Recently, China's lead prices have continued to weaken. Secondary smelters have been broadly trapped in a dual predicament of production losses and a shortage of scrap battery raw materials. SMM's statistics on production cuts and resumption plans at secondary lead enterprises across the country in June–July clearly reflect the current pressure on the industry.

I. Secondary Lead in June: Notable Divergence Among Enterprises, Overall Slight MoM Increase

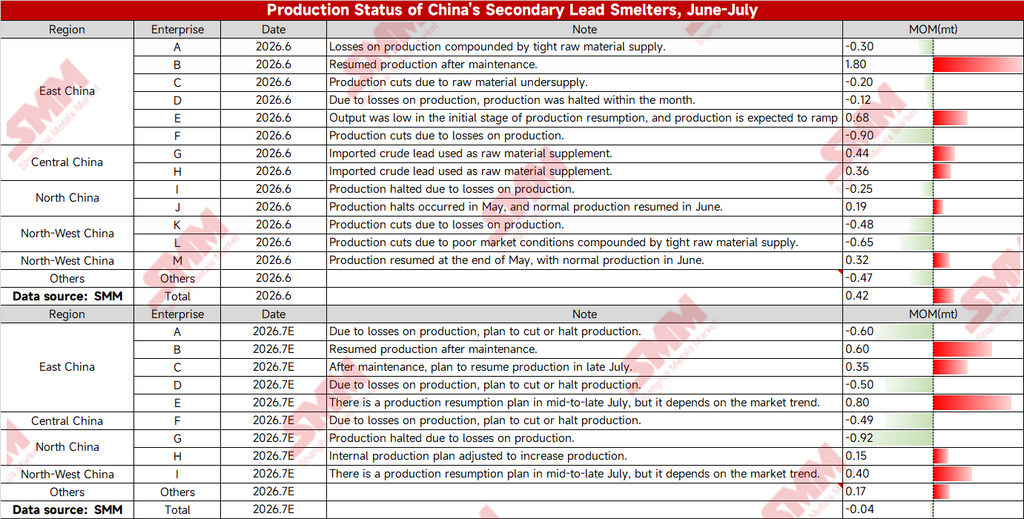

In June 2026, smelters across regions were polarized:

1. Core logic behind production cuts: Multiple enterprises, including East China A/C/D/F, North China I, and South China K/L, proactively reduced loads or halted production due to production losses caused by falling lead prices and insufficient recycling volumes of scrap batteries. The maximum reduction at a single plant reached 9,000 mt; scattered enterprises in other regions together further reduced production by 4,700 mt.

2. Offsetting increase from production resumptions: East China B/E, Central China G/H, North China J, and Northwest M completed maintenance and resumed production, and raised output by supplementing feedstock with imported crude lead, forming an offsetting increase.

After netting out increases and decreases, China’s secondary refined lead output edged up by 4,200 mt MoM in June, still providing some supply-side support.

II. July Expectations: Losses Worsen, Supply Increase Essentially Vanishes

As July begins (Expected E), the industry’s loss-making situation is expected to widen further, and production cuts will intensify significantly:

1. Extensive planned production cuts: Multiple smelters including East China A/D, Central China F, and North China G have clearly planned to concentrate production cuts due to market losses. The reduction at a single North China plant reached 9,200 mt, a scale far exceeding that of June. Some enterprises have production resumption plans for mid-to-late July, but all indicated they need to monitor lead price trends, leaving the pace of resumption uncertain.

2. Limited increase from resumptions: Only a few enterprises, such as East China B/C, Northwest I, and North China H, resumed production after maintenance and lifted output through internal production adjustments, with the increase insufficient to cover the reduction gap.

For the full month, July secondary refined lead output is expected to edge down by just 400 mt MoM. The supply side will thus shift from a slight MoM increase in June to basically flat, as the increase is completely offset by production cuts driven by losses.

III. Interpretation in the Context of the Current Lead Market

The core contradiction in the current lead market is centered on ample primary lead supply and weak downstream battery demand in the off-season, causing lead prices to fall under sustained pressure and directly squeezing the processing margins of secondary lead plants: The purchase price of scrap batteries remains stubbornly high, the selling price of refined lead is weakening, and smelters’ processing fees are inverted, so voluntarily cutting production to avoid risks has become a common choice;

On the raw material side, the recycling volume of scrap batteries is already at a seasonal low during the off-season, and losses further weaken enterprises' willingness to purchase raw materials, forming a negative cycle of “price decline → less procurement → production cuts”;

In July, although some maintenance-related production resumptions are scheduled, the willingness of enterprises to resume production highly depends on a recovery in lead prices. If the market remains sluggish, the original production resumption plans may be postponed, and subsequently secondary lead supply is expected to tighten further, potentially providing bottom support for lead prices.

![SHFE lead ends slightly higher intraday, short-term rebound strength needs to watch downstream destocking realization [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/xVgcv20251217171721.jpg)