SMM July 3 News:

In June, the sodium-ion battery (hereinafter "sodium battery") industry chain showed robust momentum. End-use demand continued to be released and transmitted upstream, leading to high growth for both cathode materials and hard carbon anodes, further intensifying the tight supply-demand situation. SMM data show that sodium battery cathode production increased 22% MoM and hard carbon anode production increased 17% MoM, while the pace of supply expansion still struggled to match demand growth, reflecting a clear seller's market.

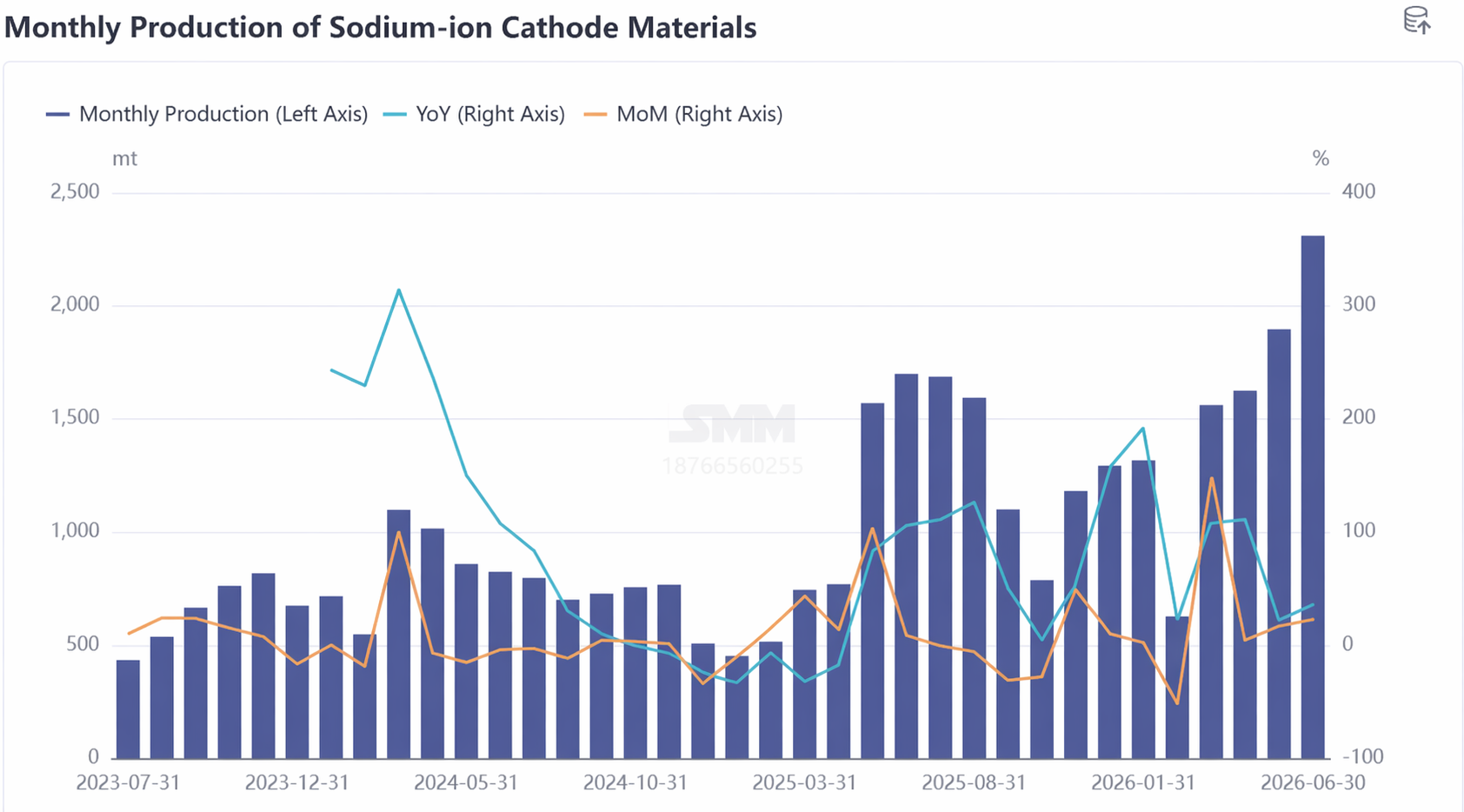

I. Cathode Materials: Undersupply Persists, H2 Gap Pressure Emerging

In June, sodium battery cathode material production increased 22% MoM and 36% YoY. In terms of product structure, the polyanion route remained dominant, accounting for as much as 82%, directly echoing the robust demand for sodium-ion energy storage.

