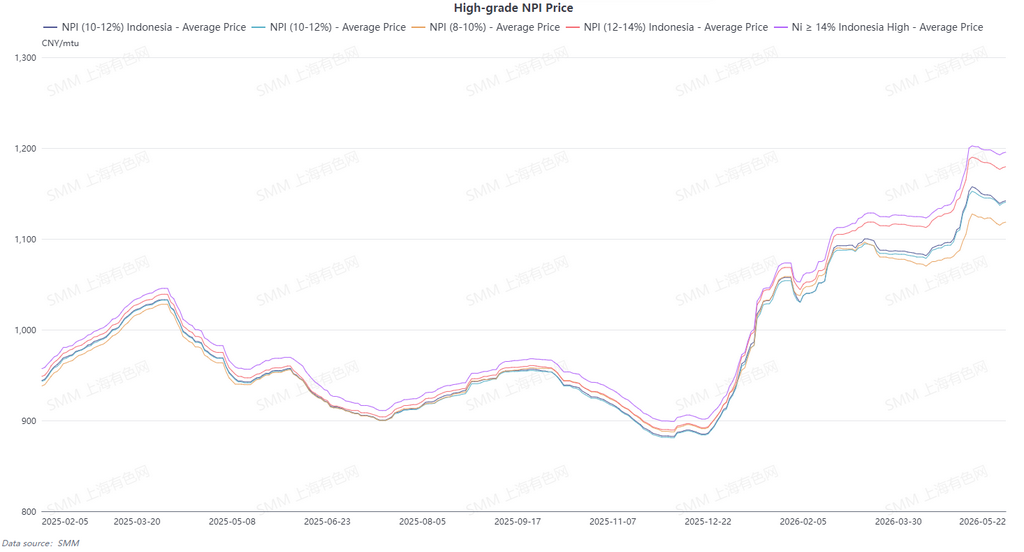

The average price of SMM 10-12% high-grade NPI fell WoW by 13.3 yuan/nickel unit to 1,133.7 yuan/nickel unit (ex-factory, tax included), and the average price of the Indonesian NPI FOB index fell WoW by $0.31/nickel unit to $146.69/nickel unit. This week, the high-grade NPI market remained in the doldrums under a supply-demand tug-of-war and persistently sluggish trading, with prices under pressure overall.

Tight spot circulation provided bottom support for offers, and suppliers maintained resilient pricing. However, alternative raw materials such as steel scrap and refined nickel boasted a clear price ratio advantage, continuously diverting rigid demand for NPI. Downstream steel mills pushed aggressively for lower prices, leading to a wide bid-ask spread that made bulk transactions difficult to conclude. By mid-week, the gap between supply and demand price expectations widened further. Sellers showed no willingness to actively make concessions through shipments, and there was no pressure for concentrated spot selling in the short term. Yet, persistently weakening futures continued to erode NPI's own cost-effectiveness, further suppressing steel mills' willingness to purchase. Most suppliers opted to suspend one-price offers, leading to a notably stronger wait-and-see sentiment. In the latter half of the week, the market's weak logic gradually became clear, with price cuts for high-nickel-unit cargoes being more pronounced. The price spread between grades narrowed, and high-priced support for high-nickel cargoes gradually failed. Throughout the week, downstream restocking demand remained weak as steel mills slowed their procurement pace and essentially made no proactive, concentrated restocking moves. The market only saw the execution of prior orders and the circulation of a few small, scattered deals, lacking guidance from significant firm transactions. The tight spot balance only limited the extent of the price decline but could not reverse the core situation of weak demand and sluggish transactions. Looking ahead to next week, nickel prices are expected to rebound amid cooling expectations for US Fed interest rate hikes, and NPI is expected to stop falling and stabilize, driven by nickel prices.

