SMM July 3 News:

In the metals market:

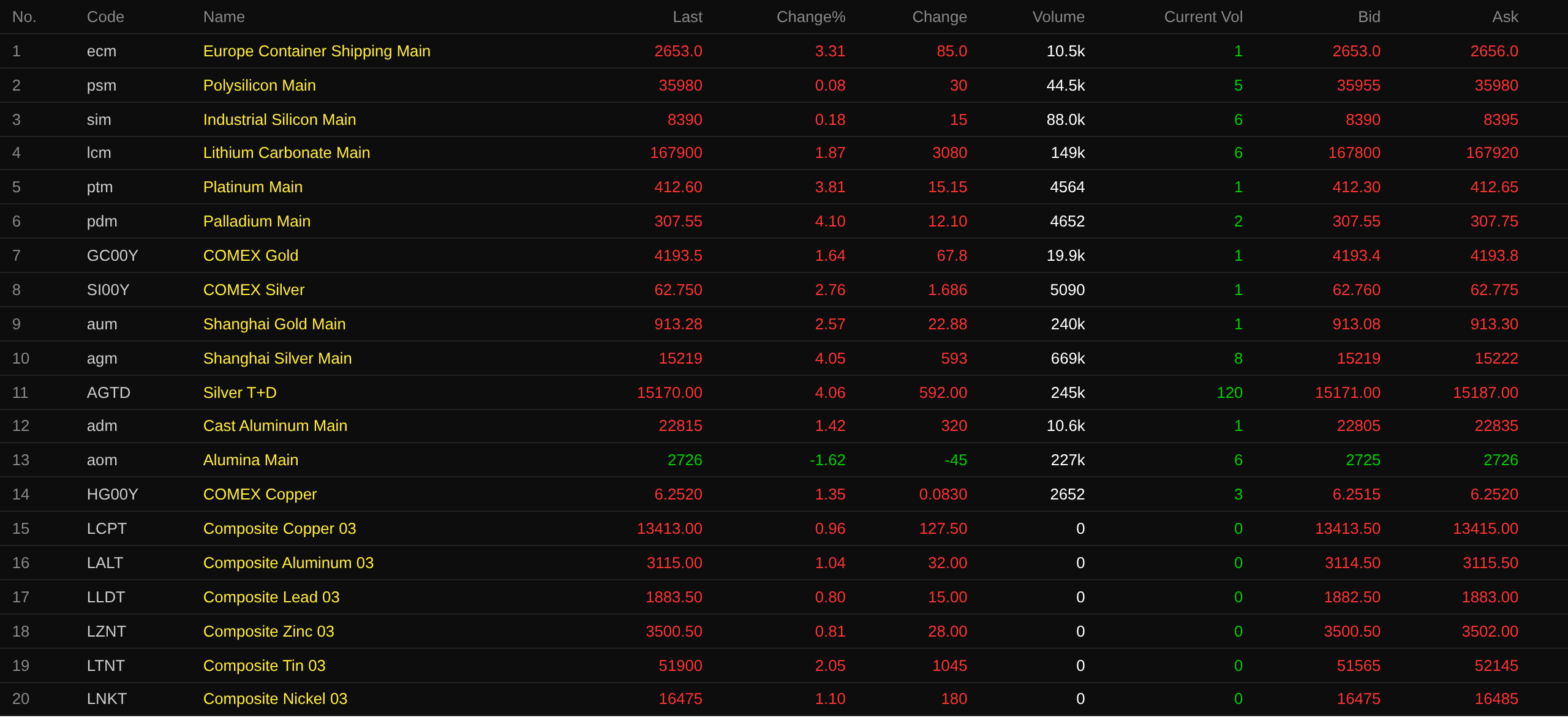

As of the midday close, most domestic base metals rose. SHFE copper gained 0.76%, SHFE aluminum rose 1.45%. SHFE lead advanced 0.47%. SHFE zinc edged down 0.02%. SHFE tin climbed 0.66%. SHFE nickel increased 0.59%.

Additionally, the most-traded cast aluminum futures rose 1.42%, while the most-traded alumina fell 1.62%. The most-traded lithium carbonate futures rose 1.87%. The most-traded silicon metal futures gained 0.18%. The most-traded polysilicon futures edged up.