The most prominent contradiction in the cathode market is severe undersupply. Top-tier players have largely maintained full production and sales, with finished product inventories falling to extremely low levels; some enterprises can only prioritize supply to key clients. This has already led to delivery urging at the downstream battery cell segment.

From a competitive landscape perspective, the sodium battery cathode is still in the early stage of commercialization. Only a handful of enterprises are capable of large-scale shipments, and the industry's total monthly shipments remain in the hundreds of tonnes, without yet achieving a breakthrough to the thousand-tonne level. This landscape suggests that cathode suppliers will maintain strong bargaining power in the near term.

Looking ahead to H2, the supply-demand imbalance may intensify further. Now at the transition between H1 and H2, downstream battery cell enterprises have already transmitted their H2 demand forecasts upstream. As demand is released in a concentrated manner in H2, SMM expects the tight cathode supply situation to persist, with possible periodic supply-demand gaps in certain segments.

The cost side is also under pressure. In June, raw material costs for NFPP (sodium iron phosphate) continued to climb, with iron phosphate prices rising persistently. Upstream iron phosphate producers have now proposed using the SMM iron phosphate price as the settlement benchmark, while NFPP cathode plants plan to pass costs downstream to battery cell manufacturers via formula-based pricing. This move is expected to establish a more controllable cost pass-through mechanism and foster a virtuous commercial cycle in the industry chain. Against this backdrop, NFPP cathode prices clearly increased in June.

In contrast, the layered oxide cathode remains lukewarm, and progress in vehicle installation needs to accelerate. However, with potential car models adopting the layered oxide route being launched in H2, this route is expected to gain volume momentum.

July Outlook: Demand improvement continues, with production schedules expected to increase further. SMM expects sodium battery cathode production to rise 8% MoM and 47% YoY in July.