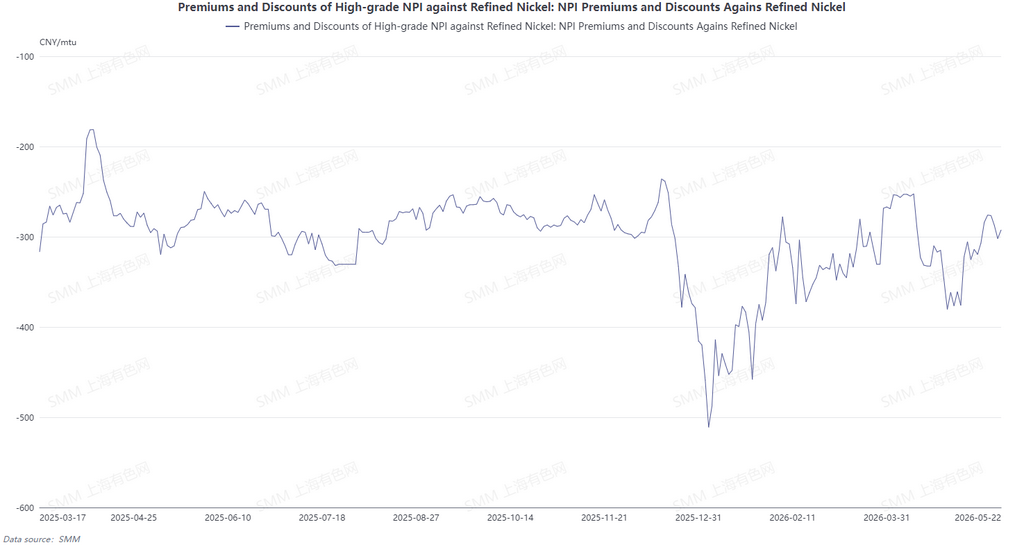

From the perspective of converting NPI to high-grade nickel matte, the overall center of refined nickel prices continued to shift lower this week. However, supported by tight spot supply, the downside room for China's high-grade NPI prices was limited, with the decline notably smaller than that of refined nickel. The discount between the two continued to narrow, and the average discount of high-grade NPI to refined nickel converged to 127.7 yuan per nickel unit. Looking ahead to next week, market expectations suggest that refined nickel prices are likely to see a certain degree of WoW recovery and rebound, which may drive the discount of high-grade NPI against refined nickel to widen again, though the expansion of the price spread is expected to be relatively limited. Meanwhile, the current equivalent price spread between nickel pig iron and high-grade nickel matte can hardly cover the conversion costs, leaving enterprises without economic incentive to convert high-grade NPI into high-grade nickel matte. The conversion logic remains difficult to materialize in the near term.

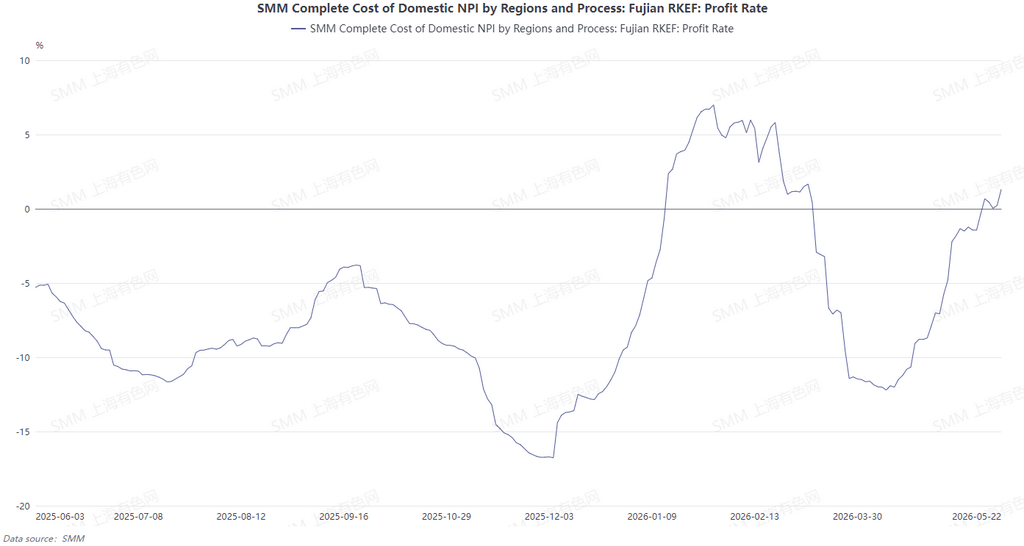

This week, smelting costs for NPI in and outside China saw simultaneous improvement. Chinese plants mainly purchased Philippine nickel ore, with ore prices continuing to decline, and coupled with stable domestic coal prices, the cost advantage on the raw material side was further consolidated, allowing domestic NPI enterprises' profitability to be maintained at a stable level. Indonesian local nickel ore prices also moved lower; together with the use of low-priced Philippine nickel ore, ore procurement costs saw a notable pullback. Despite persistent upward pressure on Indonesian coal and electricity auxiliary materials, the considerable benefits from ore price declines significantly eased overall production cost pressure and opened up room for profit recovery on the smelting side.

![[SMM Analysis] Weak Nickel Caps Chinese Stainless Steel Futures in a Tight Range as Mill Price Discipline](https://imgqn.smm.cn/production/admin/votes/imagesLDoQB20260703182347.png)

![[SMM Analysis] Nickel and Cobalt Salt Prices Weak; Intermediate Product Payables Under Pressure](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)

![[SMM Analysis] Indonesia's nickel ore HMA sharply cut by 7.6%, high inventories in China and Indonesia suppress nickel ore market sentiment](https://imgqn.smm.cn/usercenter/vcoVV20251217171732.jpeg)