With continued growth in electric vehicles (EVs), energy storage systems (ESS), and consumer electronics, the global installed base of lithium-ion batteries has expanded rapidly, resulting in a steady increase in end-of-life batteries and driving the development of the battery recycling industry. As more battery scrap and black mass become available overseas, China's role as the world's largest battery recycling and hydrometallurgical processing market has made overseas black mass an increasingly important source of feedstock.

Greater Linkage Between China's Domestic and Overseas Black Mass Markets

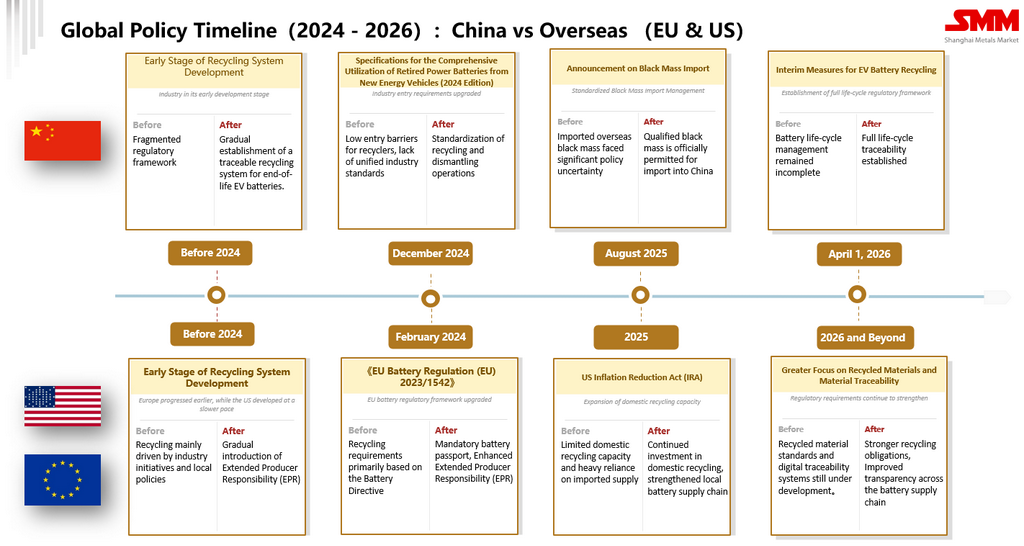

In August 2025, China officially reopened imports of qualified overseas black mass. At the time, the market widely expected lower-cost overseas material to supplement feedstock supply for domestic hydrometallurgical recyclers and significantly increase imports into China.

Nearly one year later, however, the market has evolved differently from initial expectations.

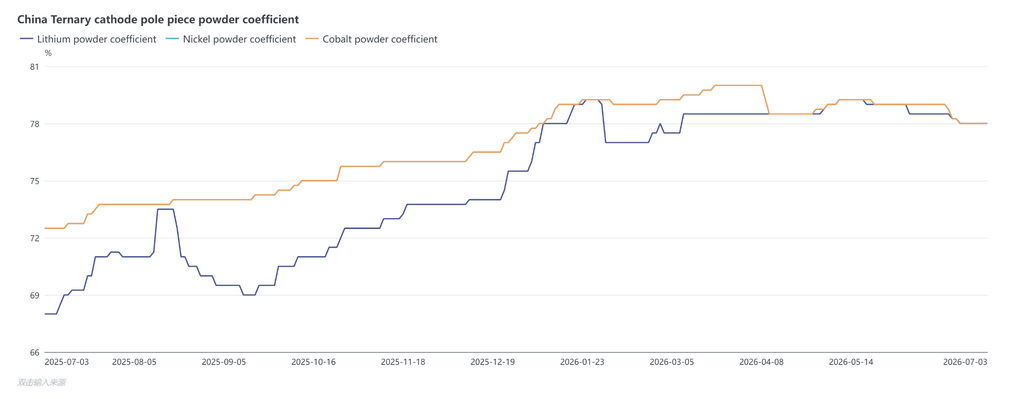

According to SMM, domestic ternary black mass payables have remained relatively firm since the policy was introduced, while Malaysia FOB payables rose during the initial months following the reopening before gradually trending lower in line with fluctuations in nickel, cobalt and lithium salt prices. Compared with the period before imports were reopened, overseas and domestic black mass markets have become increasingly interconnected.

Market participants noted that as more Chinese companies source black mass from Malaysia, local transactions have gradually shifted toward referencing China's ternary black mass payable system. Final purchasing prices are increasingly determined by adjusting domestic Chinese payables for ocean freight, logistics, import duties, financing costs and other cross-border expenses. As Chinese demand has grown, domestic pricing has become an important benchmark for part of the Malaysian market.