Ferrous metals mostly fell. Iron ore declined 1.41%. HRC, rebar, and stainless steel all fell within 0.4%. In the coking coal and coke markets, the most-traded coking coal contract rose 1.58%, and the most-traded coke contract rose 1.89%.

In overseas base metals, as of 11:46, LME metals rose across the board. LME copper gained 0.96%, LME aluminum rose 1.04%, LME lead advanced 0.8%. LME zinc increased 0.81%, LME tin climbed 2.05. LME nickel rose 1.1%.

In precious metals, as of 11:46, COMEX gold rose 1.64%, and COMEX silver gained 2.76%. In domestic precious metals, SHFE gold advanced 2.67%, and the most-traded SHFE silver futures contract surged 4.05%.

Strategists at OCBC Bank Group Research said in a report that gold's medium-term role as a target for asset diversification remains valid, but its price may be dragged down by a more challenging macroeconomic environment. OCBC analysts said demand for gold may be supported by the official sector, with central banks indicating they intend to increase gold reserves in the next 12 months. However, they added that investors have already priced in expectations for US Fed interest rate hikes, and the short-term macro pressure from rising real yields and a stronger US dollar is unlikely to be fully offset. OCBC expects gold prices to reach $4,360 per ounce by the end of 2026 and $4,680 per ounce by the end of Q2 2027. (Jinshi Data APP)

Furthermore, as of the midday close, the most-traded platinum futures rose 3.81%, and the most-traded palladium futures gained 4.1%.

As of the midday close, the most-traded European container shipping route futures contract rose 3.31% to 2,653 points.

As of 11:46 on July 3, midday quotes for some futures:

Spot and fundamentals

Copper: Today, spot #1 copper cathode in Guangdong against the front-month contract: high-quality copper quoted at 60 yuan/mt, up 10 yuan/mt from the previous trading day; standard-quality copper quoted at 20 yuan/mt, up 20 yuan/mt from the previous trading day; SX-EW copper quoted at a discount of 50 yuan/mt, up 10 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 102,965 yuan/mt, up 625 yuan/mt from the previous trading day, while the average price of SX-EW copper was 102,875 yuan/mt, up 620 yuan/mt from the previous trading day. In the spot market, Guangdong inventories have pulled back for two consecutive days…

Macro Front

On the domestic front:

[This year's 200 billion yuan "program of large-scale equipment upgrades and consumer goods trade-ins" funding for equipment renewal has been fully allocated] The National Development and Reform Commission (NDRC) has noted that this year's 200 billion yuan ultra-long-term special sovereign bond funding to support the "program of large-scale equipment upgrades and consumer goods trade-ins" for equipment renewal has been fully allocated. (CCTV News)

[PBOC's open market operations resulted in a net drain of 168.5 billion yuan on the day, and a net drain of 1,587 billion yuan for the week] The PBOC conducted 63 billion yuan of 7-day reverse repo operations today. With 231.5 billion yuan of 7-day reverse repos maturing today, this resulted in a net drain of 168.5 billion yuan for the day. For the week, the PBOC conducted 678.5 billion yuan of 7-day reverse repos and 900 billion yuan of overnight reverse repos. With 2,265.5 billion yuan of 7-day reverse repos and 900 billion yuan of overnight reverse repos maturing this week, this resulted in an aggregate net drain of 1,587 billion yuan for the week. (Jin10 Data APP)

On the US dollar front:

As of 11:46, the US dollar index fell 0.07% to 100.81. On Friday, the US dollar was on track for its biggest weekly loss in nearly three months, after a weaker-than-expected June payrolls report delayed market expectations for US Fed rate hikes and offered some respite to the ailing yen. A sharp slowdown in US employment growth in June prompted traders to scale back their expectations of near-term rate hikes by the US Fed, with the market now pricing in a 52% chance of a hike at the September meeting, down from 64% the previous trading day. US Treasury yields also pulled back from earlier highs, with the two-year yield snapping a three-day winning streak. OCBC currency strategist Sim Moh Siong said, "At the margin, the data is a bit dovish and helps ease concerns about an overheating labor market and the need for more aggressive policy tightening." However, he added that so long as expectations of Fed tightening remain in place, the overall outlook for the US dollar remains constructive, especially against low-yielding currencies. (Jin10 Data APP)

