SMM July 4 report:

The overall supply-demand imbalance persisted, with prices showing little improvement.

Looking back at H1 2026, the polysilicon market faced prominent overcapacity and a historical inventory overhang. Despite occasional rebounds supported by policy expectations, the overall downward trend remained intact.

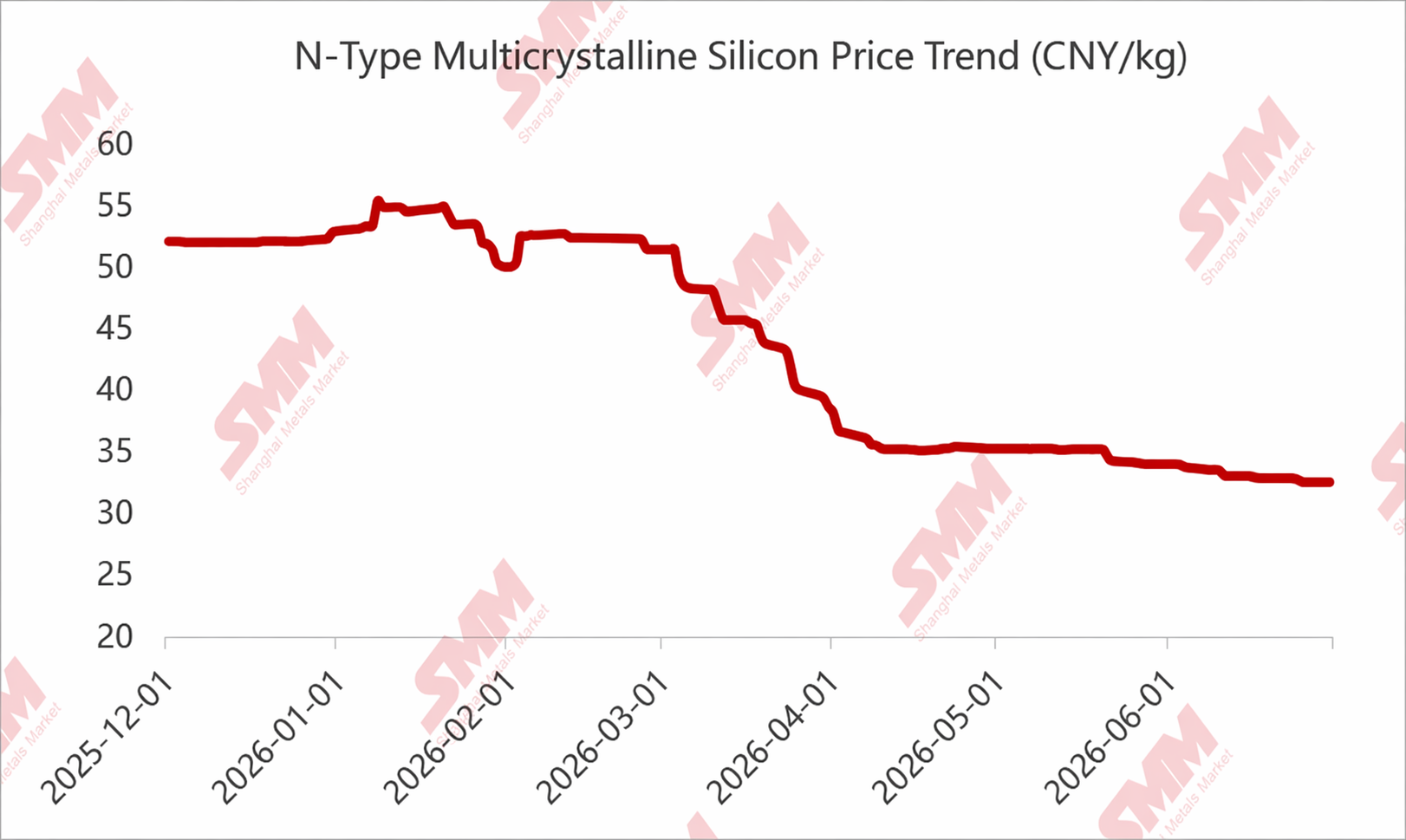

Price-wise, the high point came in early-to-mid January, driven by the December CPIA industry conference, the “capacity consolidation company,” and self-discipline expectations. Prices steadily rose, supported by the reported 60 yuan/kg full cost line. Actual transactions surpassed 55 yuan/kg, and some quotes even exceeded 60 yuan/kg.

