Recentemente, os preços do chumbo na China continuaram a enfraquecer, com as fundições secundárias geralmente enfrentando um duplo dilema de perdas de processamento e escassez de matérias-primas de baterias usadas. A pesquisa da SMM sobre cortes de produção e planos de retomada nas fundições secundárias de chumbo em todo o país, de junho a julho, reflete claramente a pressão atual sobre o setor.

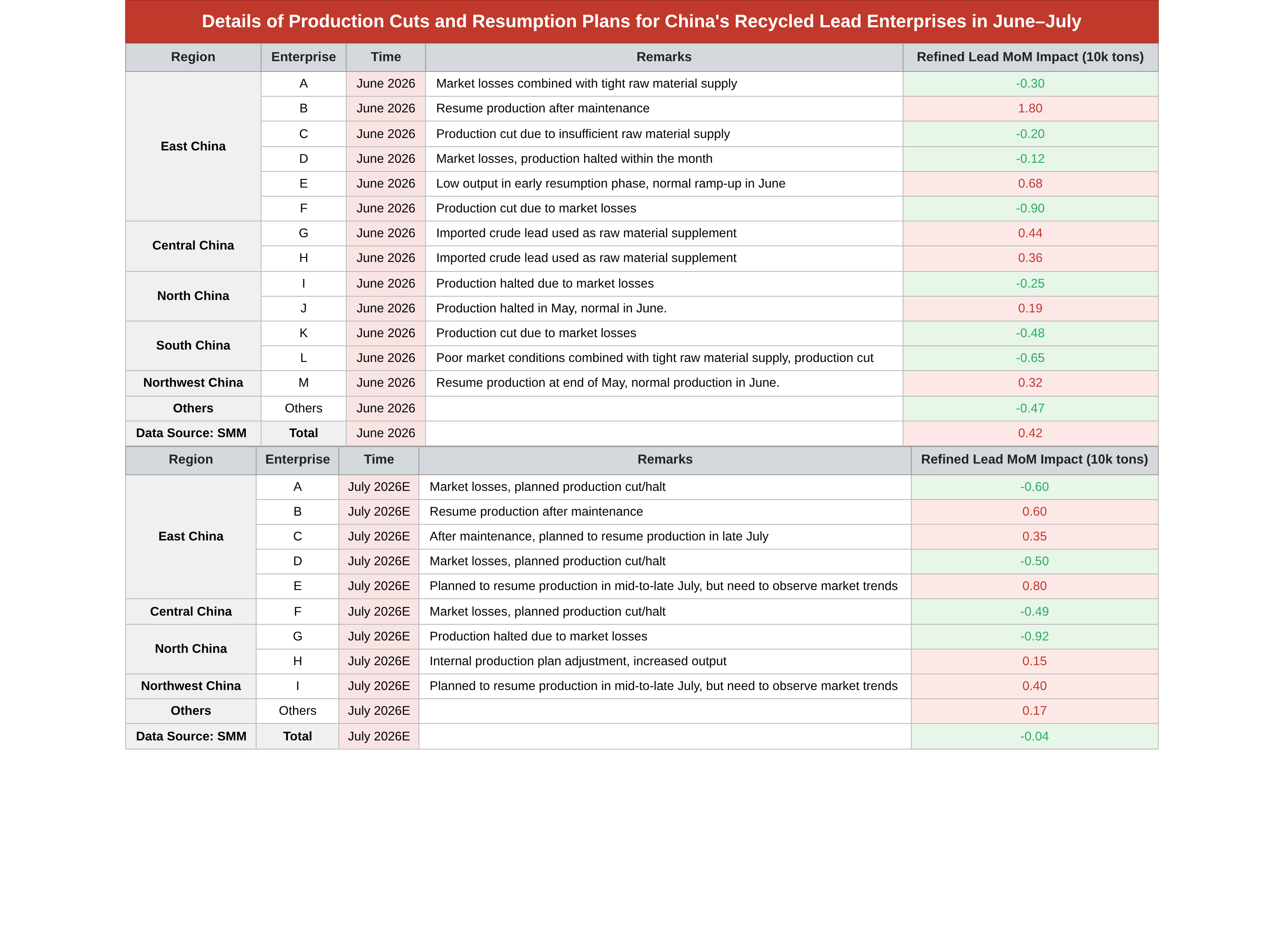

I. Chumbo Secundário em Junho: Significativa polarização entre empresas, leve aumento geral

Em junho de 2026, as operações das fundições em todas as regiões se polarizaram:

Lógica central dos cortes de produção: Várias empresas no leste da China (A/C/D/F), norte da China (I) e sul da China (K/L) reduziram proativamente a carga ou suspenderam a produção devido à queda dos preços do chumbo, o que causou perdas na produção, e volumes insuficientes de reciclagem de baterias usadas. Uma única fundição nessas áreas reduziu a produção em até 9.000 toneladas métricas; outras empresas dispersas em outras regiões cortaram mais 4.700 toneladas métricas.

