SMM, le 3 juillet – Actualités :

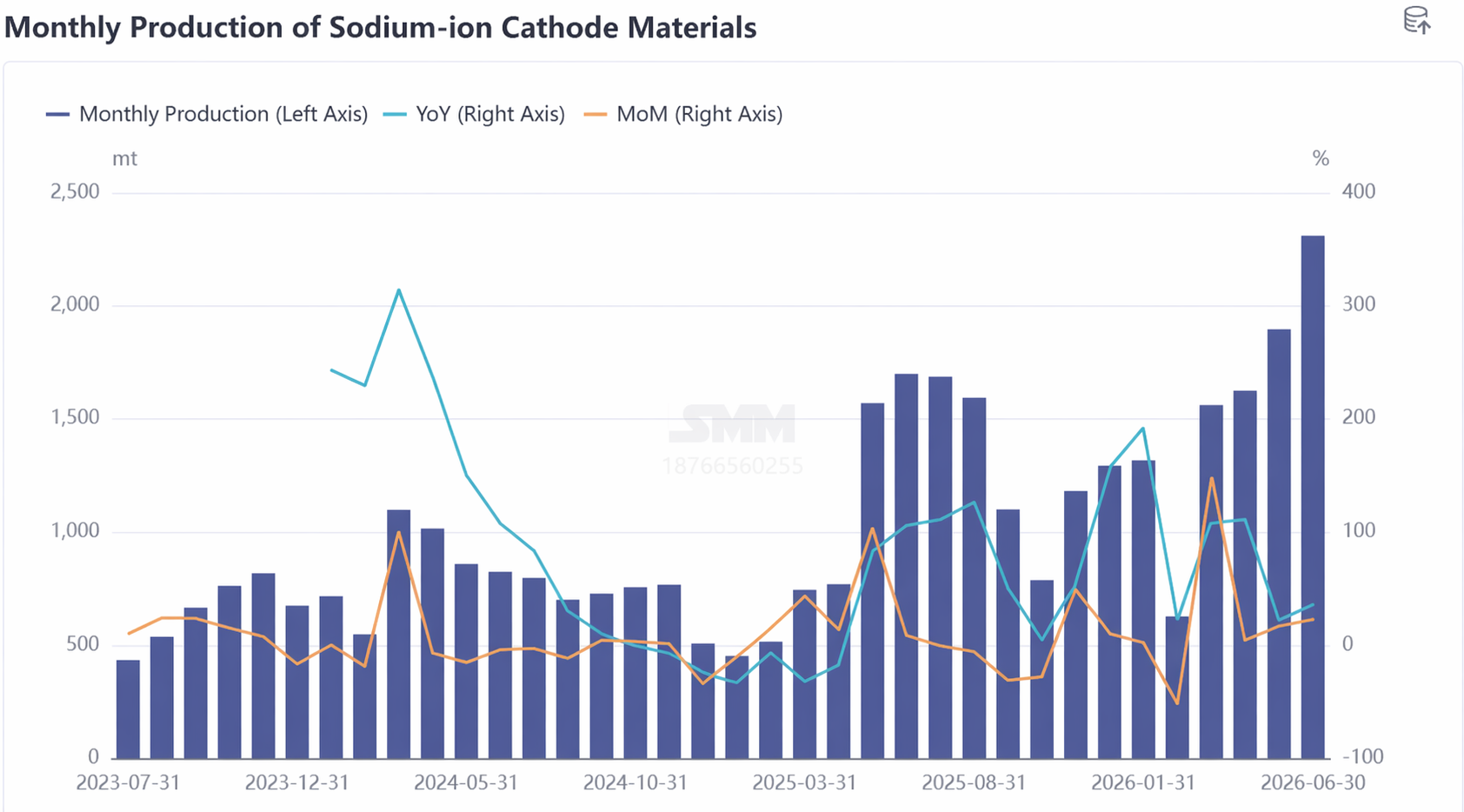

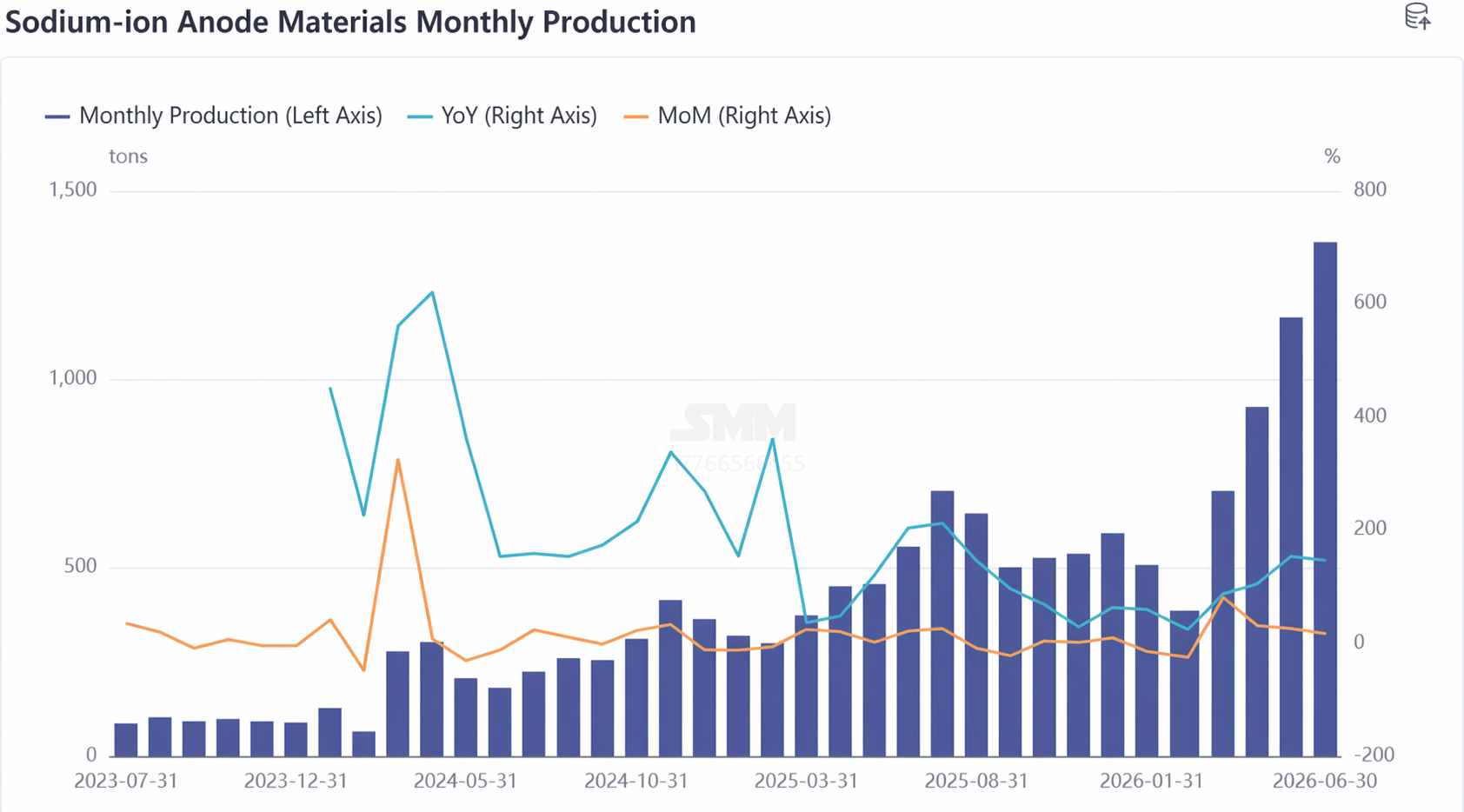

En juin, la chaîne industrielle de la batterie sodium-ion (ci-après "sodium battery") a affiché une forte dynamique. La demande finale continue de se libérer et de se transmettre en amont, entraînant une forte croissance des matériaux de cathode et des anodes en carbone dur, ce qui accentue encore la tension entre l'offre et la demande. Les données de SMM montrent que la production de cathodes pour batteries sodium a augmenté de 22 % en glissement mensuel et celle d'anodes en carbone dur de 17 % en glissement mensuel, tandis que le rythme d'expansion de l'offre peine toujours à suivre la croissance de la demande, ce qui traduit clairement un marché vendeur.

I. Matériaux de cathode : la sous-offre persiste, des tensions sur l'écart se profilent au second semestre

En juin, la production de matériaux de cathode pour batteries sodium a augmenté de 22 % en glissement mensuel et de 36 % en glissement annuel. En termes de structure de produit, la voie polyanionique est restée dominante, représentant jusqu'à 82 %, en écho direct à la demande robuste pour le stockage d'énergie sodium-ion.

La contradiction la plus marquante sur le marché des cathodes est la grave sous-offre. Les principaux acteurs ont dans l'ensemble maintenu une production et des ventes à pleine capacité, les stocks de produits finis