SMM Jul. 6 News:

Metals Market Update:

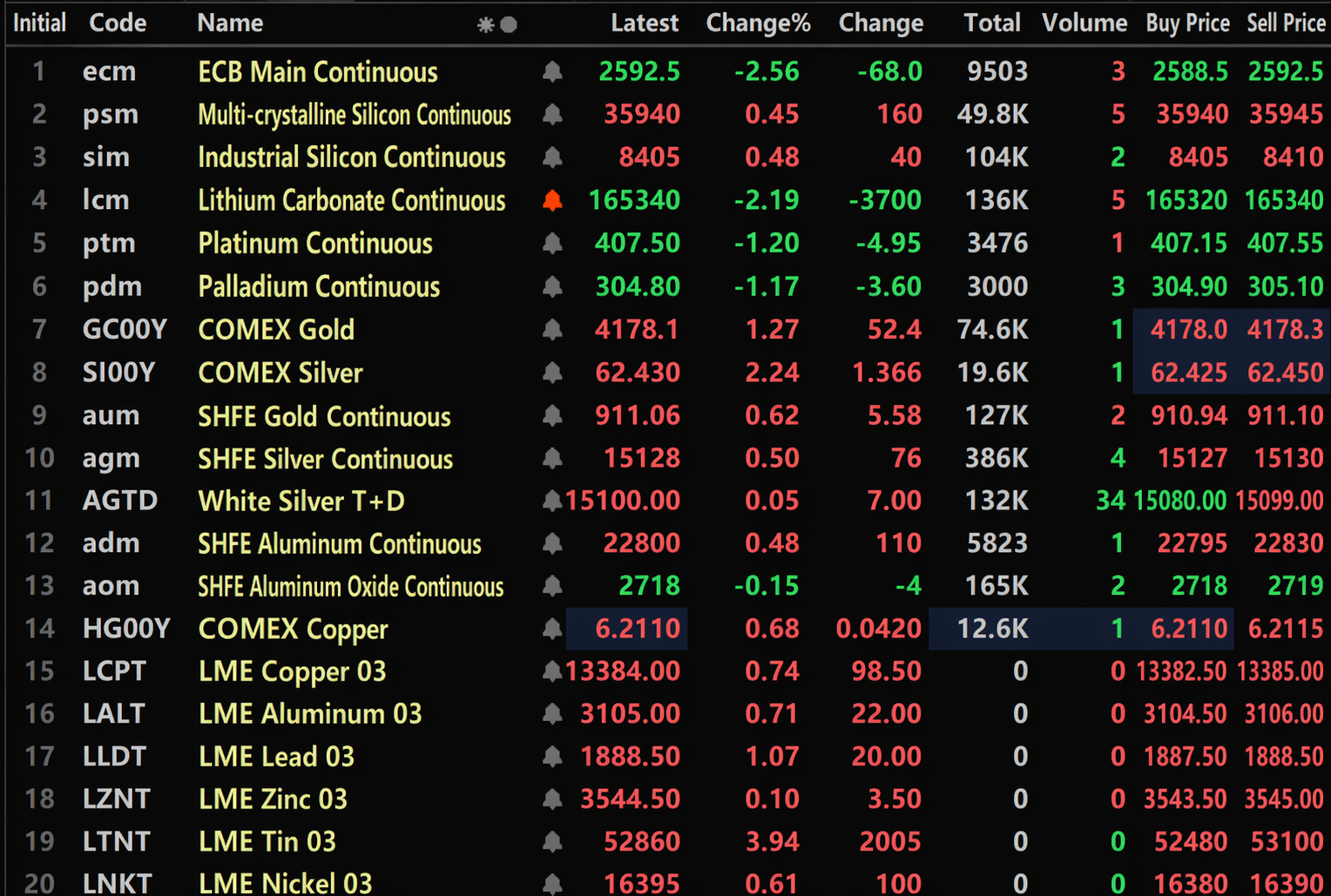

As of the midday close, base metals on the domestic market all rose. SHFE copper edged up 0.26%, SHFE aluminum gained 0.84%. SHFE lead ticked higher. SHFE zinc added 0.97%. SHFE tin surged 2.9%. SHFE nickel inched up 0.12%.

