SMM News Release, July 3

Domestic molybdenum market saw a trend of correction at the start of June, rally in mid-month and narrow high-level fluctuations at month-end, with mainstream products posting modest gains throughout the month. Tight supply fundamentals remained in constant conflict with sluggish demand from the traditional steel off-season, while the "molybdenum replacing tungsten" theme in the semiconductor sector lifted market sentiment temporarily, keeping prices hovering at multi-year highs.

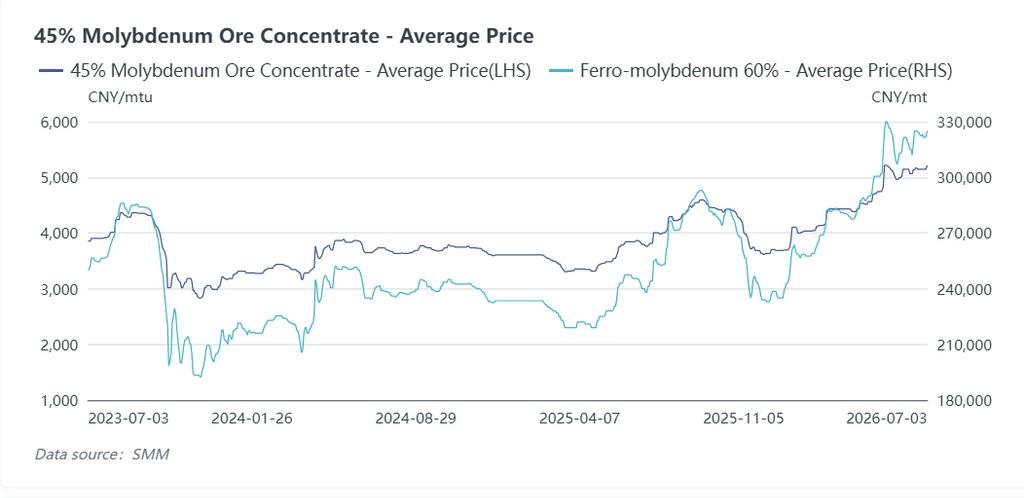

Monthly Price Performance

Over June, 45% molybdenum concentrate rose from 4,995 yuan per Mo unit at the start to 5,145 yuan per Mo unit at month-end, up 3.00% month-on-month at an average of 5,121 yuan per Mo unit. Domestic molybdenum oxide (≥50% Mo) climbed from 5,105 yuan to 5,255 yuan per Mo unit, a 2.94% increase. Imported molybdenum oxide (57% Mo, CIF Tianjin Port) edged up from USD 30.93 to USD 31.35 per lb Mo. 60% ferromolybdenum advanced from 313,000 yuan to 321,500 yuan per metric ton, gaining 2.72% with a monthly average of 320,024 yuan per metric ton. Grade 1 molybdenum powder inched up from 585 to 595 yuan per kg, rising 1.71%.

Phased Market Review

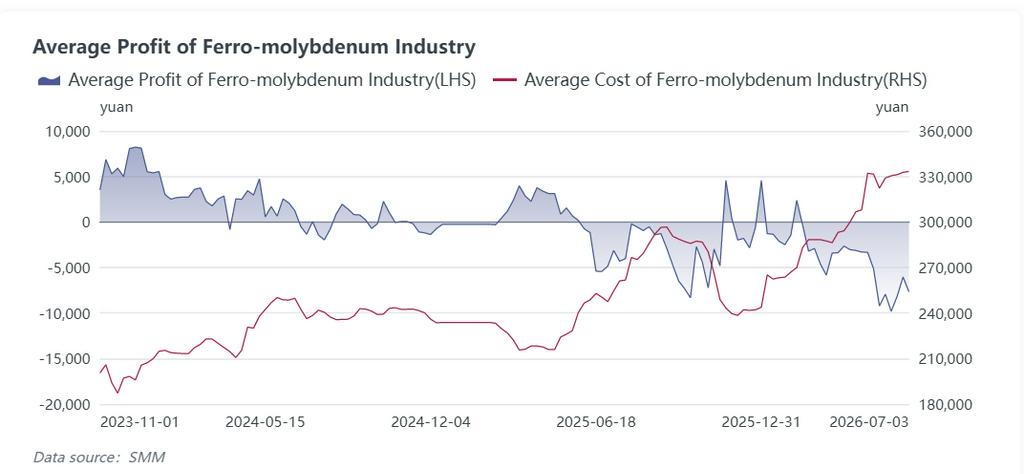

Early June witnessed concentrated auctions held by mines in Henan and Jiangxi, driving auction prices sharply higher. On June 3, 45% molybdenum concentrate jumped 150 yuan per Mo unit to 5,145 yuan per Mo unit, prompting most mines to hold back shipments and tighten spot supply. Prices dipped temporarily between June 11 and 15 on weaker auction bids from Yunnan mines, with 45% concentrate falling to 5,065 yuan per Mo unit. Major mines in Henan held off shipments through the month to keep inventories low, yet ferromolybdenum smelters faced widening cost losses: average weekly losses stood at 7,927 yuan per ton during June 1–5 and expanded to 9,817 yuan per ton June 8–12. Steel mills capped tender prices at 310,700–313,500 yuan per ton, dragging ferromolybdenum down to its monthly low of 312,000 yuan per metric ton.

