Iron ore prices followed an initial rise and subsequent decline this week, with the price center shifting further lower. The core drivers were that after the ninth round of coke price cuts was implemented, steel mill losses widened further. Combined with expectations of environmental protection-driven production restrictions in some regions, blast furnace maintenance plans increased, hot metal production continued to pull back, and the demand side was clearly under pressure. In terms of supply, global iron ore shipments and China’s port arrivals both increased MoM, with supply-side pressure intensifying somewhat and further weighing on ore prices. During the week, market talk that benchmark negotiations might restrict low-grade ore port cargo pick-up pushed futures to a short-term rebound. However, the market broadly viewed the probability of this measure actually being implemented as low, and after sentiment was released, price logic returned to a demand-led mode. Affected by this, spot prices performed weaker than futures. In port spot cargoes, the weekly average of the MMI 61% index slipped 5 yuan/mt MoM.

Chart: MMI 61% Port Spot Index

Source: SMM

The domestic iron ore concentrate market edged lower this week, with regional divergence in performance. Prices remained basically stable in Tangshan, Qian’an, and Qianxi in Hebei. Areas such as Chaoyang, Beipiao, and Jianping in western Liaoning edged down by 5-10 yuan/mt. East China saw a pullback of 10-15 yuan/mt. Overall domestic ore production remained steady, but the resource landscape diverged by region. Supply in Hebei remained somewhat tight; within this, the Chengde area saw a further contraction in resource supply due to a mining accident, which provided some support to local iron ore concentrate prices. On the demand side, hot metal production at steel mill blast furnaces remained at a high level, still offering support to iron ore concentrate demand. However, steel mill profits have narrowed significantly recently, and the overall desire to bargain down prices is strong, causing local iron ore concentrate prices to edge down slightly.

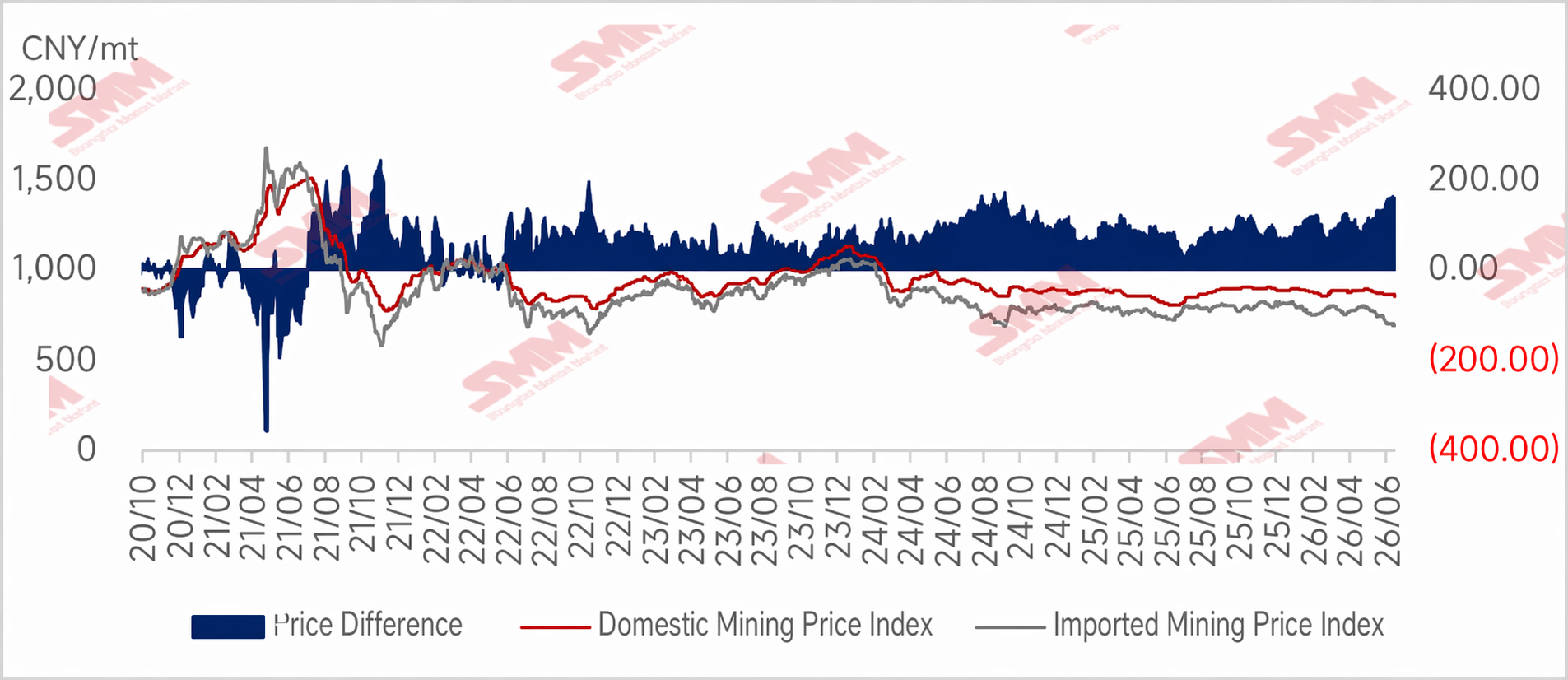

Chart: Tight Domestic Ore Supply Supports Prices — Domestic vs. Imported Ore Price Spread to Widen Further Next Week

Outlook for Next Week

Looking ahead to next week, the probability of the 10th round of coke price increases being implemented is relatively high. Increasing steel mill maintenance resulting from losses will lead to a larger decline in hot metal production. Iron ore demand will continue to deteriorate. Meanwhile, mines will push shipments in June, and imported ore port arrivals still have upside room over the next two weeks, leading to a slight accumulation in port inventories. In addition, a new round of talks between the US and Iran is scheduled for mid-month, and crude oil prices still face downside expectations, so iron ore shipping costs will remain weak. Iron ore prices will remain under pressure. However, considering the disturbance from benchmark negotiation news, there may be opportunities for a price rebound. Overall, iron ore prices are expected to remain in the doldrums next week. Domestically, the tight iron ore supply situation is expected to be difficult to alleviate. But given that demand for iron ore concentrates has weakened somewhat, steel mills’ push for lower prices will continue to dominate. The game between sellers and buyers continues. Overall, the domestic iron ore market is expected to be in the doldrums next week, but the decline may be smaller than that for imported ore.

![[SMM Steel] Turkish Rebar Prices Fall Amid Weak Demand as Buyers Remain Sidelined](https://imgqn.smm.cn/usercenter/LMnqz20251217171717.jpg)

![Stainless Steel Costs and Prices Pull Back Synchronously, Steel Mill Profits Remain Basically Stable [SMM Analysis]](https://imgqn.smm.cn/usercenter/SEwWP20251217171716.jpg)