Jun 30, 2026

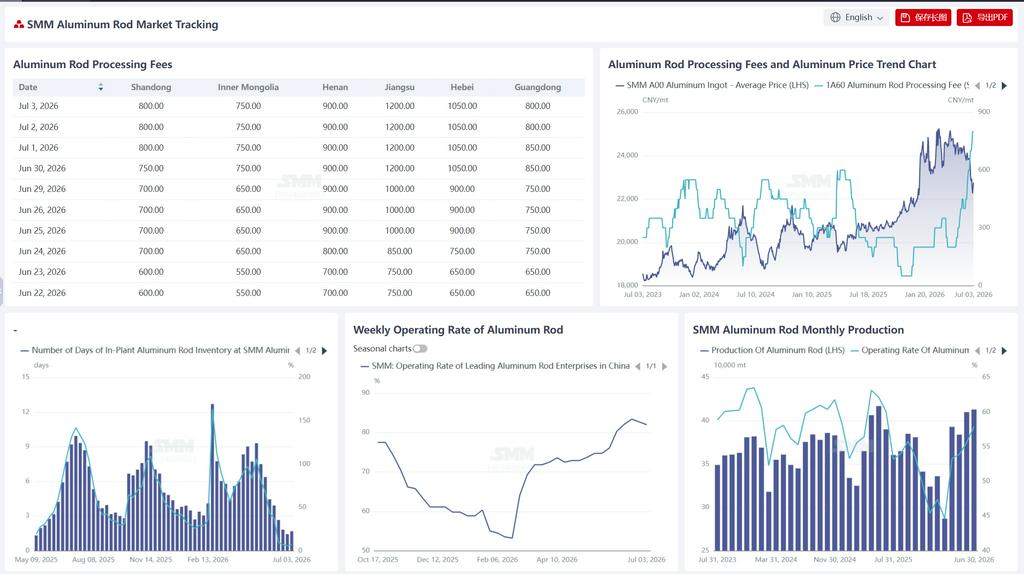

According to SMM, as of Jun 26, the in-factory inventory days of aluminum rod plants in China stood at 1.43 days, down 0.39 days WoW from 1.82 days on Jun 18, with the inventory ratio further dropping from 6.87% to 5.67%, a decline of 1.2 percentage points. The inventory destocking trend continued but the pace has narrowed significantly, indicating that inventories have hit extremely low levels and further destocking space is very limited. Over the same period, the comprehensive operating rate of industry-leading aluminum rod enterprises stood at 82.70%, down 0.7 percentage points WoW, marking the first pullback after four consecutive weeks of gains, confirming initial signs of loosening at high capacity utilization rates. The persistently low inventory was mainly due to the production schedule inertia accumulated from earlier export and State Grid orders that has not been fully absorbed. Producers are still focusing on fulfilling orders on hand, keeping supply tight. However, with losses on aluminum stranded wire exports and a significant shrinking of new export orders, demand-side support is weakening marginally. Inventory is expected to stabilize at low levels in the short term, no longer continuing the previous rapid destocking trend. The operating rate, against the backdrop of gradually shrinking export orders, will face some downward pressure after July, with a retreat from highs likely to gradually take shape.

Aluminum prices slumped sharply during the week, with SMM A00 aluminum average price falling to 22,500 yuan/mt, a daily plunge of 440 yuan/mt, a notable decline. The sharp pullback in aluminum prices, though lowering downstream raw material purchasing costs, led aluminum rod producers to generally hold prices firm, given rising cost pressure and persistently tight supply, resulting in continuously increasing processing fee quotes. As of Jun 30, aluminum rod processing fees across regions rose across the board compared with last Tuesday (Jun 23): Shandong reported 750 yuan/mt (up 150 yuan/mt), Inner Mongolia 750 yuan/mt (up 200 yuan/mt), Henan 900 yuan/mt (up 200 yuan/mt), Jiangsu 1,200 yuan/mt (up 450 yuan/mt), Hebei 1,050 yuan/mt (up 400 yuan/mt), and Guangdong 850 yuan/mt (up 200 yuan/mt). Looking at the seasonal comparison chart for the past three years, Shandong's processing fee has reached 750 yuan/mt in 2026, significantly higher than the same period in 2023 (300 yuan/mt) and 2025 (250 yuan/mt), standing at a high level for the same period in recent three years. Moreover, in trading regions, due to tight supply and producers holding prices firm, processing fees rose notably, while market trading sentiment was somewhat lackluster. The main reasons for this round of sharp increase in processing fees are: the slump in aluminum prices triggered producers' price protection, combined with unfinished earlier-order production schedules in some regions and still-tight supply, prompting traders to actively hold prices firm. However, a key concern is that export losses have largely shut the export window for aluminum stranded wire, with new order support weakening significantly. Attention will need to be paid to the strength of power grid order uptake going forward. In the near term, processing fees are expected to stay high, but as producers slow their production schedules in July and export orders are gradually cleared, downward pressure on processing fees will gradually emerge, potentially forming a downtrend through July.

This week, the operating rate of China's aluminum wire and cable industry was 69.4%, flat MoM. Operations continued to run at high levels during the week, with enterprises still mainly executing earlier orders on hand. Production schedules remained steady, and capacity utilization rates stayed high for the year. On the order side, the export market cooled notably. Weighed by successive declines in LME aluminum, export profits for China's aluminum stranded wire flipped to losses, and new orders contracted significantly, with only a few orders placed in advance by traders looking to lock in the price spread between Chinese and overseas markets. Existing production schedules can still cover full-month output, and June exports of aluminum stranded wire are expected to remain stable, but after July, as earlier scheduled orders are gradually delivered and new orders prove difficult to secure, challenges will mount. Domestically, long-cycle orders from ultra-high-voltage projects are still being delivered steadily, but the peak period for centralized cargo pick-up by power grids has not yet arrived. With raw material prices having dropped sharply, enterprises are mainly activating earlier pending production orders, providing some support for conductor-type orders. As expectations of future pressure on the export side intensify, the industry's operating rate is likely to continue to consolidate at highs in the near term, but downward pressure on the operating rate will increase after July as export orders gradually shrink.