Mid-June saw large-scale mines across six core producing regions (Henan, Jiangxi, Inner Mongolia, Jilin and Heilongjiang) release material via auctions, with roughly 2,000 tons of physical concentrate traded. Smelters rushed to secure raw materials, lifting 45% concentrate from 5,065 yuan to a monthly peak of 5,165 yuan per Mo unit, while ferromolybdenum hit its monthly high of 325,000 yuan per metric ton.

From June 22 to 30, intensified safety inspections triggered production cuts at molybdenum mines in Henan and Inner Mongolia, again tightening mine supply. SMM data showed domestic molybdenum concentrate output reached 22,900 tons in June, down 4.98% month-on-month from May’s 24,100 tons. May’s molybdenum concentrate imports totalled 7,590.79 tons, a 14.32% month-on-month drop, further limiting external supply sources. Output from copper-molybdenum mines in Chile and Peru fell short of expectations, pushing CIF molybdenum oxide prices up to USD 31.35 per lb Mo and forming mutual price support between domestic and overseas raw material markets. 45% molybdenum concentrate stabilised at 5,145 yuan per Mo unit from June 23 onwards, while ferromolybdenum traded within a narrow band of 321,000–325,000 yuan per metric ton.

Ferromolybdenum Market Breakdown

Cramped by high molybdenum concentrate costs, thin processing fees and persistent selling price losses, domestic ferromolybdenum producers widely cut operating loads in June. The industry average operating rate fell 7–9 percentage points month-on-month versus May with clear regional divergence: major smelters in core producing provinces Henan and Shaanxi ran at half capacity, while medium and small facilities suspended production for maintenance. Small ferromolybdenum plants in East and Southwest China operated at less than 40% capacity.

June marked the traditional off-season for steel consumption amid softer crude steel production. Monthly ferromolybdenum tender volumes from major steel mills totalled 12,600 tons, down 10.7% month-on-month from May and mirroring weaker physical ferromolybdenum demand. Driven by semiconductor optimism early and mid-month, special steel plants stepped up forward fixed-price purchases to lift trading volumes. In late June, high temperatures and mid-year capital repayment pressure slowed steel mill procurement pace. Major steelmakers including Baosteel, HBIS, TISCO, Valin Steel and Shandong Steel opened centralized tenders with uniform price cuts of 500–800 yuan per ton, closing bids at 318,000–320,000 yuan per ton, well below mid-month spot highs.

June Market Summary

In June, supply-side policy curbs and overseas mine disruptions delivered firm price support. On the demand side, traditional steel consumption weakened in the off-season with lower ferromolybdenum tender volumes and muted spot trading. Sustained cost losses forced smelters to curb output and restrict ferromolybdenum circulation, while steel mill price suppression capped upside potential. Ferromolybdenum stood at the centre of cross-market game dynamics, with overall prices locked in high-level narrow volatility with limited swing space.

July Market Outlook

The molybdenum market is expected to maintain narrow high-level fluctuations in July with no sharp unilateral rallies or slumps. Early July auctions of molybdenum concentrate from Jiangxi mines delivered strong underlying support: two batches of 128 tons each went under the hammer, with 40–45% grade concentrate bid at a floor price of 5,160 yuan per Mo unit and closed at 5,210 yuan per Mo unit; 45–50% high-grade concentrate was priced at a floor of 5,190 yuan per Mo unit and settled at 5,280 yuan per Mo unit. All lots traded at premium prices, boosting confidence among mine holders and firming spot quotations to underpin concentrate price floors.

Ferromolybdenum remains trapped in cost inversion amid high raw material costs, with steel mill tender prices mostly ranging from 318,000 to 325,000 yuan per ton. Supply-side constraints including mine regulation and overseas mine disruptions will persist, keeping smelters running at low capacity. High temperatures will weigh on crude steel and regular steel demand in July, alongside modest output declines of 300-series molybdenum-bearing stainless steel. Steel mill ferromolybdenum tender volumes are projected to stay weak at 12,000–12,800 tons, dominated by long-term contract deliveries with thin spot trading activity.

The semiconductor "molybdenum replacing tungsten" catalyst from June has been fully priced in, cooling speculative buying sentiment. Weak manufacturing activity overseas in the off-season fails to lift external molybdenum oxide prices, further limiting upward momentum. Sustained demand from photovoltaics, wind power and semiconductor high-purity molybdenum products provides long-term fundamental resilience to cap downside risks, and overall price volatility will be milder than June.

Significant upside catalysts include unplanned production halts at overseas mines or advance pre-stocking by steel mills ahead of August. Downside risks stem from sharper-than-expected steel demand deterioration and concentrated arrivals of imported molybdenum raw materials triggering spot sell-offs.

Operation Suggestions

- Mine operators: Hold material at low price levels and ship on demand, avoid distress sales.

- Ferromolybdenum smelters: Maintain restricted output, lock long-term steel mill contracts and limit high-cost raw material stocking.

- Steel mills and molybdenum product manufacturers: Make staged purchases on price dips, avoid bulk high-price stockpiling and secure long-term monthly contracts to lock in raw material costs.

![[SMM Analysis] Supply Shocks Support High Molybdenum Prices Downstream Pressure Restricts Upside](https://imgqn.smm.cn/production/admin/news/cn/thumb/RWipd20171024152142.jpeg?imageView2/1/w/176/h/110/q/100)

![Overseas Molybdenum Market Rises Along with Increased Stocking Demand from Domestic Steel Mills, Molybdenum Market Advances [SMM Molybdenum Daily Review]](https://imgqn.smm.cn/usercenter/gKDYO20251217171723.jpeg)