SMM July 3 News:

Metals Market:

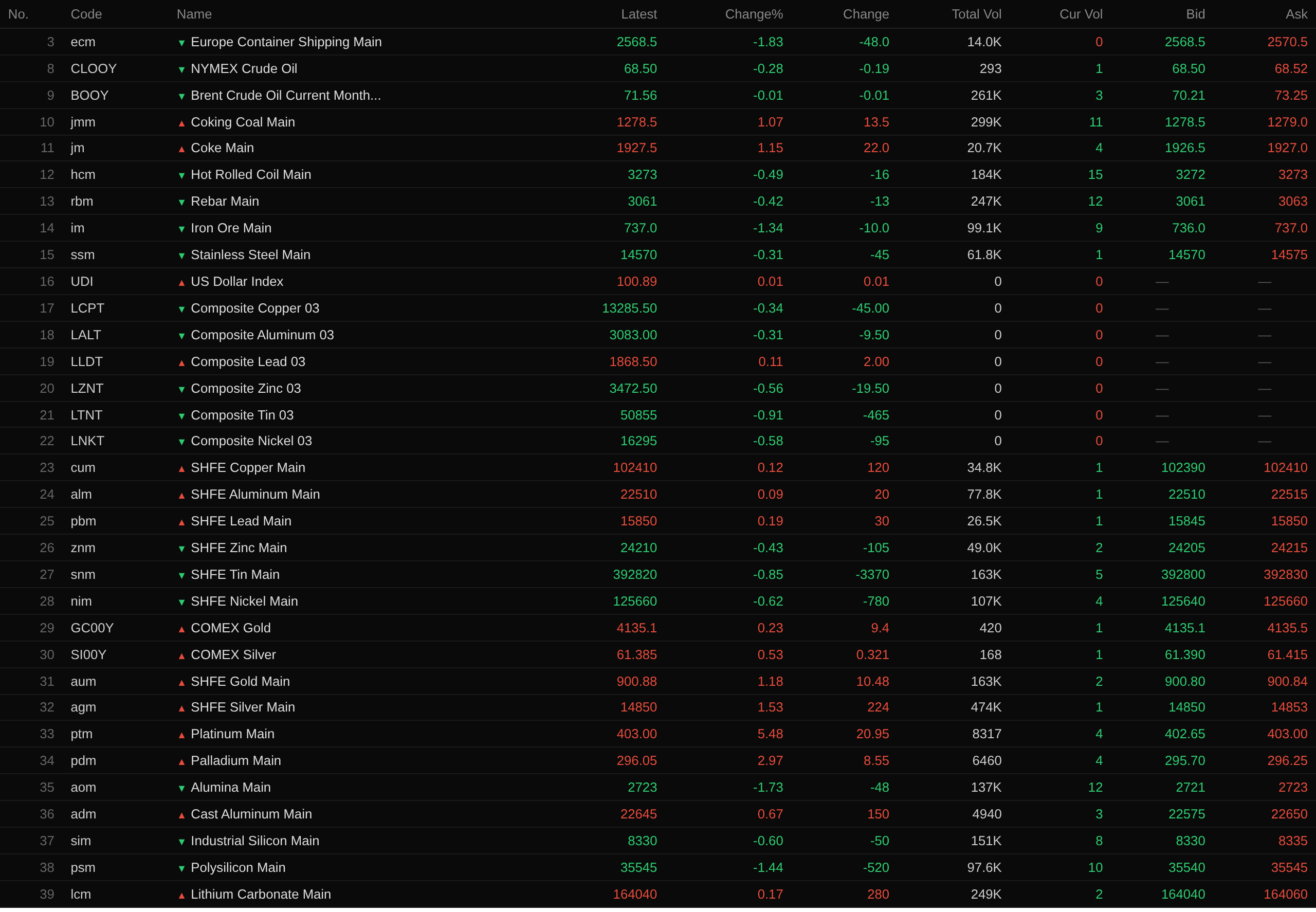

Overnight, base metals on both domestic and overseas markets showed mixed performance. SHFE lead led the gains with a 0.19% increase, SHFE copper rose 0.12%, LME lead rose 0.11%, and SHFE aluminum rose 0.09%. LME tin led the losses with a 0.91% drop, SHFE tin fell 0.85%, and declines in other metals were relatively small. The most-traded alumina contract fell 1.73%, while cast aluminum rose 0.67%.

In the ferrous metals sector overnight, iron ore led the losses with a 1.34% drop, while rebar and HRC fell around 0.4%. As for coking coal and coke, coking coal rose 1.07%, and coke rose 1.15%.

In precious metals overnight, all rose. COMEX gold rose 1.3%, and COMEX silver rose 1.54%. On the domestic market, SHFE gold rose 1.18%, and SHFE silver rose 1.53%.

