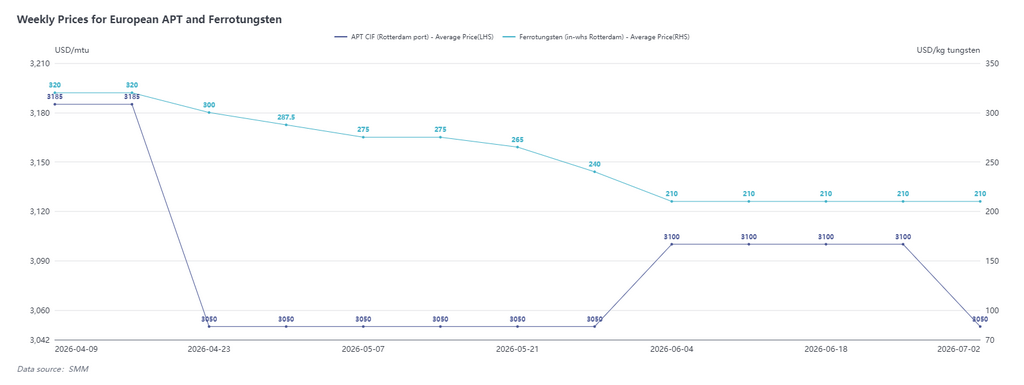

European Raw Material Market Review in June: APT at High Stalemate, Summer Break Demand Mediocre

According to SMM data, as of July 2, ammonium paratungstate (APT) was quoted at $2,900-3,200/mtu CIF Rotterdam, with the average price at $3,050/mtu, down by $50 from early June; ferro-tungsten (Rotterdam warehouse) was quoted at $180-240/kg tungsten, with the average price at $210/kg tungsten, basically flat from early June.

Approaching the summer break, the European market feedback in June was overall mediocre. A small portion of long-term contract tungsten oxide and APT were still executed at around $3,000/mtu, but the overall situation showed a pattern of high prices but no transactions, and offers appeared somewhat inflated. Multiple enterprises in Europe and the US have established relatively complete scrap recycling systems, resulting in high scrap inventory and insufficient purchase willingness for primary APT. Entering July, as the European summer break season begins, procurement willingness on the demand side remains mediocre, and market sentiment mainly fluctuates with Chinese prices. Additionally, in June there were still low-priced offers for Chinese foreign trade APT, but without export approval qualifications, the European market supply sources remain mainly from non-Chinese supply systems.

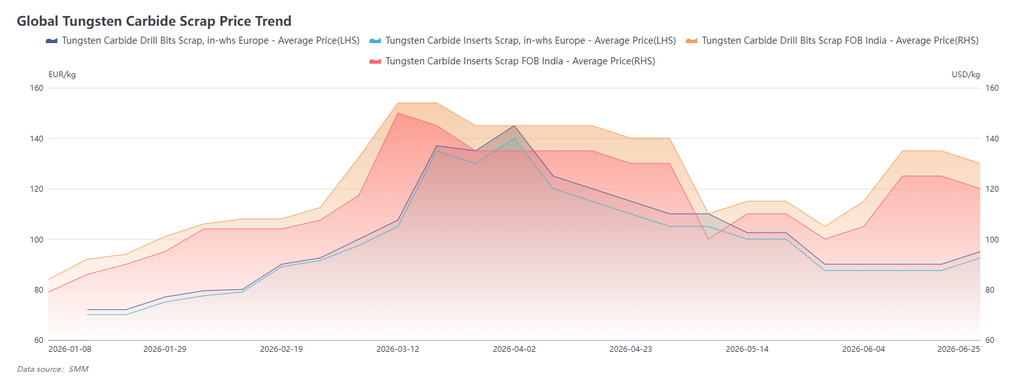

International Tungsten Scrap Market Review in June: India First Rising Then Pulling Back, Europe Building Momentum at Lows

As of July 2, European scrap tungsten alloy inserts were quoted at €90-95/kg, with the average price at €92.5/kg, up by €5 from early June; India scrap tungsten drill bits FOB were quoted at $120-140/kg, with the average price at $130/kg, up by $15 from early June.

In the Indian market, the upward shift in the price center in June was mainly driven by the rapid rise in Chinese tungsten prices, with scrap traders collectively pushing up offers, combined with previously low inventory, leading to active transactions and heated market sentiment in mid-June. On the demand side, sodium tungstate manufacturers procured larger volumes, with good sodium tungstate export orders to terminal markets in Europe, the US, and Japan in June. However, as the Chinese market recently pulled back, Indian scrap prices have cooled slightly.

In European scrap, trader offer divergences were evident. Scrap inventory accumulated from speculative positions when prices were high remained elevated, causing European scrap to consolidate at lows overall in June. In late June, as inventory was gradually cleared, some scrap dealers began to raise offers. As European scrap is expected to replace primary raw materials as the main supply source for local downstream tungsten, European scrap prices are expected to return to high levels in H2 2026.

