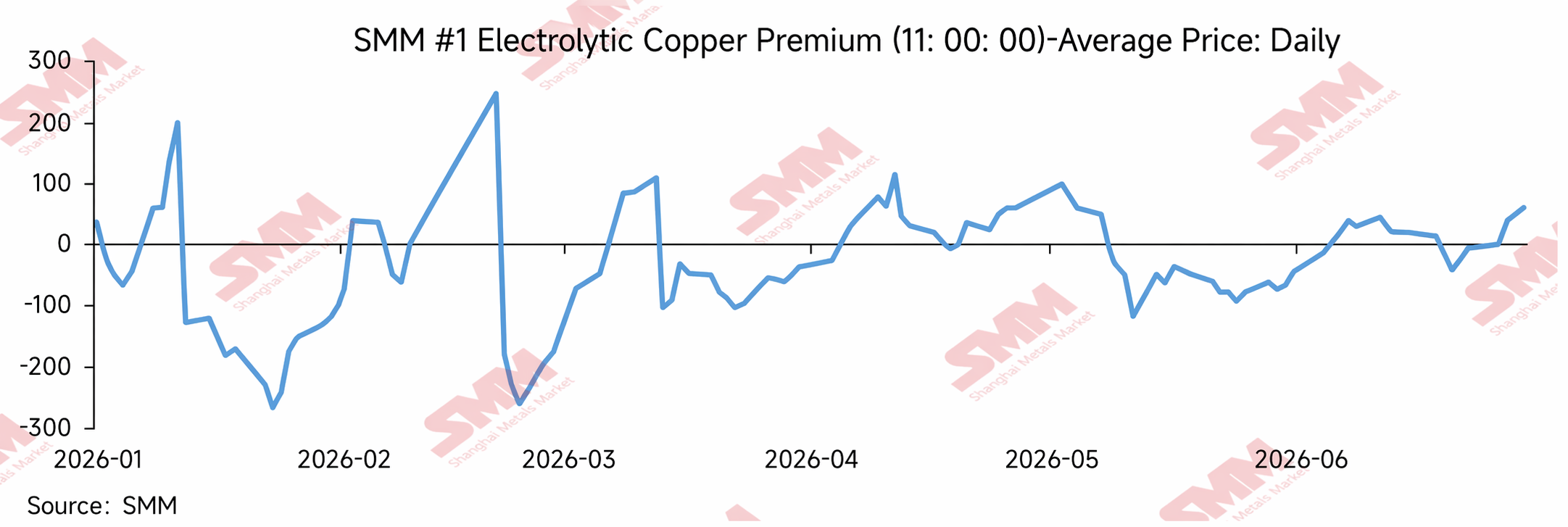

In H1 2026, SHFE copper cathode spot premiums fluctuated noticeably, exhibiting characteristics of “high volatility, periodical deep discounts, recovery in Q2, and a return to premiums at mid-year.”

Around the Chinese New Year, spot premiums fluctuated more sharply driven by downstream stockpiling, contract rollover, and inventory changes. After the holiday, as social inventory built up seasonally and downstream recovery was slow, the spot market once came under pressure and weakened. After entering Q2, as social inventory continued to destock, particularly the rapid decline in Guangdong, spot premiums in South China rose sharply, opening an arbitrage window for transferring inventory from East China to South China, which indirectly lifted spot premiums in Shanghai. In May-June, although high copper prices and off-season expectations dampened downstream purchases, the COMEX-LME price spread continued to widen. This strengthened the momentum of supplies flowing to the US market from outside China, disrupting the pace of imported copper arrivals in China. The low domestic inventory environment still provided support for spot premiums.

Overall, SHFE copper premiums in H1 2026 were not simply determined by local consumption strength in Shanghai, but were shaped by a combination of low domestic inventory, regional inventory divergence, cross-regional inventory arbitrage, limited imported copper replenishment, and changes in overseas price spreads. Low inventory provided underlying support for the spot market. High premiums in Guangdong were a key driver of the premium recovery in Q2. The widening COMEX-LME spread reduced imported copper’s ability to supplement the domestic market, allowing SHFE copper premiums to show resilience even as consumption weakened at the margin.

1. Review of SHFE Copper Premiums in H1

January: Pre-Holiday Stockpiling and Contract Rollover Disruptions Amplified Premium Volatility

In January 2026, SHFE copper spot premiums were highly volatile. At the beginning of the month, the market was still in the pre-holiday stockpiling window, and some downstream enterprises still had restocking needs before the Chinese New Year. Combined with contract rollover and temporary changes in the supply structure, spot premiums strengthened temporarily. However, as the holiday approached, downstream enterprises gradually shut down, market trading turned thinner, and traders faced increasing pressure to sell. This caused spot premiums to pull back quickly and shift into discounts.