However, weak downstream demand persisted, and downstream segments were unwilling to accept excessively high prices. More importantly, as self-discipline progress fell short of expectations and some actions were even “suspended,” polysilicon prices began to decline.

Another meeting was held around February, but the outcome was disappointing. Coupled with the Chinese New Year off-season, a very brief rebound was followed by another downward move.

From there, polysilicon entered a prolonged and steady decline. Even with export tax rebate policy support and broad-based downstream price gains from March to April, polysilicon prices showed no meaningful improvement. The reasons were: 1) the historical polysilicon inventory backlog was severe, with producer inventory maintained at 4–6 months levels for most of H1; 2) overcapacity was evident, with more than 3 million mt of commissioned capacity. Even excluding long-term idled capacity, around 2.5 million mt remained, compared to demand just over 1 million mt in 2026—the oversupply pressure was indeed too great; and 3) the market was deeply concerned about the upcoming rainy season supply in Q2, leading to extremely cautious procurement starting in March.

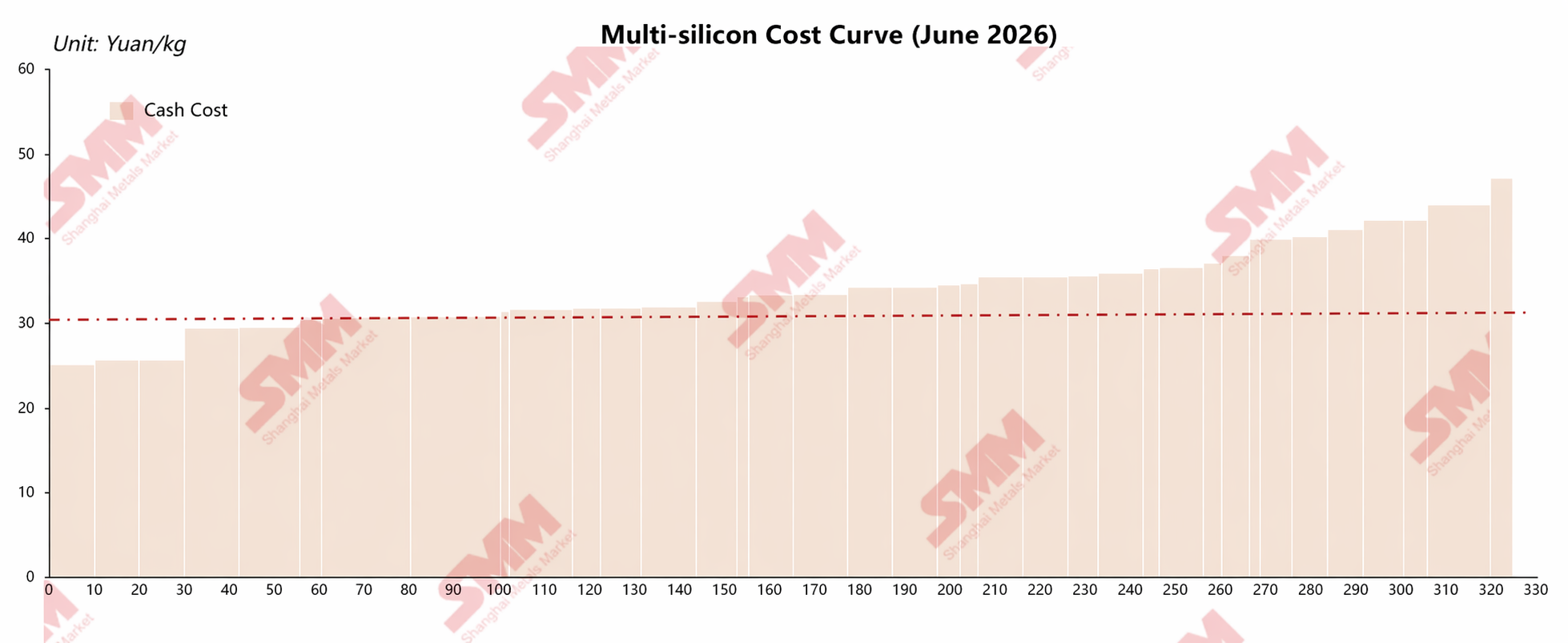

Under these conditions, polysilicon prices fell below the previous year’s low in June. Dense/recharge polysilicon spot prices dropped to as low as 31 yuan/kg, and some mixed polysilicon prices even fell below the 30 yuan mark.