tombant à des niveaux extrêmement bas ; certaines entreprises ne peuvent approvisionner en priorité que leurs clients clés. Cela a déjà entraîné des relances de livraison au niveau des cellules de batterie en aval.

Du point de vue du paysage concurrentiel, la cathode pour batterie sodium en est encore à un stade précoce de commercialisation. Seule une poignée d'entreprises est capable de réaliser des expéditions à grande échelle, et le total mensuel des expéditions du secteur reste de quelques centaines de tonnes, sans avoir encore franchi le cap des milliers de tonnes. Cette configuration suggère que les fournisseurs de cathodes conserveront un fort pouvoir de négociation à court terme.

Pour le second semestre, le déséquilibre offre-demande pourrait s'intensifier. À la charnière entre le premier et le deuxième semestre, les fabricants de cellules en aval ont déjà transmis leurs prévisions de demande pour le second semestre en amont. La demande se libérant de manière concentrée au second semestre, SMM s'attend à ce que la situation tendue de l'offre de cathodes persiste, avec de possibles écarts offre-demande périodiques dans certains segments.

Le côté des coûts est également sous pression. En juin, les coûts des matières premières pour le NFPP (phosphate de fer sodique) ont continué de grimper, les prix du phosphate de fer augmentant sans cesse. Les producteurs de phosphate de fer en amont proposent désormais