From a market performance perspective, the rapid fluctuations in premiums in January reflected pre-holiday trading pace adjustments and supply-side disruptions rather than sustained improvement in consumption. In the last stage before the Chinese New Year, downstream purchases gradually contracted, market buying decreased, and suppliers actively lowered their offers to facilitate transactions, causing spot discounts to widen. This also laid the foundation for the seasonal inventory buildup after Chinese New Year and the spot market being in the doldrums in Q1.

Post-holiday Inventory Buildup Weighs on Spot Market; Premiums Recovery Lacks Sustainability, February-March.

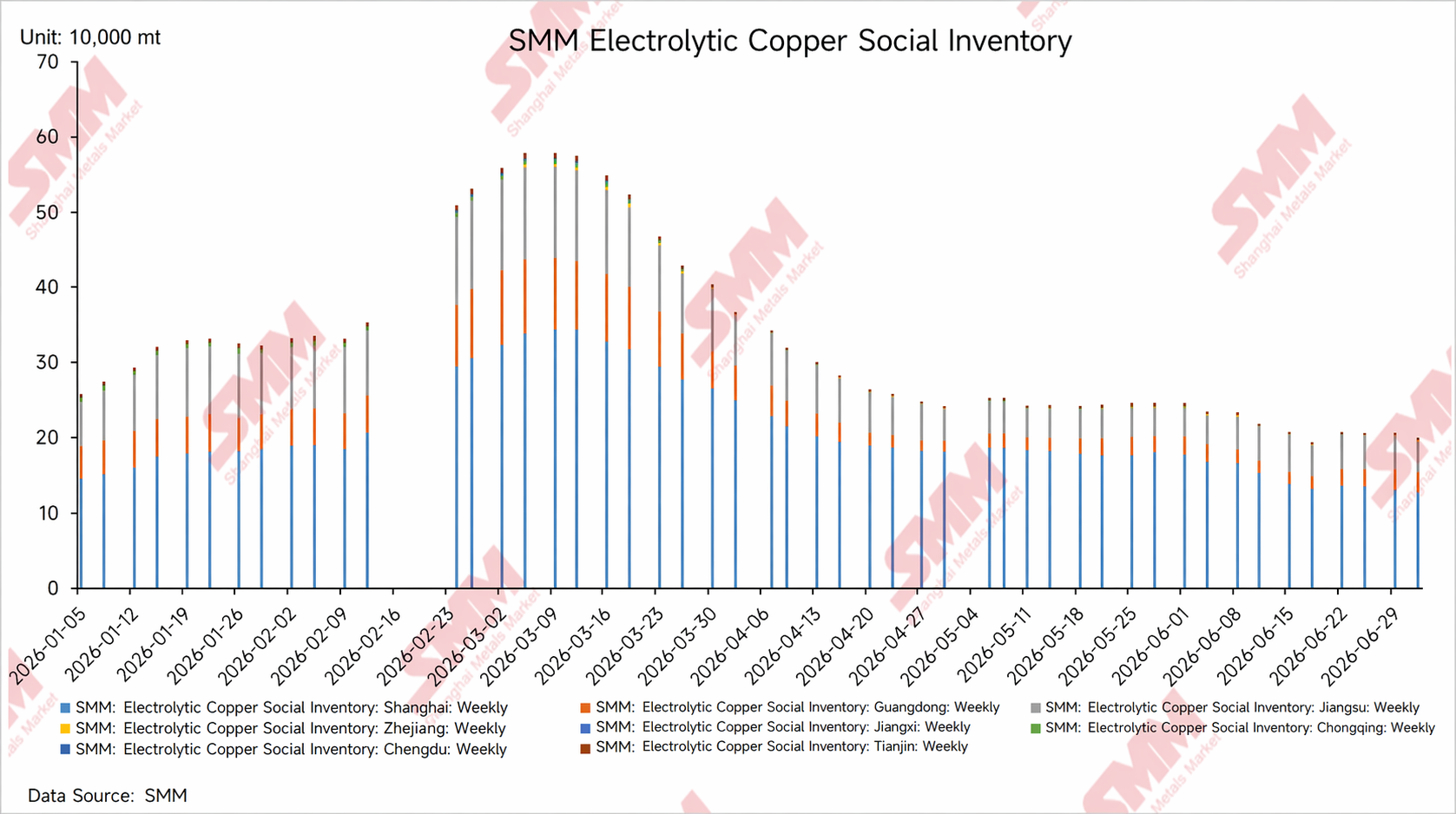

After Chinese New Year, China's social inventory of copper cathode entered a seasonal inventory buildup cycle, with downstream enterprises resuming operations at a relatively slow pace and end-use order recovery still requiring time. Against the backdrop of inventory accumulation outpacing consumption recovery, suppliers were under heavy shipment pressure, spot market quotations were broadly under pressure, and SHFE copper premiums once stayed at deep discounts.

Around mid-February, affected by contract rollover, phased tightening of available cargoes, and market sentiment disruptions, premiums experienced a brief rapid surge. However, because downstream consumption had not yet fully recovered at that time, inventory pressure remained, and high spot premiums struggled to gain sustained support from transactions, quotations subsequently fell back again. This indicates that the phased spikes in the spot market in Q1 were driven more by short-term supply and futures structure disruptions than by a genuine broad-based strengthening of consumption.

After entering March, as downstream operations gradually advanced, spot market transactions improved compared with the post-Chinese New Year period, social inventory growth slowed and gradually entered the initial destocking phase, and premiums recovered somewhat from the previous deep discounts. However, because end-use demand recovery remained mild, high copper prices inhibited downstream procurement, and the market was dominated by just-in-time transactions. The premium recovery process was not smooth, and after contract rollovers, premiums still repeatedly fell back into discount territory.

Overall, in Q1, the main logic driving the Shanghai spot copper market was “post-holiday inventory buildup pressure + slow downstream recovery + contract rollover delivery disruptions.” Although premiums rebounded in phases, they lacked a basis for sustained rise.

Inventory Drawdown and Consumption Improvement Lift Premiums Center in Phases, April-May.