In addition, the most-traded foundry aluminum futures contract rose 0.48%, while the most-traded alumina contract dipped 0.15%. The most-traded lithium carbonate contract fell 2.19%. The most-traded silicon metal contract climbed 0.48%. The most-traded polysilicon futures contract gained 0.45%.

Ferrous metals all advanced. Iron ore, HRC, and rebar each rose within 0.5%. Stainless steel added 0.89%. Coking coal and coke: the most-traded coking coal contract increased 0.82%, and the most-traded coke contract rose 1.06%.

Overseas base metals: as of 11:45, LME metals all advanced. LME copper gained 0.74%, LME aluminum rose 0.71%, LME lead climbed 1.07%. LME zinc ticked up 0.1%, LME tin surged 3.94%. LME nickel added 0.61%.

Precious metals: as of 11:45, COMEX gold advanced 1.27%, and COMEX silver jumped 2.24%. Domestic precious metals: SHFE gold rose 0.62%; the most-traded SHFE silver contract gained 0.5%.

In addition, as of the midday close, the most-traded platinum futures contract fell 1.2%, while the most-traded palladium futures contract dropped 1.17%.

As of the midday close, the most-traded container freight index (Europe) futures contract slid 2.56% to 2,592.5 points.

As of 11:45 on Jul. 6, select futures midday quotes:

Spot and Fundamentals

Nickel: On Jul. 6, SMM #1 refined nickel price declined 750 yuan/mt from the previous trading day. For spot premiums, the average premium for Jinchuan #1 refined nickel stood at 2,300 yuan/mt, up 50 yuan/mt from the prior day DoD...

Macro Front

China:

[PBOC Reverse Repo Operation Results in Net Injection of 49.5 Billion Yuan] The PBOC conducted 7 billion yuan in 7-day reverse repos and 1,000 billion yuan in outright reverse repos today. With 157.5 billion yuan in 7-day reverse repos and 800 billion yuan in outright reverse repos maturing, the day saw a net injection of 49.5 billion yuan. (Jinshi Data APP)

[Guangzhou Baiyun International Airport’s Foreign Visitor Arrivals, Share Hit Record Highs] As of 0:00 on Jul. 6, Baiyun Port station of the Guangzhou General Station of Immigration Inspection reported over 4 million foreign entries and exits at Guangzhou Baiyun International Airport this year, up 34% YoY and accounting for over 41% of the airport’s total passenger flow. The growth rate topped the national average by 8 percentage points, with both volume and share reaching record highs. Overall, the port has handled over 10 million inbound and outbound passenger trips, up 19.6% YoY, crossing the 10 million mark 34 days earlier than in 2025. Inbound and outbound flights exceeded 63,000, up 14% YoY. (CCTV News)

US dollar:

As of 11:45, the US dollar index was up 0.09% at 100.95. According to the CME FedWatch Tool, the probability that the US Fed holds rates steady in July is 77%, while the probability of a cumulative 25bp hike is 23%. For September, the probability of no change is 41.9%, a cumulative 25bp hike 47.6%, and a cumulative 50bp hike 10.5%.

Goncalves George, head of US macro strategy at Mitsubishi UFJ Securities Americas, said Warsh’s concise style gives the June meeting minutes greater weight than usual and offers a valuable lens into the differing stances among Fed officials. “The minutes will become more important because, so far, we don’t know what the Fed is thinking,” Goncalves George said. “It will be instructive to see how they debate and what they focus on.” He added that some investors have already questioned Warsh’s hands-off approach, and many would like to see greater transparency restored. Many market participants are not accustomed to the reduced flow of information, and there remains a considerable degree of skepticism over how long the Fed can maintain this. For now, we have to read between the lines.

In a research note, Wan Michael, senior FX analyst at Mitsubishi UFJ Bank, said markets appear to be in a wait-and-see mode, looking for the next catalyst for the US dollar and US interest rates. Looking ahead, “global markets will seek direction from key data points such as the US ISM services data and Fed minutes later this week, and US CPI next week,” he said. In addition, the market is also closely watching whether Japanese authorities intervened in the currency market last week to curb yen weakness, so this uncertainty risk should not be underestimated as USD/JPY continues to hover near the 162 level. (Jin10 Data APP)

Other currencies:

As imports surge while export growth stalls, the boost from the mining boom to Australia’s trade appears to be fading, and the country may face its first annual trade deficit since 2016. This year, the goods trade surplus has narrowed sharply as the data center construction boom drives a surge in imports of fuel and equipment, while exports have stagnated. This trend appears set to continue, with the Australian government forecasting that export revenue from key commodities will grow only 3% in the current fiscal year compared with the previous one. The mining investment boom drove a surge in exports of iron ore, natural gas, and other commodities, fueling years of economic expansion and wealth accumulation. A return to deficits, however, could weigh on the Australian dollar and constrain the government’s fiscal space. Economist James McIntyre said, “Commodity price declines are expected to weigh on export revenues. As a result, the trade surpluses and occasional current account surpluses recorded over the past decade may give way to a pattern of deficits.” (Jin10 Data App)

Data:

Today, the seasonally adjusted unemployment rates for France and Switzerland in June, the eurozone July Sentix Investor Confidence Index, the eurozone May PPI monthly rate, the eurozone May retail sales monthly rate, the US June S&P Global Services PMI final, the US June ISM Non-Manufacturing PMI, and the US June Global Supply Chain Pressure Index, among other data, will be released. Additionally, speeches are expected from Fed Governor Waller, ECB Executive Board member Schnabel, ECB Governing Council member Wunsch, and Riksbank Deputy Governor Seim.

Crude Oil:

As of 11:45, oil prices on both exchanges fell, with WTI down 0.38% and Brent down 0.57%.

Oil prices were weighed down by OPEC+’s latest decision to raise output. After an online meeting on Sunday, the group said it would increase output by about 188,000 barrels per day in August, marking the fifth consecutive monthly increase. However, analysts at ANZ Research said in a note, “Even if the Strait of Hormuz reopens, members may struggle to utilize this additional capacity due to ongoing risks to vessels.” The analysts noted, “During the weekend, multiple vessels were observed making abrupt course reversals while attempting to transit the Strait of Hormuz along the Oman route.” (Jin10 Data App)

A statement showed that OPEC+ will raise oil production quotas by 188,000 barrels per day in August. The seven core members of OPEC+, which comprises OPEC and allies including Russia, have collectively raised production quotas by nearly 800,000 barrels per day from April to July. However, because the US-Israeli war on Iran has closed the Strait of Hormuz to oil tanker shipments for some of the most important OPEC+ members, including Saudi Arabia, Kuwait, and Iraq, previous increases have largely remained on paper. (Jin10 Data App)

According to agency reports, the number of vessels transiting the channel along the Omani coast of the Strait of Hormuz dropped sharply on Sunday. A day earlier, multiple vessels sailing out of the strait along that channel abruptly executed sharp course reversals, underscoring Iran’s ongoing tightening of control over this strategic waterway. A product tanker that turned around on Saturday appears to be attempting passage again, having passed the northernmost point of Oman’s Musandam Peninsula. Earlier, another product tanker transited the same route and publicly broadcast its voyage intention, and is now broadcasting its position in the Gulf of Oman. Some vessels opted for “dark transit” through the strait. A Suezmax crude oil tanker that last broadcast its position in the Persian Gulf on Saturday appeared in the Gulf of Oman on Sunday. Between Friday and Saturday, at least eight vessels suddenly turned around while transiting the Strait of Hormuz along the Omani shipping lane. Four of them subsequently altered course northward, departing the strait via the Iranian side lane. There is no official explanation for the sudden U-turns. However, Iran has repeatedly stated that vessels can only transit the Strait of Hormuz through lanes designated and authorized by Iran. According to Kpler data, a total of 19 vessels transited the Strait of Hormuz in both directions on Saturday, but only one publicly indicated its intention to enter the strait via the Omani coastal lane, compared with 13 on Friday. The tally only covers observable vessel movements. (Jinshi Data APP)

Spot market roundup:

►

►

►

►

►

►

►

►

►

►

![Inventory destocking coupled with demand resilience, Shanghai spot copper premiums strengthen steadily [SMM Shanghai spot copper]](https://imgqn.smm.cn/usercenter/HAuaN20251217171710.jpg)

![SHFE Aluminum Rises for Three Consecutive Days, Spot Aluminum Strong and Firm [SMM South China Aluminum Spot Daily Review]](https://imgqn.smm.cn/usercenter/TFHUe20251217171651.jpg)