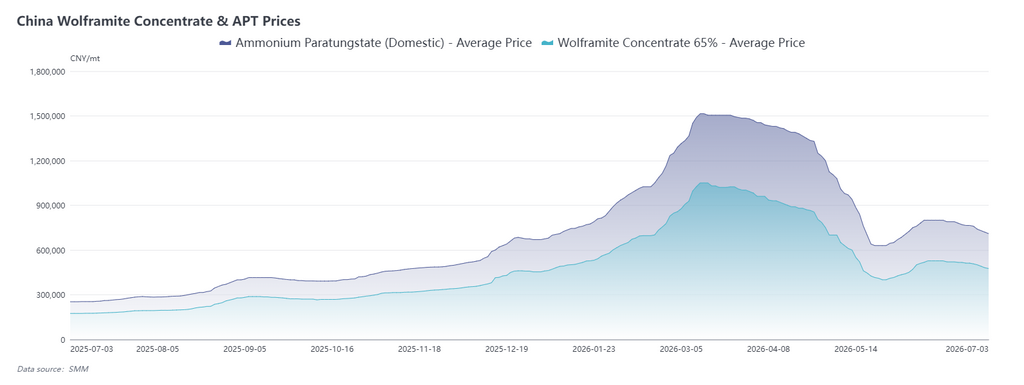

China Tungsten Market June Review: Tungsten Prices Pull Back from Highs After Rapid Rebound, Medium and Long-Term Support Solid

In June, China’s tungsten market went through a full cycle of “rapid rebound – high-level stalemate – weak consolidation”.

At the start of the month, tungsten concentrates rebounded for eight consecutive trading days after the deep correction in May bottomed at 400,000 yuan/standard tonne, with cumulative gains on the ore side exceeding 100,000 yuan/mt; top-tier players raised long-term contract prices in line with spot, boosting market confidence. By mid-June, tungsten concentrates surged to about 520,000 yuan/standard tonne, and APT rose to 800,000 yuan/mt.

The core driver of this round of price increases was the gradual clearance of earlier inventories at the ore side, with the market returning to just-in-time procurement under long-term contracts. Mines in south-west China held back from selling to hold prices firm, while the flooding season in south China constrained mining and transportation, keeping tungsten concentrate circulation relatively tight. Large-scale restocking by end-users has not yet materialized, but active export inquiries in early June provided some boost to demand.

In the second half of June, market momentum weakened as mines continued to release supply, downstream restocking returned to rational levels, and prices shifted to a high-level pullback. As of June 26, tungsten concentrates closed at 512,000 yuan/standard tonne, APT closed at 765,000 yuan/mt, and tungsten carbide powder fell to 1,160 yuan/kg.

On the supply side, from mid-month onward, mine auctions in Shaanxi, Yunnan, Hunan and other regions gradually increased, transactions of medium- and low-grade tungsten concentrates were active, the volume of material circulating in the market rose significantly, and overall industry inventories were in a relatively ample range. On the demand side, sectors such as machining and mold making enter their traditional off-season in July, downstream enterprises face a backlog of finished product inventories, procurement has shifted entirely to small-scale replenishment on an as-needed basis, and a zero-stockpiling strategy dominates the market. On the policy front, the Regulations for the Implementation of the Mineral Resources Law took effect on June 15, listing tungsten as a national-level strategic mineral subject to whole-chain control. On June 22, the Ministry of Commerce added 10 US military-related entities to the export control list, further narrowing export channels for tungsten products to the US. On the trade front, in May, China’s exports of tungsten products totaled 1,063.6 mt (down 17.9% YoY), while imports of tungsten concentrates amounted to 2,060.2 mt (up 50% YoY), continuing the pattern of ‘strong imports and weak exports’.

In the short term, as downstream sectors enter the traditional consumption off-season in July, cemented carbide and machining enterprises will have limited procurement appetite, and the market will continue to undergo weak consolidation following the high-level pullback. However, long-term contract prices will stay high in the second half of the month, providing some support to the bottom. Going forward, the key focus will be on July long-term contract price guidance, the pace of mine shipments, and changes in overseas export policies.

From a medium and long-term perspective, mining controls on primary tungsten mines in China continue to be tightened, demand for cemented carbide remains rigid, and net exports keep increasing, leaving a supply-demand gap for tungsten throughout the year. In Q3, mine quotas will face a transitional shortfall and supply will tighten, while the September-October peak season is expected to drive restocking and a recovery. Rigid demand from military, high-end equipment, and new energy sectors will continue to expand, and the high price spread between domestic and overseas markets will catalyze export expectations, providing solid support for the medium and long-term tungsten price center. However, caution is needed regarding the negative feedback risk of excessively rapid raw material price hikes squeezing downstream profits and forcing end-user production cuts. The tungsten market is expected to return to a mild and orderly uptrend.