After entering Q2, the operating logic of the Shanghai spot copper market underwent marginal changes. As the traditional peak consumption season arrived, the operating rates of some downstream sectors, such as wire and cable, copper cathode rod, copper pipe & tube, and copper plate/sheet and strip, improved MoM, end-user just-in-time procurement recovered somewhat, and social inventory began to gradually destock. Meanwhile, from April to June, domestic smelters entered a period of relatively concentrated annual maintenance, with some undergoing phased maintenance or slowing their shipment pace, causing market arrivals to fall short of expectations and further tightening available cargoes. Under the combined effect of demand recovery MoM and supply-side maintenance disruptions, suppliers' willingness to hold prices firm strengthened, and the center of spot premiums shifted upward accordingly.

Furthermore, continuous destocking in Guangdong and high spot premiums in South China were also important drivers. In Q2, downstream consumption in South China recovered MoM, and combined with slower regional arrivals during the smelter maintenance season, Guangdong's social inventory kept declining, available cargoes within the region tightened markedly, suppliers' sentiment for holding prices firm strengthened, and spot premiums in Guangdong were at one point significantly higher than in Shanghai. Against this backdrop, the price spread between east China and south China gradually widened, creating some arbitrage opportunities from moving inventory between regions. Expectations of some cargoes being shipped from east China to south China strengthened, thus also marginally affecting the available supply in the Shanghai market, indirectly boosting Shanghai spot premiums.

The core driver of the strength in premiums during this period was not entirely a surge in demand, but rather the amplification of spot price elasticity in a low-inventory environment. On one hand, as social inventories declined, the pool of selectable cargoes for traders and downstream enterprises shrank, and low-priced cargoes were quickly traded. On the other hand, smelter maintenance caused a temporary reduction in shipments, coupled with unstable arrival rhythms of some imported copper, intermittent closure of the import window or widening losses, which limited domestic spot replenishment, further strengthening suppliers' willingness to hold prices firm.

Overall, the Q2 SHFE copper spot market gradually shifted from being “dominated by inventory pressure” in Q1 to being “supported by destocking logic.” Among these factors, QoQ improvement in consumption provided the demand base, concentrated smelter maintenance slowed supply replenishment, and rapid destocking in Guangdong amplified regional premium elasticity. Together, these three factors drove the center of SHFE copper premiums higher in stages in April-May.