According to CME "FedWatch": The probability of the US Fed keeping rates unchanged at the July meeting is 82.4%, and the probability of a cumulative 25-basis-point rate hike is 17.6%. For the September meeting, the probability of rates remaining unchanged is 46.8%, while the probability of a cumulative 25-basis-point rate hike is 45.6% and the probability of a cumulative 50-basis-point rate hike is 7.6%. Jin10 Data APP)

CICC research report pointed out that the US added 57,000 nonfarm payrolls in June, below market expectations, indicating a cooling of the acceleration in job growth. After downward revisions to previous months, the average job gains over the past three months still reached 111,000, showing that the labour market is still expanding. Meanwhile, the unemployment rate fell to 4.2%, and the labour force participation rate continued to pull back, reflecting steady labour demand coexisting with a contraction in labour supply, with overall unemployment pressure relatively small. CICC believes that this data gives the US Fed time to wait and watch, thus maintaining the judgement that there will be neither an interest rate increase nor a cut for the rest of the year. In the medium term, the improvement in US employment this year is more attributable to the economic cycle recovery driven by AI investment, rather than short-term factors such as the World Cup. This means that if total economic demand continues to expand boosted by AI, the possibility of the US Fed resuming interest rate hikes next year cannot be ruled out.

Huatai Securities research report stated that the US nonfarm payrolls in June missed expectations, mainly due to a sharp pullback in leisure and hospitality and local government employment, which had been boosted earlier by the early Memorial Day and the World Cup. By sector, both services and government saw a marked slowdown in new nonfarm jobs, while the goods sector saw a small rebound. The June nonfarm report eased market concerns about overheating risks in the US labour market. Leading indicators suggest that employment levels will be around the equilibrium level of 0‒50,000 in the coming months, maintaining the view that the US Fed will keep interest rates unchanged in H2 and may need to raise rates next year.

Data:

Today, France's May industrial production m/m, France's June final services PMI, Germany's June final services PMI, Eurozone June final services PMI, UK June final services PMI, and other data will be released. In addition, China's refined oil products will open a new pricing window. European Central Bank President Lagarde will attend an economic forum, and Bank of England Governor Bailey will deliver a speech on fiscal and monetary policy coordination.

