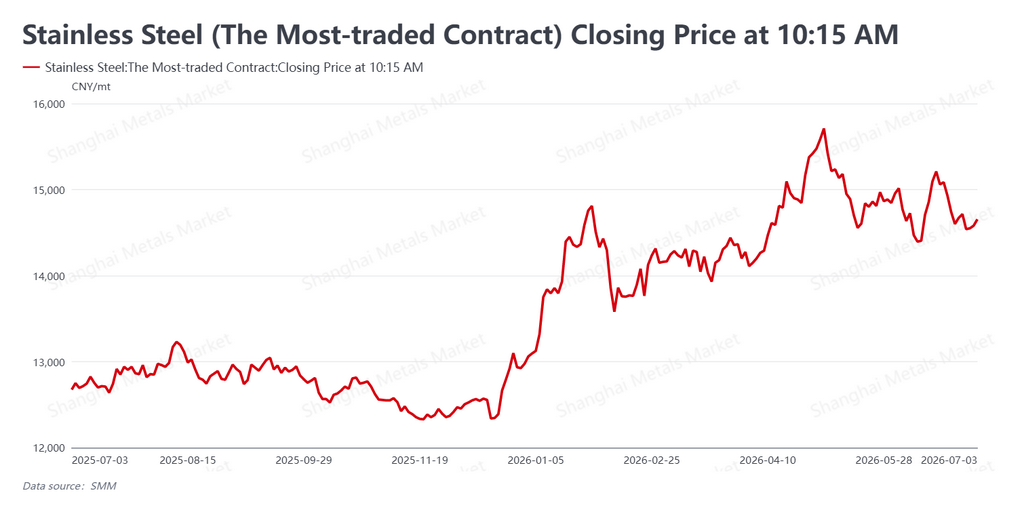

China's most-active stainless steel futures contract (SS2608 on the Shanghai Futures Exchange, SHFE) traded sideways this week, closing on July 3 at roughly $2,162/mt (RMB 14,655/mt), down just RMB 15/mt (about $2) week-on-week, with the RMB 14,500/mt (~$2,139/mt) level holding firmly and no downside break. The defining feature remained a futures-spot divergence: the futures contract lacked upward momentum under the weight of weak nickel, while the physical market stayed relatively firm on mill price support and low inventories.

Macro turned neutral: rate-hike bets slipped, but Chinese factory data cushioned sentiment

Offshore, U.S. June non-farm payrolls came in far below expectations, and markets quickly pushed bets on a Fed rate hike out to year-end; the unemployment rate eased to 4.2%, though the jobs composition was mixed. Fed Chair Kevin Warsh said both near-term inflation expectations and inflation risks had declined, but signaled a clear intent to reduce the balance sheet. Together with softer international oil prices as geopolitical tensions eased, the inflation trade cooled, weighing on commodity valuations broadly. Domestically, June manufacturing PMI rose 0.3 point to 50.3%, back above the 50 expansion line, offering some floor for futures. On balance, macro sentiment was neutral and commodities stayed under pressure.

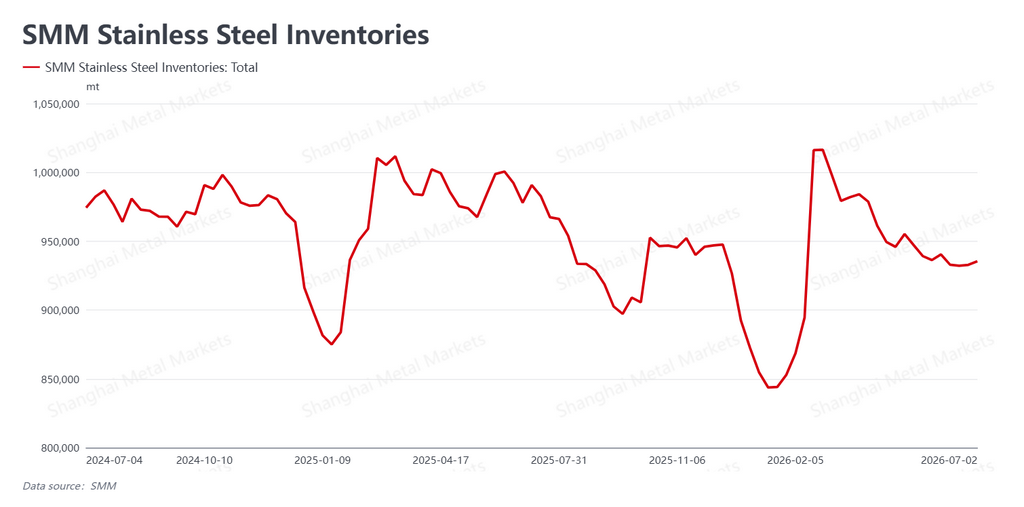

Inventories bottomed and ticked up as the off-season arrived; spot held, but trade thinned

Stainless social inventory (distributor and warehouse stocks) registered 935,400 mt this week, up 2,600 mt week-on-week — halting the prior downtrend and turning to modest accumulation. With the seasonal demand lull now in full swing, the build was still limited and overall inventory pressure remains light, providing a solid floor under spot prices.