May-June: High copper prices and off-season expectations suppressed procurement, with premiums showing intensified fluctuations

From late May to June, the SHFE spot copper market entered a phase of mixed bullish and bearish factors. On one hand, the traditional consumption off-season was approaching, and high copper prices further suppressed downstream purchasing sentiment, with end-users mostly making just-in-time procurement and showing little willingness to restock proactively. Spot trading activity declined compared with April-May. On the other hand, domestic social inventory remained relatively low, and the impact of concentrated smelter maintenance from April to June had not yet fully faded. In some regions, arrivals for replenishment remained limited, and suppliers were reluctant to sell at low prices, so premiums did not weaken sharply in a unilateral manner.

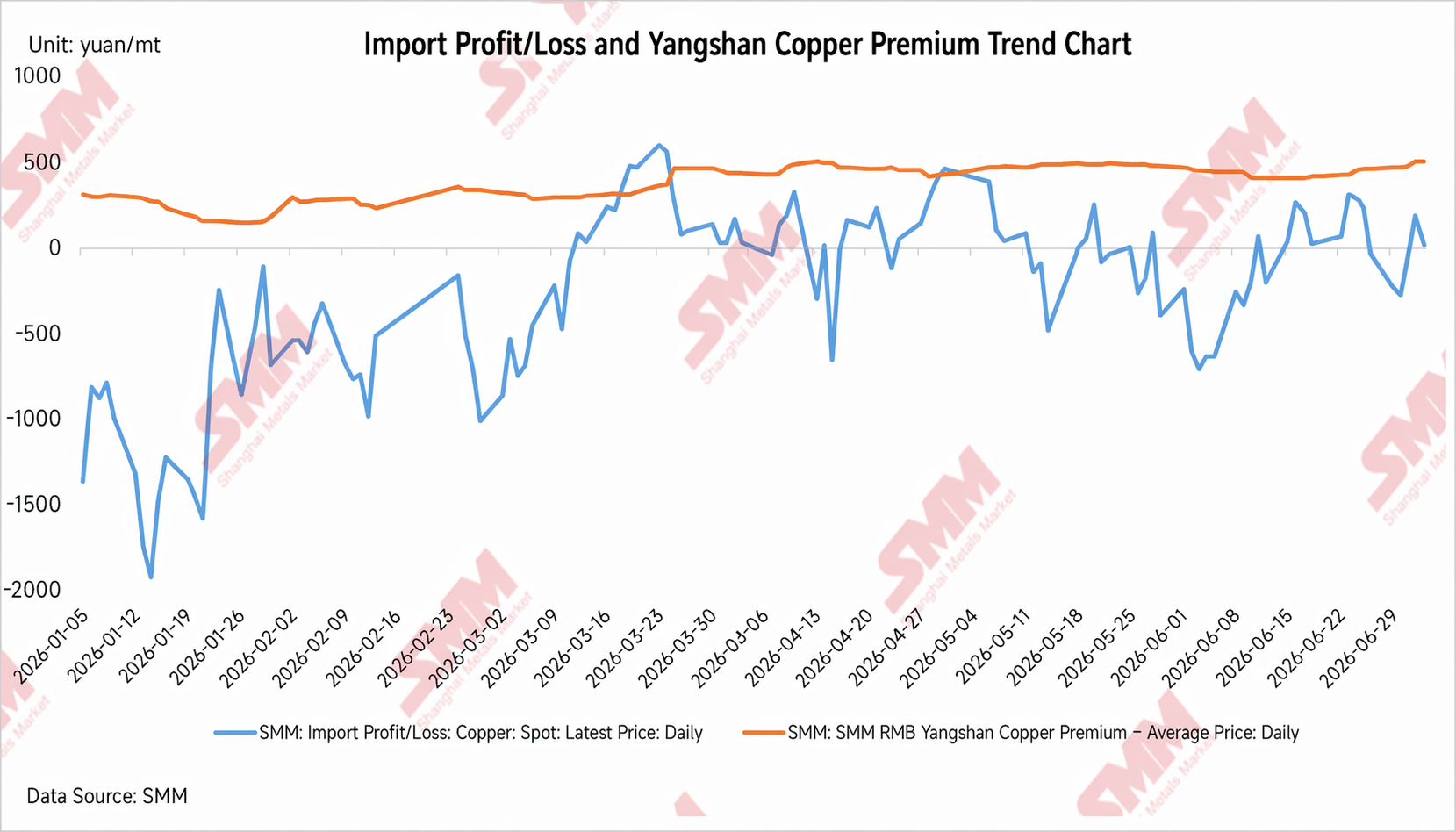

During this period, apart from low domestic inventories and smelter maintenance disruptions, the widening LME-COMEX price spread also became an important external variable affecting SHFE copper premiums. In May-June, COMEX copper prices outperformed LME, and the LC spread continued to expand, altering overseas copper cathode trade flows. Some delivery brand cargoes were more likely to head to the US market to capture higher delivery or arbitrage gains, squeezing the overseas spot resources available to Asia and the Chinese market.