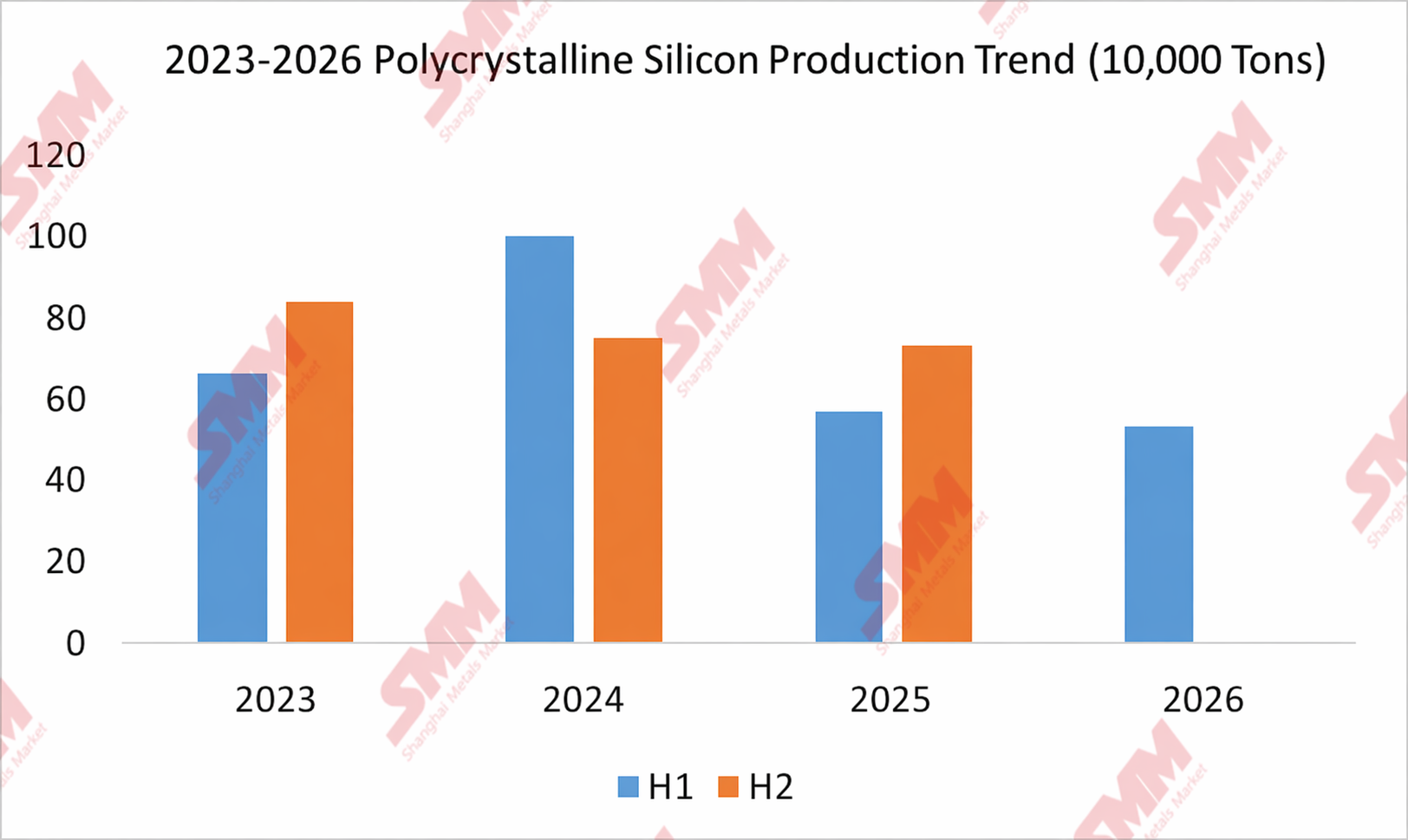

Supply-demand side, H1 2026 polysilicon operating rates were already “relatively restrained” due to pricing and cost pressures. In particular, a top-tier player halted all production at the start of the year, significantly limiting H1 output. According to SMM data, total China polysilicon production in H1 2026 was 534,400 mt, a YoY decline of 6.8% and a 46.67% drop from 2024. Yet the historically accumulated inventory was so massive and the overcapacity so extreme that meaningful destocking proved impossible.