Spot resilience rested on three factors:

-

Mill price discipline. Major producers held firm on ex-works prices, locking down spot downside from the mill gate.

-

Controlled restocking. The inventory build, while positive, was contained, leaving limited supply pressure in the market.

-

Tightening supply expectations. A steady stream of maintenance and output-cut news reinforced expectations of marginally tighter availability.

Demand, however, was visibly soft. Off-season end-user demand is naturally thin, with buyers purchasing on a need-only basis, and persistent futures weakness dragged on trading confidence. Traders were keen to destock and move volume, so turnover stayed light — and the demand side's support for prices kept eroding.

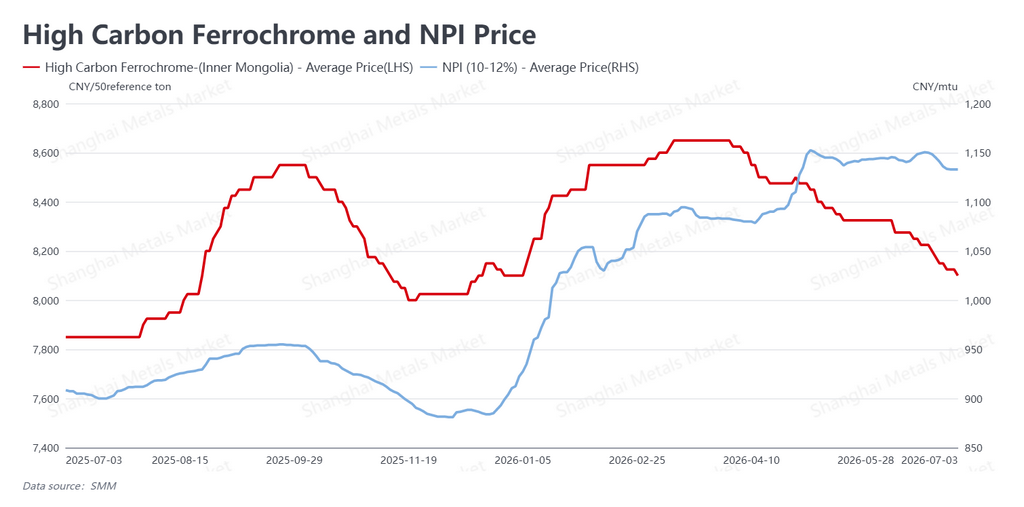

Raw materials kept sliding; nickel weakness was the primary drag

On the cost side, raw-material prices extended their decline and cost support weakened further. High-carbon ferrochrome was quoted at roughly $1,195/mt (RMB 8,100/mt, on a 50% Cr basis), down RMB 50 (~$7); high-grade Nickel Pig Iron (NPI) came in at about $167 per nickel unit (RMB 1,133 per nickel unit — i.e., per 1% nickel content), down RMB 8 (~$1). With both chrome and nickel alloys softening in tandem, the raw-material floor under stainless steel thinned.

On nickel specifically, Indonesia's supplementary ore mining quota (part of the RKAB approval system that governs how much laterite ore miners may extract) remained unresolved, yet the market's dominant concern was still ample nickel supply ahead. SHFE nickel traded in a low range and failed to stage a meaningful rebound, making it the chief external force capping SS futures. On the supply side, while maintenance and output-cut chatter continued and industry output edged lower, the cuts were limited: the sector's high-supply structure is fundamentally unchanged, and loose medium-to-long-term supply remains the main factor holding back any upward shift in the price center.

Outlook

For the week, the stainless steel board was range-bound with its center holding steady, caught in a two-way tug-of-war between weak nickel and a softening off-season on one side and mill price support and low inventories on the other — and the futures-spot divergence looks set to continue. Looking ahead, progress on Indonesia's ore quota and whether SHFE nickel can stabilize are the key external variables for both the cost side and the near-term direction of SS futures.

Domestically, the market has now fully entered its seasonal lull: end-user rigid demand is weak and turnover is thin, so whether spot can stay firm hinges on the persistence of mill price discipline and maintenance-related cuts. June's return to PMI expansion provides a macro floor, but transmission to actual stainless end-demand will take time. We expect the most-active contract to remain range-bound in the near term, with support and off-season pressure trading blows repeatedly, and marginal shifts in nickel and raw materials setting the tempo. Industry participants are advised to view nickel and macro noise rationally, watch closely for the landing of Indonesia's ore quota, the real pace at which off-season demand weakens, and the durability of mill maintenance cuts — and to maintain a steady, disciplined approach.

Written by Bruce Chew

Nickel & Stainless Steel Analyst, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088

![[SMM Analysis] Nickel and Cobalt Salt Prices Weak; Intermediate Product Payables Under Pressure](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)

![[SMM Analysis] Indonesia's nickel ore HMA sharply cut by 7.6%, high inventories in China and Indonesia suppress nickel ore market sentiment](https://imgqn.smm.cn/usercenter/vcoVV20251217171732.jpeg)