However, this trend is primarily observed in transactions involving Chinese buyers. Globally, no unified pricing mechanism for black mass currently exists. In Europe, the United States and South Korea, black mass is still commonly priced under a two-metal pricing model, where value is mainly calculated based on international nickel and cobalt prices, with lithium value already embedded within the overall payable rather than priced separately. By contrast, transactions involving Chinese buyers are increasingly adopting China's three-metal pricing model, in which lithium, nickel and cobalt are valued individually before logistics, tariffs and other cross-border costs are incorporated into the final purchase price. As Chinese companies continue expanding overseas procurement, both pricing systems are expected to coexist and serve different markets and trading relationships.

Water-Soluble Fluorine Remains a Key Constraint on Import Growth

Despite the reopening of imports, one of the biggest challenges limiting larger import volumes remains the water-soluble fluorine specification.

Black mass is the powder generated after spent lithium-ion batteries are discharged, dismantled, shredded and mechanically separated. It contains valuable metals such as lithium, nickel, cobalt and manganese, making it the primary feedstock for hydrometallurgical recovery. However, black mass also contains residual fluorine compounds, mainly originating from lithium hexafluorophosphate (LiPF₆) in the electrolyte and polyvinylidene fluoride (PVDF) used as the electrode binder. During battery dismantling and shredding, these fluorine-containing materials enter the black mass stream and may form water-soluble fluorides.

When water-soluble fluorine exceeds China's import specifications, black mass cannot be directly imported. As a result, fluorine removal has become one of the industry's major areas of technological development.

Many companies are actively developing defluorination technologies to meet China's import requirements. However, commercial deployment requires more than simply meeting product specifications. Process stability, metal recovery efficiency, operating costs and environmental compliance must also be considered. If fluorine removal remains expensive, the original cost advantage of overseas black mass could be significantly reduced.

Overseas Intermediate Processing Emerges as an Alternative Route

Against this backdrop, another cross-border supply chain model has begun attracting industry attention.

Instead of exporting black mass directly, some companies are choosing to complete battery dismantling, black mass production and initial hydrometallurgical processing overseas, converting black mass into intermediate products such as mixed nickel-cobalt carbonate before shipping them to China. Domestic refiners then carry out further refining to produce battery-grade materials.

Compared with direct black mass imports, this approach reduces exposure to black mass import restrictions while leveraging China's well-established hydrometallurgical refining capacity. It effectively creates a supply chain in which preliminary resource recovery is completed overseas and high-value refining remains in China.

Malaysia provides one example of this emerging model. If intermediate products satisfy ASEAN Rules of Origin requirements and obtain the relevant certificates of origin, they may qualify for preferential tariff treatment when exported to China under applicable ASEAN-China trade agreements, reducing overall cross-border costs and improving supply chain competitiveness. Compared with building a fully integrated hydrometallurgical operation overseas, this model may also reduce uncertainties related to environmental approvals, policy changes and long-term operational management.

Direct Black Mass Imports and Overseas Intermediate Processing May Coexist

Industry participants generally believe that overseas intermediate processing is unlikely to replace direct black mass imports entirely. Instead, both models are expected to coexist over the long term.

Should defluorination technologies become commercially mature and consistently satisfy China's import specifications, direct imports of overseas black mass could regain stronger cost competitiveness and provide additional feedstock options for Chinese recyclers.

More broadly, as global volumes of end-of-life lithium-ion batteries continue to increase, competition within the recycling industry is expanding beyond recycling technology itself. Access to overseas resources, cross-border supply chain integration and commercially viable business models are becoming increasingly important competitive advantages. Whether the industry ultimately favours direct black mass imports or a combination of overseas intermediate processing and domestic refining, companies capable of establishing stable, efficient and economically sustainable global recycling networks are likely to be best positioned for future growth.

![[SMM Analysis] China’s Sulphuric Acid Production and Sulphur/Sulphuric Acid Imports & Exports in H1 2026](https://imgqn.smm.cn/usercenter/OpmKJ20251217171712.jpg)

![H1 Battery Materials Import and Export Data Released, Lithium Carbonate Imports Surge over 50%, How About Other Segments? [SMM Special]](https://imgqn.smm.cn/usercenter/JmyWy20251217171729.png)

![Lithium Carbonate Market Weekly Review: Jul 20-23 Spot Lithium Carbonate Prices Moved Sideways in a Narrow Range [SMM Weekly Review]](https://imgqn.smm.cn/usercenter/WyqWW20251217171729.jpg)