d'utiliser le prix SMM du phosphate de fer comme référence de règlement, tandis que les fabricants de cathodes NFPP prévoient de répercuter les coûts en aval sur les fabricants de cellules via une tarification basée sur une formule. Cette mesure devrait établir un mécanisme de répercussion des coûts plus contrôlable et favoriser un cycle commercial vertueux dans la chaîne industrielle. Dans ce contexte, les prix des cathodes NFPP ont clairement augmenté en juin.

En revanche, la cathode à oxyde lamellaire reste tiède, et les progrès de l'intégration dans les véhicules doivent s'accélérer. Cependant, avec le lancement potentiel de modèles de véhicules adoptant la voie de l'oxyde lamellaire au second semestre, cette voie devrait prendre de l'ampleur en volume.

Perspectives de juillet : l'amélioration de la demande se poursuit, les programmes de production devraient encore augmenter. SMM s'attend à ce que la production de cathodes pour batteries sodium progresse de 8 % en glissement mensuel et de 47 % en glissement annuel en juillet.

II. Anode en carbone dur : la libération de capacité s'accélère, la pénurie de produits haut de gamme persiste.

En juin, le marché des anodes en carbone dur pour batteries sodium-ion a continué de connaître une offre insuffisante, avec une production en hausse de 17 % en glissement mensuel et bondissant de 145 % en glissement annuel, maintenant une forte dynamique de croissance.