Aumento compensado pelas retomadas de produção: Fundições no leste da China (B/E), centro da China (G/H), norte da China (J) e noroeste da China (M) retomaram a produção após manutenção e aumentaram a produção usando chumbo bruto importado como matéria-prima, formando um aumento compensatório. Após combinar aumentos e reduções, a produção nacional de chumbo refinado secundário em junho aumentou marginalmente em 4.200 toneladas métricas MoM, com a oferta ainda tendo algum suporte.

II. Expectativas para Julho: Perdas se aprofundam, aumento da oferta praticamente desaparece

Ao entrar em julho (estimativa E), o escopo de prejuízo do setor se expandiu ainda mais, e a magnitude dos cortes de produção aumentou significativamente:

Cortes de produção planejados em grande escala: Várias fundições no leste da China (A/D), centro da China (F) e norte da China (G) planejaram explicitamente concentrar cortes de produção devido a perdas de mercado, com uma única fundição no norte da China reduzindo a produção em 9.200 toneladas métricas – uma escala que excede em muito a de junho. Embora algumas empresas tenham planos de retomada de produção para meados ou final de julho, todas indicaram que precisam observar as tendências dos preços do chumbo, tornando o ritmo das retomadas incerto.

Aumento limitado das retomadas de produção: Apenas algumas empresas no leste da China (B/C), noroeste da China (I) e norte da China (H) retomaram a produção após manutenção ou ajustaram a produção interna para aumentar os volumes, com o aumento incapaz de cobrir a lacuna dos cortes de produção. Estimativas gerais para o mês completo indicam que o chumbo secundário refinado em julho recuará apenas 400 mt em relação ao mês anterior, passando de um leve aumento em junho para estabilidade, uma vez que o aumento é totalmente compensado pelos cortes de produção motivados por prejuízos.

III. Interpretação no contexto atual do mercado de chumbo

A contradição central atual no mercado de chumbo concentra-se na oferta abundante de chumbo primário + fraca demanda por baterias no setor downstream durante o período de baixa temporada, o que manteve os preços do chumbo sob pressão de queda, comprimindo diretamente as margens de processamento das fundições de chumbo secundário:

1. Os preços de compra de baterias inservíveis permanecem rígidos e difíceis de cair, enquanto os preços de venda do chumbo refinado enfraquecem, levando a tarifas de tratamento (TCs) negativas para as fundições. Cortes de produção proativos para evitar riscos tornaram-se uma escolha comum.

2. Do lado da matéria-prima, os volumes de reciclagem de baterias inservíveis já se encontram em mínimas de baixa temporada, e os prejuízos reduzem ainda mais a disposição das empresas em adquirir materiais, formando um ciclo negativo de "queda de preço → menor coleta de material → cortes de produção".

3. Embora algumas retomadas de produção relacionadas à manutenção estejam programadas para julho, a disposição para retomar depende fortemente de uma recuperação nos preços do chumbo. Caso o mercado permaneça lento, as retomadas originalmente planejadas poderão ser adiadas, e as expectativas de um maior aperto na oferta de chumbo secundário fornecerão um suporte para os preços do metal.

![Demanda do mercado de baterias de chumbo-ácido está fraca, algumas empresas do setor interrompem a produção para recesso de altas temperaturas [SMM – Comentário Semanal da Taxa de Operação de Baterias de Chumbo-Ácido]](https://imgqn.smm.cn/usercenter/guTSZ20251217171722.jpg)

![Fornecedores Ampliaram Descontos para Desovar Mercadorias no Fim do Mês, Transações no Mercado à Vista Lentas [Revisão Semanal do Mercado à Vista de Chumbo Refinado SMM]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![Taxa Semanal de Operação das Fundições de Chumbo Primário SMM (17 de julho a 23 de julho de 2026) [Revisão Semanal de Fundição de Chumbo Primário SMM]](https://imgqn.smm.cn/usercenter/mfCMp20251217171721.jpeg)