From the perspective of China's copper imports, the expanding LC spread reduced the incentive for overseas cargoes to flow into the Chinese market. Even as the domestic SHFE/LME price ratio recovered in stages, there was still a lag in actual arrivals and customs clearance of imported copper. For the domestic spot market, this meant that with low inventories, imported copper could not quickly provide effective replenishment, and suppliers' concerns about subsequent concentrated arrivals eased, keeping spot price quotations supported.

Therefore, the resilience of SHFE copper premiums in May-June should not be simply attributed to still-strong domestic consumption; it was the combined result of low inventory, smelter maintenance, insufficient import supplementation, and the diversion of overseas supply. Against a backdrop of weakening downstream procurement, the upside room for premiums was limited. However, because domestic supply replenishment was limited and arrivals of imported copper fell short of expectations, the spot market was unable to quickly ease. Premiums overall consolidated at highs with periodic fluctuations.

II. Core Drivers of SHFE Copper Premiums in H1

1. Inventory: Low Inventory Was a Key Support for Spot Premiums

The core support for SHFE copper premiums in H1 came from inventory changes. After Chinese New Year, social inventory accumulated and spot premiums came under pressure. Entering Q2, inventory continued to draw down, tightening available supply in the market and boosting suppliers’ willingness to hold prices firm. Notably, Guangdong inventory declined rapidly in April-May, driving a significant increase in spot premiums in South China and creating arbitrage opportunities to ship inventory from East China to South China, which indirectly supported the Shanghai market. Thus, the recovery in Q2 premiums was not driven solely by Shanghai’s local consumption, but was the combined result of low inventory and regional cargo movements.

2. Consumption Recovery Supported Premiums, While High Copper Prices and Price Spreads between Futures Contracts Capped Sustained Upside

During Q2’s traditional peak season, downstream just-in-time procurement improved, providing support for the recovery in premiums. But against the backdrop of copper prices fluctuating at highs, downstream willingness to restock proactively was limited, and spot transactions were mainly need-based, capping the room for sustained premium gains. Meanwhile, contract rollover, delivery, and changes in SHFE copper price spreads between futures contracts increased short-term fluctuations. Overall, consumption determined the upside height of the premium recovery, price spreads between futures contracts set the short-term pace, and high copper prices limited sustained upside.

3. Import: Changes in Import Profit Margins Affected the Pace of Domestic Spot Replenishment

The flow of imported copper had a clear impact on SHFE spot copper premiums. When import losses widened and the import window closed, the incentive for overseas supply to flow into China weakened, domestic spot replenishment was limited, and suppliers’ sentiment to hold prices firm strengthened, making premiums easy to support. Conversely, when import losses narrowed or even the window temporarily opened, market expectations for increased arrivals of imported copper rose, suppliers turned cautious on pricing, and the upside room for premiums was capped.

In May-June, the LME-COMEX spread continued to widen, strengthening the incentive to divert deliverable overseas supply to the US market, which squeezed the availability of imported copper resources for Asian and Chinese markets. Meanwhile, although China’s import profit margins recovered somewhat, delays in actual arrivals and customs clearance prevented the domestic spot market from quickly shifting to looseness. Insufficient import replenishment combined with low inventory levels became a key reason for the resilience of SHFE copper premiums in the first half of the year.

III. Outlook for SHFE Copper Premiums in H2 2026

Looking ahead to H2, SHFE copper premiums are expected to continue to revolve around inventory, consumption, imports, regional price spreads, and the spread structure between futures contracts. Low inventory will remain a key factor supporting the spot market, but the dampening effect of high copper prices on downstream consumption, changes in the pace of import replenishment, domestic smelter shipment pace, and the seasonal shifts will jointly shape the range of premiums movements.

1. Q3: Off-Season to Cap Premium Upside, but Low Inventory May Limit Discount Depth

Q3 is typically the traditional off-season for copper consumption, and weakening orders from some end-users could impact downstream operating rates. Against the backdrop of high and fluctuating copper prices, downstream enterprises will likely remain cautious in procurement, with spot transactions expected to be dominated by rigid demand and limited active restocking demand. If consumption lacks significant improvement, the upside room for SHFE copper premiums may be constrained.