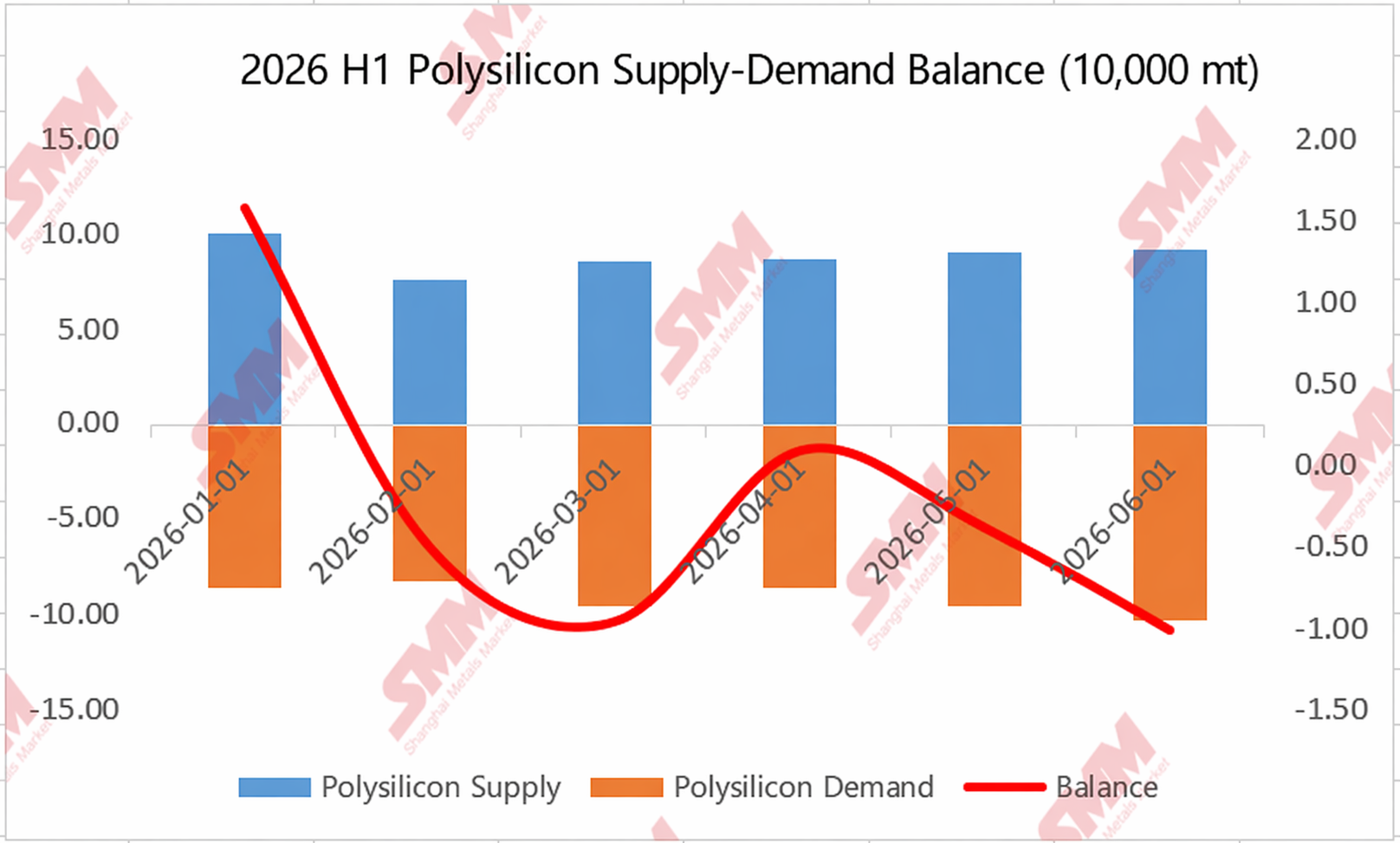

The supply-demand chart also clearly shows that, although inventory was drawn down for much of the half, the actual destocking volume was minimal.

