SMM News, July 3:

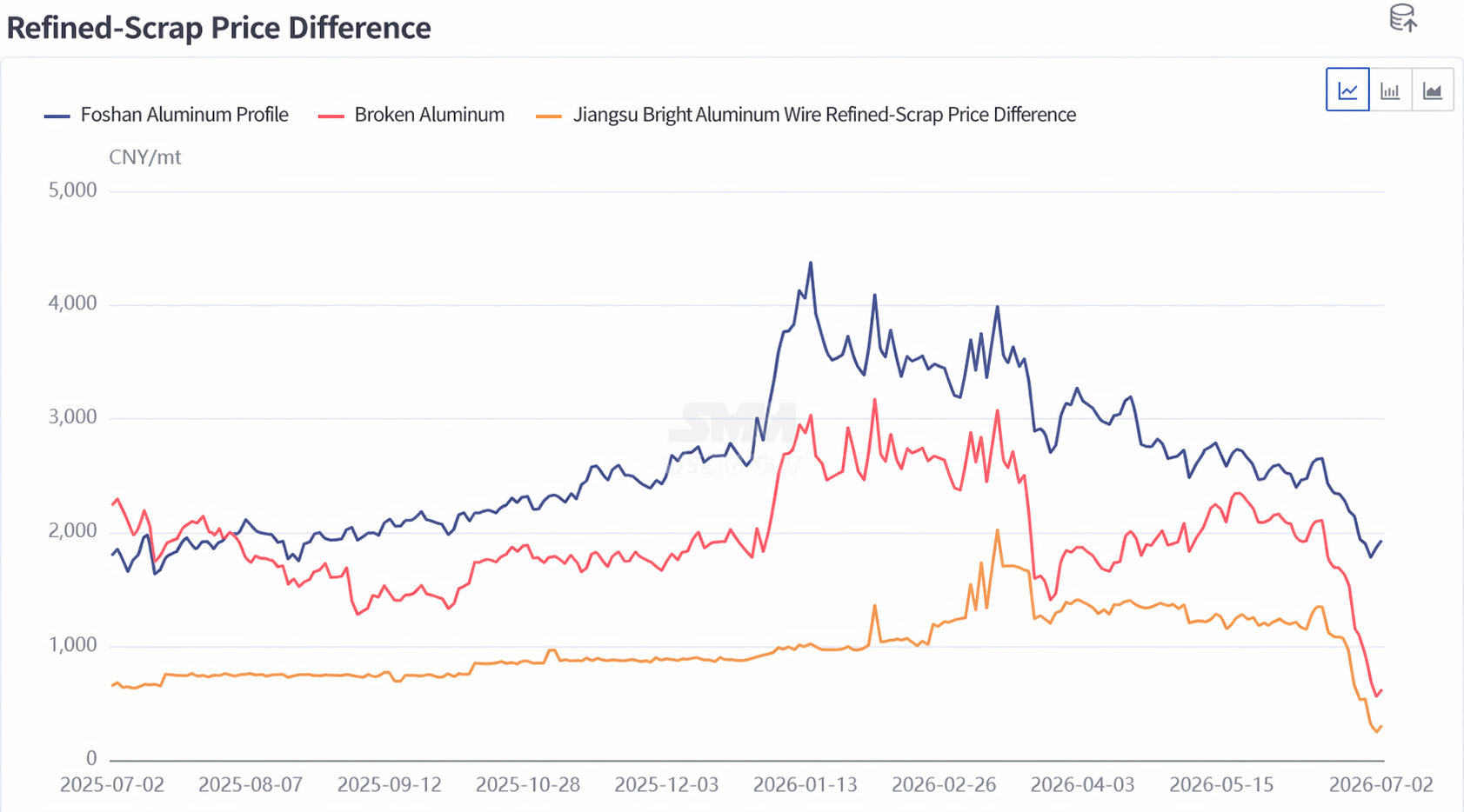

Today, SMM A00 spot aluminum prices closed at 22,760 yuan/mt, up 220 yuan/mt from the previous trading day, and aluminum scrap prices largely followed suit. The supply side remained tight as supervision over the "reverse invoicing" policy continued to tighten. Production cuts and shutdowns spread among small and medium-sized scrap utilization enterprises in Anhui, Jiangxi, Hubei and other regions, and Shandong also heard news of suspending reverse invoicing from July, further increasing the scarcity of compliant invoiced aluminum scrap. Regarding price spreads, on July 2, the price difference between A00 aluminum and mixed aluminum extrusion scrap free of paint in Foshan was recorded at 1,931 yuan/mt, and the price difference between A00 aluminum and shredded aluminum tense scrap was 623 yuan/mt. Notably, under the dual pressure of rapidly declining aluminum prices and tight invoice availability, the price spread for aluminum tense scrap narrowed sharply. Some cast aluminum alloy enterprises have begun using A00 aluminum ingots as a substitute for aluminum scrap as raw material. On the import side, besides low port arrivals in June-August due to the 1-3 month shipping lag, the UAE's four-month temporary export ban on aluminum scrap starting in June and the EU's proposed 15% tariff from September have significantly strengthened expectations of shrinking overseas high-quality scrap supply, and the import supply chain will suffer substantial damage.

The aluminum scrap market is expected to continue to consolidate at low levels, but the downside room for prices is limited. The mainstream range of shredded aluminum tense scrap prices based on aluminum content is projected at 19,200-19,800 yuan/mt (tax excluded). Supply side, the constraints from the reverse invoicing policy are unlikely to reverse in the short term, and the tight supply of compliant invoiced cargo will persist. Import side, multiple headwinds will gradually materialize in the form of depressed actual port arrivals in the coming months, and the supply of imported aluminum scrap will weaken further. Demand side, amid the deepening off-season, downstream operating rates remain low, end-user orders are unlikely to see substantial improvement, and scrap utilization enterprises will likely continue their strategy of purchasing as needed and maintaining low inventories. The price spread between aluminum scrap and primary aluminum has narrowed to a historical low, significantly eroding the economic advantage of scrap over primary aluminum. If aluminum prices continue to fall, the substitution effect will accelerate and become more evident.