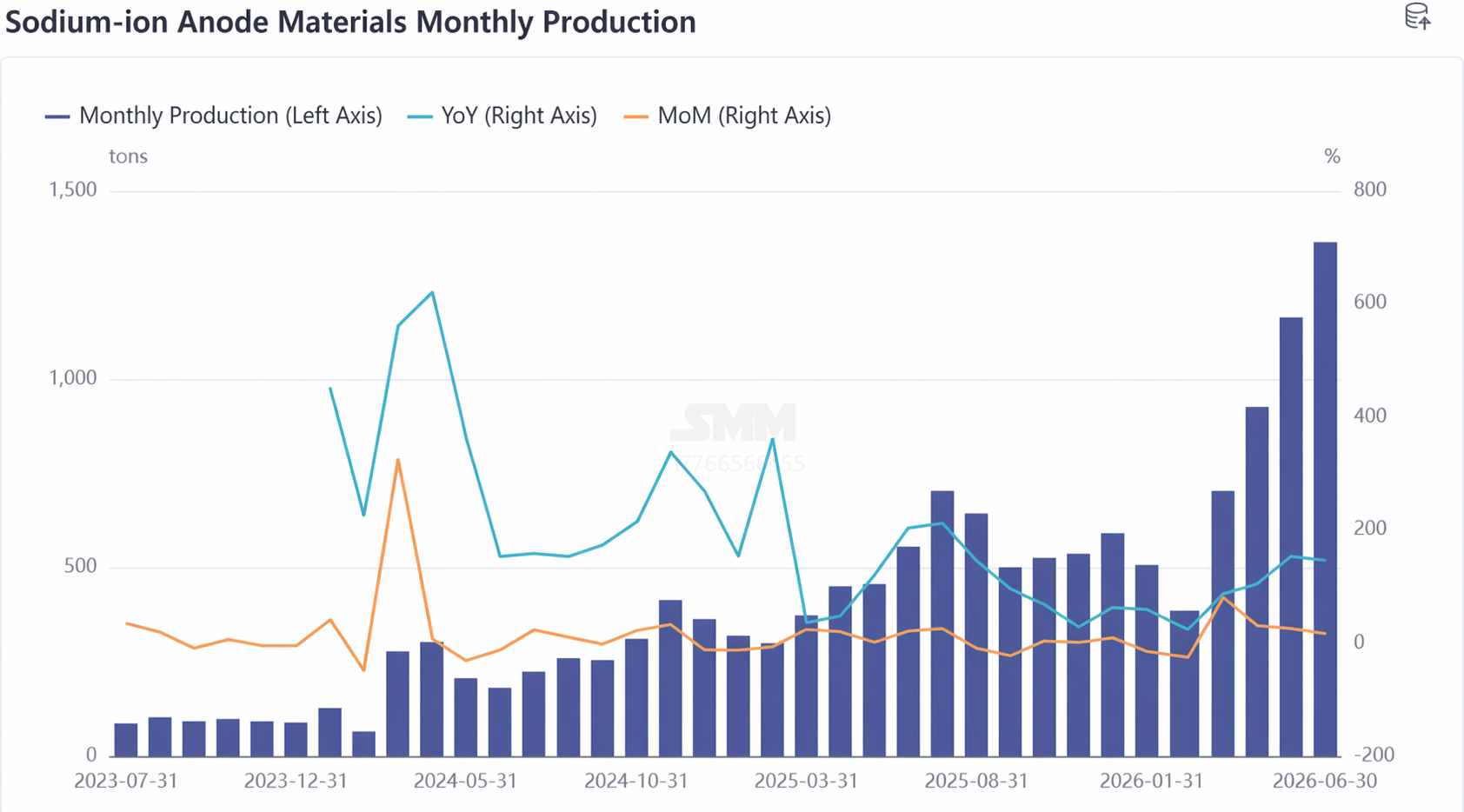

II. Hard Carbon Anode: Capacity Release Accelerates, High-End Product Shortage Persists

In June, the sodium-ion battery hard carbon anode market continued to see undersupply, with production up 17% MoM and surging 145% YoY, maintaining robust growth momentum.

Supply side, the industry operated with extremely low inventory overall, with finished products shipped immediately after completion and minimal safety stock cycles, indirectly confirming sustained strong demand-side pull. Meanwhile, new entrants are accelerating line commissioning and ramp-up, and incremental supply is on the way.

Demand side, signals are positive. In H2, lithium battery enterprises' anode procurement scale is expected to reach kt level or above, with relevant engagement progress likely to achieve substantial breakthroughs in H2, which will then drive further volume growth in the anode market.

From the competitive landscape perspective, constrained by capacity, the hard carbon anode market shows clear seller's market characteristics. Notably, subtle changes are taking place within the industry: some upstream enterprises have begun forming client binding relationships with downstream players to lock in supply volume and priority supply rights. Due to insufficient capacity, toll processing is gradually increasing, but the issue of uneven quality control standards under the tolling model is also emerging, which to some extent affects the full release of hard carbon product quality and battery cell performance.

July Outlook: Market volume growth expectations from July to August are clear, with relatively sufficient industry confidence. However, the tight supply pattern for high-end products may persist, and enterprises with process upgrade capabilities and stable quality control are expected to secure more advantageous positions in the current upcycle. SMM expects hard carbon anode production to increase 13% MoM and 119% YoY in July.

III. Summary: Supply-Demand Mismatch Persists, Industry Chain Faces Growth Window

Overall, the sodium-ion battery industry chain saw high prosperity in June, with supply-demand mismatch persisting on both cathode and anode sides. Upstream capacity expansion is accelerating, but it still struggles to meet the concentrated release of downstream demand in the short term, clearly indicating a seller's market.

Cost side, pressure is gradually moving upstream, and pricing mechanisms are becoming more market-oriented, which is conducive to a more balanced profit distribution along the industry chain. In H2, with the possible launch and delivery of sodium-ion battery car models, accelerated tendering for energy storage projects, and finalized large-scale procurement by lithium battery enterprises, the sodium-ion battery industry chain is expected to enter a key window period of accelerated demand release. During this stage, enterprises with capacity scale-up implementation, stable quality control, and cost pass-through capabilities will take the lead in breaking through amid reshaping competitive landscape.

SMM New Energy Research Team

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lyu Yanlin 021-20707875

![[Lithium Battery: Samsung SDI Plans Battery Lines For Solid-State, LFP, Sodium]](https://imgqn.smm.cn/usercenter/cTxNb20251217171727.jpg)

![[SMM Cobalt Morning Brief] Cobalt intermediate product quotations firm, cobalt salt stabilizes, restocking cautious](https://imgqn.smm.cn/usercenter/ChqBy20251217171724.jpeg)