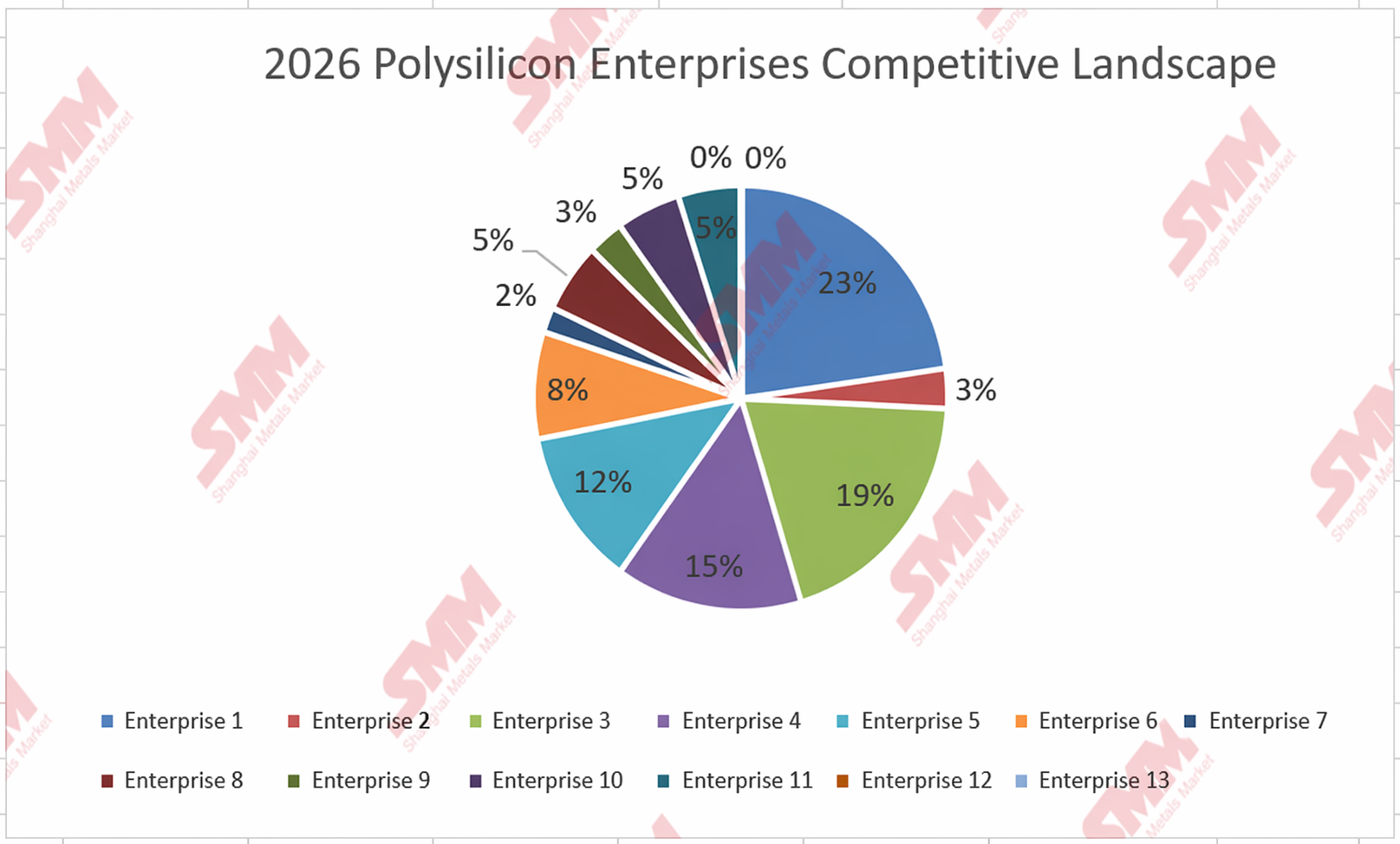

Enterprises are also spontaneously exiting the market, while top-tier concentration remains undiminished.

Looking at individual enterprises, the market is undergoing spontaneous elimination and exit. SMM data shows that in 2024, there were about 16 enterprises that maintained stable production (not in long-term shutdown); in 2025, this number dropped to 13; and as of now, only 11 enterprises remain relatively stable in operation.

Market competition pattern, top-tier concentration from 2025 to H1 2026 did not show a significant decline. In 2025, CR5 accounted for about 78%, and in 2026, even against the backdrop of major production cuts at top-tier players in H1 (partly influenced by the low-water season), CR5 still stood at 77%.

H2 2026 Outlook: Focus on Costs and Policies

Looking ahead to H2 2026, SMM believes that from the supply-demand or capacity side, it is difficult to see a significant spontaneous improvement. Key attention should be paid to policy expectations and cost conditions—costs determine the price floor, while policies determine the price trend.

SMM believes that from the current price perspective, polysilicon prices in H2 are unlikely to see another significant drop. From the base cost curve, at the current price of around 31-33 yuan, except for granular polysilicon and a few top-tier advanced bases, most bases are already unable to cover their cash cost. This is also evidenced by the recent increase in enterprises cutting production in Xinjiang, Inner Mongolia, and other regions as prices have declined, with polysilicon enterprises showing little willingness to cut prices significantly. SMM believes the cash cost line of top-tier bases may serve as the lower limit for polysilicon prices in H2.