Côté offre, l’industrie fonctionnait globalement avec des stocks très bas, les produits finis étant expédiés immédiatement après leur production et les cycles de stock de sécurité étant minimaux, ce qui confirme indirectement une demande soutenue et vigoureuse. Parallèlement, de nouveaux entrants accéléraient la mise en service et la montée en puissance de leurs lignes de production, et une offre supplémentaire est en route.

Côté demande, les signaux sont positifs. Au second semestre, l’échelle d’achat des anodes par les entreprises de batteries lithium devrait atteindre le niveau du kilotonne ou plus, avec des progrès d’engagement susceptibles de réaliser des percées substantielles au second semestre, ce qui stimulera ensuite une nouvelle croissance des volumes sur le marché des anodes.

Du point de vue du paysage concurrentiel, contraint par les capacités, le marché des anodes en carbone dur présente clairement des caractéristiques de marché vendeur. Notamment, des changements subtils sont en cours dans l’industrie : certaines entreprises en amont ont commencé à nouer des relations de fidélisation avec les acteurs en aval pour verrouiller les volumes d’approvisionnement et les droits de priorité. En raison de capacités insuffisantes, le traitement à façon augmente progressivement, mais le problème de l’irrégularité des normes de contrôle qualité sous ce modèle émerge également, ce qui affecte dans une certaine mesure la pleine expression de la qualité des produits en carbone dur et les performances des cellules de batterie.

Perspectives de juillet : Les attentes de croissance des volumes du marché de juillet à août sont claires, avec une confiance sectorielle relativement suffisante. Cependant, la configuration d’offre tendue pour les produits haut de gamme pourrait persister, et les entreprises dotées de capacités de modernisation des procédés et d’un contrôle qualité stable devraient s’assurer des positions plus avantageuses dans le cycle haussier actuel. SMM s’attend à ce que la production d’anodes en carbone dur augmente de 13 % en glissement mensuel et de 119 % en glissement annuel en juillet.

III. Résumé : Le déséquilibre offre-demande persiste, la chaîne industrielle face à une fenêtre de croissance

Dans l’ensemble, la chaîne industrielle des batteries sodium-ion a connu une forte prospérité en juin, le déséquilibre offre-demande persistant tant du côté des cathodes que des anodes. L’expansion des capacités en amont s’accélère, mais elle peine encore à satisfaire la libération concentrée de la demande en aval à court terme, indiquant clairement un marché vendeur.

Côté coûts, la pression se déplace progressivement vers l’amont, et les mécanismes de tarification s’orientent davantage vers le marché, ce qui est propice à une répartition plus équilibrée des bénéfices tout au long de la chaîne industrielle. Au second semestre, avec le possible lancement et la livraison de modèles de voitures à batteries sodium-ion, l’accélération des appels d’offres pour les projets de stockage d’énergie, et la finalisation des achats à grande échelle par les entreprises de batteries lithium, la chaîne industrielle des batteries sodium-ion devrait entrer dans une période clé de libération accélérée de la demande. Durant cette phase, les entreprises disposant d’une mise en œuvre de montée en capacité, d’un contrôle qualité stable et de capacités de répercussion des coûts prendront l’initiative de percer dans un paysage concurrentiel en recomposition.

Équipe de recherche SMM en énergies nouvelles

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lyu Yanlin 021-20707875

![[Briefing matinal SMM Cobalt] La faiblesse de la chaîne du cobalt persiste, le réapprovisionnement au T3 reste à voir.](https://imgqn.smm.cn/usercenter/cgspx20251217171725.jpg)

![[Compte-rendu de la réunion matinale SMM Cobalt-Lithium] Les prix des matériaux pour batteries divergent ; les achats des utilisateurs finaux restent prudents.](https://imgqn.smm.cn/usercenter/MbKXH20251217171730.jpg)