As of 6:38 am on July 3, overnight closing prices:

Macro Front

China:

[National Energy Administration: Vigorously Promote the Exploration and Development of Deep Coalbed Methane] On July 1, the National Energy Administration held a special meeting on deep coalbed methane exploration and development in Beijing. The meeting pointed out that the core task is to ensure national energy security, vigorously promote the exploration and development of deep coalbed methane, and continuously consolidate the foundation of energy supply. The meeting emphasized the implementation of relevant plans. It called for the issuance and implementation of the "15th Five-Year Plan" for coalbed methane (coal mine gas) development and utilization, as well as action plans for increasing reserves and production in key regions, with tasks detailed to each enterprise and each coalbed methane block, increasing investment in exploration and development, and accelerating the construction of key projects. (National Energy Administration)

[Liu Gang of the NDRC Led a Team to Conduct Work Research at Xiaomi Group] Liu Gang, Deputy Director of the Price Monitoring Center of the National Development and Reform Commission (NDRC), led a team to conduct work research at Xiaomi Group. The research covered the price trends of NEVs and mobile phones, sought to understand the main issues facing the industry, and solicited opinions and suggestions on standardizing the automotive industry’s practices and promoting orderly competition. (NDRC Price Monitoring Center)

US Dollar:

As of the overnight close, the US dollar index fell 0.54% to 100.86. The US economy added 57,000 nonfarm payrolls in June, below Wall Street expectations. After three consecutive months of stronger-than-expected employment growth, the slowdown in June hiring prompted the market to lower expectations for further Fed rate hikes. Data released by the US Bureau of Labor Statistics on Thursday showed that the 129,000 jobs added in June, revised down from May, represented a sharp decline, and was also below the 115,000 forecast by economists surveyed by Bloomberg. The report marked a significant cooling in the labour market following three months of better-than-expected job gains. While job growth decelerated, it remained well above the 2025 target of 10,000 new jobs per month on average. The unemployment rate edged down to 4.2% from 4.3% in May. The US dollar weakened as investors scaled back bets on further Fed rate hikes. Futures traders now expect the Fed to raise rates in December. Previously, the market had anticipated a rate hike in October. (Jin10 Data APP)

A CICC research report stated that the US added 57,000 nonfarm payrolls in June, below market expectations, indicating that the acceleration in job growth has cooled. After downward revisions to previous months, the average job gains over the past three months still reached 111,000, suggesting that the labour market remains expansionary. Meanwhile, the unemployment rate fell to 4.2%, and the labour force participation rate continued to decline, reflecting steady labour demand alongside a shrinking labour supply, with overall unemployment pressure relatively low. We believe this data gives the Fed time to wait and watch, thus we maintain the view that there will be neither a rate hike nor a rate cut this year. In the medium term, the improvement in US employment this year is driven more by AI investment-led economic cycle repair rather than short-term factors like the World Cup. This means that if aggregate demand continues to expand under the boost of AI, the possibility of the Fed resuming rate hikes next year cannot be ruled out. (Jin10 Data APP)

According to the CME FedWatch Tool: The probability that the Fed keeps interest rates unchanged in July is 82.4%, while the probability of a cumulative 25-basis-point rate hike is 17.6%. For the September meeting, the probability of rates staying unchanged is 46.8%, the probability of a cumulative 25-bp hike is 45.6%, and the probability of a cumulative 50-bp hike is 7.6%. (Jin10 Data APP)

On the Macro Front:

Today, data including China's June RatingDog Services PMI, French May industrial production month-on-month, the final June Services PMIs for France, Germany, the Eurozone, and the UK will be released.

In addition, China will open a new round of price adjustment window for domestic refined oil products. ECB President Christine Lagarde will participate in an economic forum, and BOE Governor Andrew Bailey will speak on the coordination of fiscal and monetary policies.

Notably, on July 3, US markets—NYSE will be closed for the US Independence Day holiday. CME will close trading in precious metals, energy, foreign exchange, US Treasury, and stock index futures contracts early at 01:00 Beijing time on July 4 for the Independence Day holiday. ICE will close Brent crude oil futures trading early at 01:30 Beijing time on July 4 for the Independence Day holiday.

Crude Oil:

Overnight, both oil benchmarks fell, with WTI crude down 0.17% and Brent crude down 0.01%, as buyers sought to secure supply ahead of the US Independence Day long weekend. Since Saudi Arabia resumed loading operations in the Persian Gulf, its crude oil exports have surged to roughly pre-war levels. This further indicates that regional producers' supply is recovering following the temporary peace agreement between the US and Iran. Bloomberg-compiled tanker tracking data showed that Saudi Arabia, the world’s largest oil exporter, averaged 6.3 million barrels per day (bpd) of crude exports in the six days through Wednesday. That export level is comparable to the 2025 average and has reached nearly 90% of the pre-war February level, when Saudi and its Gulf neighbours ramped up supply. (from Wallstreetcn APP)

Since Saudi Arabia resumed tanker loading and unloading in the Persian Gulf, its crude oil exports have surged to near pre-war levels, further evidence that regional oil supply is recovering after the US-Iran temporary peace agreement. Bloomberg-compiled tanker tracking data showed that Saudi Arabia, the world's largest oil exporter, shipped an average of 6.3 million barrels per day (bpd) of crude in the six days through Wednesday. That shipping volume is roughly on par with the 2025 average and has reached nearly 90% of the February level. In February, before the Iran war broke out, Saudi Arabia and its Gulf neighbours had significantly increased oil supply. (Jin10 Data APP)

![Inventory continued to decline and suppliers took the opportunity to hold prices firm, but overall trading was moderate [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/TlzAr20251217171709.jpg)

![Overnight LME lead bottomed out and edged up, while SHFE lead retreated after rapid rise but closed higher [SMM Lead Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/TmYox20251217171721.jpeg)

![Non-farm payrolls data fell short of expectations, supporting LME zinc's rebound from lows [SMM Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/eyxqF20251217171756.jpg)