On the supply side, if social inventory remains low and import copper replenishment is limited, it will be difficult for the spot market to see deep discounts. On one hand, low inventories will continue to support supplier quotes; on the other hand, if the COMEX-LME price spread remains at a relatively high level, cargoes from outside China will continue to divert to the US market, which may continue to affect the arrival pace of imported copper into China, making it hard for the domestic spot market to quickly ease.

Therefore, SHFE copper premiums in Q3 are likely to exhibit a pattern of “weak demand but limited discounts.” The off-season consumption cap on premium upside will be limited, but low inventories, import replenishment uncertainties, and tight regional supply may keep the discount space relatively contained. Overall, spot premiums in Q3 are expected to move sideways, with periodic fluctuations still depending on the spread structure between futures contracts, inventory changes, and the pace of import copper customs clearance.

2. Q4: Focus on Peak-Season Realization and Inventory Inflection; Premiums May See Phased Recovery Opportunities

As the market enters Q4, attention will gradually shift to whether the consumption peak season materializes. If power grid investment, home appliance production schedules, new energy, and manufacturing orders show marginal improvement, downstream purchasing enthusiasm may pick up compared with Q3, and copper cathode consumption could see a phased recovery. In the absence of significant inventory buildup, SHFE copper premiums could again strengthen.

However, it should be noted that whether premiums can continue to rise in Q4 still depends on the pace of replenishment from the supply side. If the import window opens intermittently, leading to concentrated arrivals of imported copper, or if domestic smelters increase their shipments, the tight supply situation in the spot market could ease, limiting the room for premium recovery. In addition, in H2, on the supply side of China's copper cathode, close attention should be paid to the release pace of new and expansion capacities. Besides the Youjin Guanhua project, which was commissioned and started producing copper cathode in June, projects such as Humon Phase II, Chifeng Jintong Phase II, and Shenghai Phase II will also be key sources of supply growth drawing market attention in H2. As these projects are successively commissioned, ramp up, and form stable output, expectations for supplementary Chinese copper cathode supply will gradually strengthen.

Meanwhile, if high copper prices continue to suppress end-user purchasing and downstream restocking fails to gain volume, then even if premiums stage periodic strength, they may struggle to form a sustained trend.

Therefore, in Q4, SHFE copper premiums are more likely to exhibit a phased recovery rather than a one-way uptrend. The core criteria for judgment are: whether inventory destocking continues, whether downstream orders improve, whether imported copper arrives in concentrated volumes, whether high premiums in Guangdong reappear, and whether the inter-month spread structure continues to support spot price firmness.

Summary

Overall, in H1 2026, the trend of SHFE copper premiums exhibited distinct phased characteristics. In Q1, impacted by post-holiday inventory buildup and slow downstream production resumption, spot premiums were under pressure and fluctuated repeatedly; in Q2, as inventories destocked—especially with a rapid decline in Guangdong inventory and high premiums in South China opening up inter-regional arbitrage opportunities through warehouse movement—premiums across regions were boosted; from May to June, although expectations of an off-season consumption lull intensified, the widening COMEX-LME price spread led to a diversion of overseas supply, limiting China's imported copper replenishment, and the domestic low-inventory structure continued to underpin the spot market.

Looking ahead to H2, SHFE copper premiums will continue to be shaped by the tug-of-war among inventory, imports, consumption, and new supply additions. In Q3, the off-season may cap the upside for premiums, but low inventories, uncertain import replenishment, and tight supply in Guangdong could still support the spot market; in Q4, the key focus will be on the capacity ramp-up of new and expansion projects. Should Humon Phase II, Chifeng Jintong Phase II, Shenghai Phase II and others gradually release production, coupled with increased imported copper, domestic spot supply pressure could edge higher, capping the upside for premiums.

Overall, in H2, SHFE copper premiums are very likely to remain caught in a dual tug-of-war between 'low inventory support' and 'supply addition pressure'. If inventories stay low and imported copper replenishment is limited, premiums will still have opportunities for periodic strength; but if new capacity releases proceed smoothly, the import window opens, and consumption recovery remains weak, spot premiums could come under gradual pressure.

![End-User Purchasing Enthusiasm Weakens, Tight Supply Pushes Up North China Spot Discounts [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)

![Market Spot Copper Supply Scarce, Intraday Offers Sluggish [SMM Yangshan Spot Copper]](https://imgqn.smm.cn/usercenter/JYzFE20251217171714.jpeg)