spot in South China was under pressure and weaker. Yesterday, the spot-futures price spread briefly strengthened sharply, coupled with the absolute price rising for four consecutive sessions to a higher level. With both elevated, most suppliers actively sold to cash in, and price cuts became increasingly common; some chose to hold prices firm but with little effect. Mainstream quotations were at a discount of -10 to 0 yuan/mt, and circulation loosened...

Macro Front

China:

[World Bank Keeps Its 2026 China GDP Growth Forecast Unchanged] On July 7, the World Bank released the latest China Economic Update in Beijing. The report said that despite facing strong supply, weak demand, and shocks to global energy supplies, China’s economic growth overall maintained resilience, and China’s economic growth in 2026 is expected to be 4.4%. Compared with the previous update released in December last year, the growth forecast remained unchanged. (Xinhua News Agency)

[PBOC Reverse Repo Operations Resulted in a Net Drain of 59.5 billion yuan on the Day] Today, the PBOC conducted 10 billion yuan of 7-day reverse repo operations. As 69.5 billion yuan of 7-day reverse repos matured today, it resulted in a net drain of 59.5 billion yuan on the day. (Jinshi Data APP)

[John Lee: Hong Kong’s Gold Central Clearing System Begins Trial Operation Today; New RMB-Denominated Gold Futures Contracts Under Consideration] On July 7, John Lee announced that Hong Kong’s Gold Central Clearing System began trial operation today and that the development of new RMB-denominated gold futures contracts is under consideration. Hong Kong Exchanges and Clearing Limited will sign a memorandum of understanding with the PBOC on cross-border RMB payment and clearing. The Hong Kong gold market saw a critical upgrade at the infrastructure level, with the gold clearing and settlement system officially launched on July 7. To support the new system and simultaneously invigorate the local gold futures market, HKEX announced a one-year fee waiver for gold futures, effective from July 7. (Wall Street CN) 》Click for details

On the US dollar front:

As of 11:42, the US dollar index rose 0.03% to 100.89. Fed Governor Waller stated that the US Fed would not deliberately maintain low interest rates to help the US government finance its fiscal deficit. Waller noted that the US labor market had stabilized, while inflation had re-accelerated, meaning the risk from inflation now exceeds the risk to employment—a complete reversal from policy considerations a year ago. He pointed out that while he supported an interest rate cut last year due to labor market weakness, the policy focus should now shift back toward curbing inflation. The market’s attention has turned to the June CPI, due on July 14, the last critical inflation data before the Fed’s July 28-29 meeting. Although international oil prices have pulled back to around $70/barrel, Fed officials still expect inflation to be significantly above the 2% target at year-end. According to the CME "FedWatch" tool: The probability of the US Fed maintaining the current interest rate in July is 74.3%, while the probability of a cumulative 25-basis-point rate hike is 25.7%. For September, the probability of the rate remaining unchanged is 42.9%, the probability of a cumulative 25-basis-point hike is 46.2%, and the probability of a cumulative 50-basis-point hike is 10.8%. (Jinshi Data APP)

The US ISM Services PMI report showed that economic activity in the services sector continued to expand in June. The Services PMI registered 54, marking the 24th consecutive month in expansion territory. Miller, Chair of the ISM Services Business Survey Committee, stated that the June Services PMI of 54 was down 0.5 from May’s 54.5. The Business Activity Index remained in expansion territory, falling 2.3 from May’s 57.7 to 55.4. The Prices Index dropped to 67.7 in June, a decrease of 3.6 from May’s 71.3, falling below 70 for the first time since February. The index has been above 60 for 19 consecutive months, with a 12-month average of 68. Diesel, gasoline, oil and related commodities were again cited as the items with the largest price increases in June, but some respondents also reported price declines. This may stem from differences in contract terms for these commodities across companies. Some respondents noted declines in payments for gasoline and diesel, but this was not a widespread phenomenon. We expect this situation to persist for several months as rising oil prices feed through supply chains, but assuming the recent progress in oil shipments through the Strait of Hormuz continues, there should be some relief by autumn. (Jin10 Data APP)

Other Currencies:

Japan’s Minister of State for Economic and Fiscal Policy, Shironai Minoru, said media reports suggesting Prime Minister Takaichi Sanae’s government was trying to steer interest rates lower were completely inaccurate. Speaking at a regular press conference in Tokyo on Tuesday, Shironai said, “Reports that the government would encourage low interest rates as part of its fiscal expansion policies are groundless. If our intentions are not being accurately conveyed, we will work harder to foster understanding.” His remarks came as financial markets closely watch how Takaichi Sanae will implement her economic strategy through massive investment without adding to the already heavy debt burden. Shironai attended a Bank of Japan board meeting last month as a government representative, where policymakers raised the benchmark interest rate to 1%, the highest in 31 years. (Jin10 Data APP)

Data:

Today will see the release of Germany’s seasonally adjusted industrial output MoM for May, the UK Halifax seasonally adjusted house price index MoM for June, France’s trade balance for May, the weekly change in US ADP employment for the week ending June 20, the US trade balance for May, and China’s foreign exchange reserves for June, among others. Additionally, attention should be paid to: Turkey hosts the NATO summit through July 8; the US Trade Representative’s office holds public hearings on a proposal to impose additional tariffs on 60 global economies; Samsung Electronics will release its Q2 earnings guidance.

Crude Oil:

As of 11:42, both benchmark crude prices rose, with WTI up 0.54% and Brent up 0.61%. The brief window of US-Iran easing once again faces rupture, pushing oil prices higher. Markets are watching geopolitical developments and supply-demand outlook changes.

The number of vessels transiting the Strait of Hormuz continues to rebound. According to reports, a total of 160 vessels passed through the strait from Monday to Saturday last week, though the overall level remains far below pre-war norms. (Wall Street CN)

As a surge in global supply intensifies competition for buyers, Saudi Arabia cut the official selling prices of its main crude grades for Asian customers for August by the most in at least 26 years. According to a price list, Saudi Aramco slashed the price of Arab Light crude for Asia for August by $11 per barrel, to a discount of $1.50 per barrel against the regional benchmark. The cut was larger than the $8 per barrel expected in a survey of institutions. Crude oil prices in the Middle East have recently declined. After resuming exports from the Ras Tanura port in the Persian Gulf, Saudi Aramco temporarily raised crude oil shipments to approximately 90% of pre-war levels. Before the war, Ras Tanura was the main loading port for Saudi crude oil exports. As the war blocked the Strait of Hormuz, Saudi Aramco diverted most of its crude oil flows to the Yanbu port on the Red Sea. Previously, the OPEC+ producer group agreed to continue with a small production increase in August. Now, with shipping resuming in the Strait of Hormuz, Gulf oil producers such as Saudi Arabia, Iraq and Kuwait will be able to utilize their higher quotas. (Jinshi Data APP)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

►

![Tight Available Supply in the Market, Spot Premiums Rise [SMM Yangshan Copper Spot]](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)

![US Fed "Dovish" Governor's Stance Turns "Hawkish"; Most-Traded SHFE Tin Contract Consolidates at Highs with a Weakening Center [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/SkvFp20251217171752.jpg)

![Guangdong Zinc: Downstream Purchase Willingness Low, Spot Premiums Decline [SMM Midday Review]](https://imgqn.smm.cn/usercenter/Txorc20251217171755.jpg)