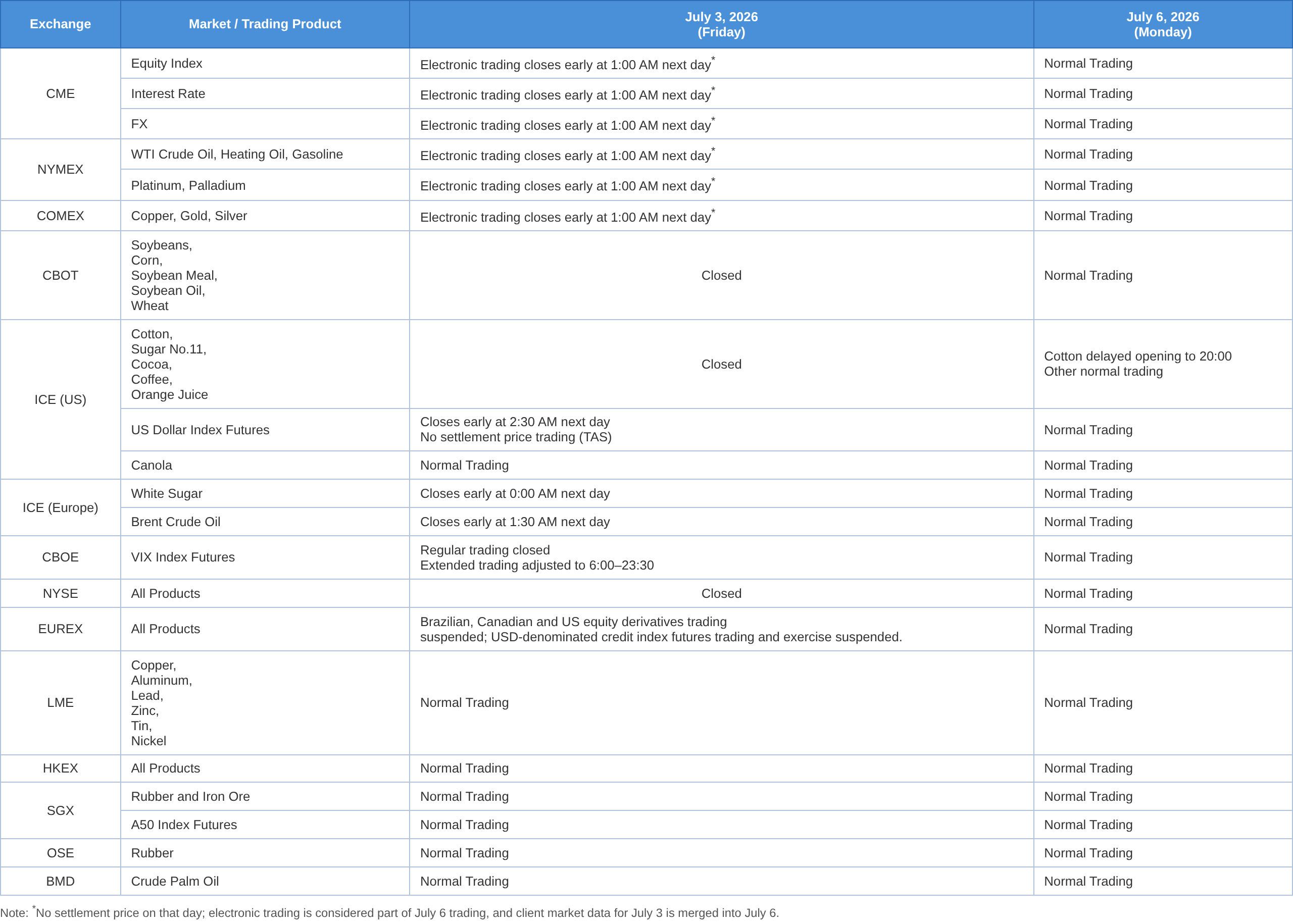

Notably, on July 3, the US – NYSE will be closed for one day due to the US Independence Day holiday. The US – CME, due to the US Independence Day, will have trading in its precious metals, energy, foreign exchange, US Treasury, and equity index futures contracts close early at 01:00 Beijing time on July 4.

July 3 (Friday) coincides with the US Independence Day holiday, and financial market trading hours will be adjusted accordingly. The holiday schedules for overseas exchanges are as follows: (all times are Beijing time)

Crude oil:

As of 11:46, both benchmarks rose, with WTI up 0.52% and Brent up 0.64%.

Saudi Arabia’s crude exports have surged to near pre-war levels since it resumed loading and unloading tankers in the Persian Gulf, providing further evidence that oil supplies from regional producers are recovering following the US-Iran interim peace agreement. In the six days through Wednesday, the world’s largest oil exporter shipped a daily average of 6.3 million barrels of crude, according to tanker-tracking data compiled by Bloomberg. That pace is roughly in line with the average for 2025 and nearly 90% of February’s level, when the kingdom and its Gulf neighbors ramped up supply before the Iran war broke out. (Jin10 Data APP)

Citigroup said the US-Iran memorandum of understanding is expected to remain in force in the coming months and eventually be converted into a formal agreement. The incentives for de-escalating the conflict outweigh the costs of returning to confrontation. The bank reiterated its recommendation to sell into any summer rally and forecast that Brent crude will fall to $60-65 a barrel by year-end.

Additionally, "gasoline prices have been a bit sticky on the way down," US Treasury Secretary Bessent said in a CBS News interview. "We’re trying to put a little pressure on the gasoline retailers. We are telling them we’re watching closely," Bessent said, "We’ve gotten positive responses from some of the big-box retailers on doing something for the consumer." Bessent hopes the average gasoline price will fall to $3 a gallon by Labor Day and said he expects oil and energy prices to continue to pull back. (From Wall Street News APP)

Separately, trading in Intercontinental Exchange (ICE) Brent crude futures contracts will close early at 01:30 Beijing time on July 4 in observance of US Independence Day.

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

►

![Inventory destocking, combined with suppliers holding prices firm, pushed the center of Shanghai spot copper premiums steadily higher [SMM Shanghai spot copper]](https://imgqn.smm.cn/usercenter/arNnt20251217171714.jpeg)

![Guangdong Zinc: End-users Hold Certain Inventory, Making Market Trading Volume Difficult to Increase [SMM Midday Comment]](https://imgqn.smm.cn/usercenter/CGlrd20251217171755.jpg)

![Tight Supply, Suppliers Bullish, Holding Prices Firm; Downstream Wary of High Prices, Trading Sluggish [SMM Yangshan Spot Copper]](https://imgqn.smm.cn/usercenter/qBqQv20251217171708.jpg)