However, another key factor to watch in H2 is policy. Since H2 2025, polysilicon prices have been strongly influenced by policy factors. Related industry meetings were held as early as April, and preliminary discussions on energy consumption standards also took place in early May. Currently, market participants widely speculate that subsequent policies may follow two directions: one is to phase out high-energy-consuming capacity through energy consumption standards, and the other is a restriction against “selling below cost.” However, as of now, there have been no clear policy signals. There have been multiple market “rumors” previously, but most were later proven to be “false.” In recent days, some bases have indicated that they have submitted some relevant information. Some market participants speculate that there is a high likelihood of significant policy moves going forward, but this remains to be observed. SMM believes that this will also be a key factor influencing polysilicon price trends in H2.

However, if no relevant policies are introduced, polysilicon prices in H2 will likely mostly consolidate near the bottom...

![[SMM Analysis] Intersolar 2026 Review: Europe’s PV Growth Slows as Policy and Returns Reshape Market Logic](https://imgqn.smm.cn/usercenter/FqtWa20251217171742.jpg)

![[SMM PV News] Jinko Energy Storage Secures 400 MWh Utility-Scale Energy Storage Project in Eastern Europe at Intersolar, Partnering with Taliva to Advance Energy Infrastructure](https://imgqn.smm.cn/usercenter/FtiwK20251217171741.jpg)

![[SMM PV Flash]Advanced manufacturing moves towards "green", and Canadian Solar Inc. helps Lianxun Instruments build a green energy system.](https://imgqn.smm.cn/usercenter/oytJq20251217171740.jpg)