SMM July 2 News: On July 1, GB/T 46992-2025, Technical specification for classification and comprehensive utilization of recyclable rare earth secondary resources, officially came into effect. The standard systematically classifies rare earth secondary resources into nine major categories for the first time and introduces an innovative three-level “SRRE” coding system. It and GB/T 23588-2020, Recyclable materials from NdFeB production and processing, form a complementary pattern—the latter is a detailed technical specification for a single NdFeB category, while the former provides a management framework covering all categories. The concurrent implementation of the two standards marks a new phase of systematic management for rare earth secondary resources.

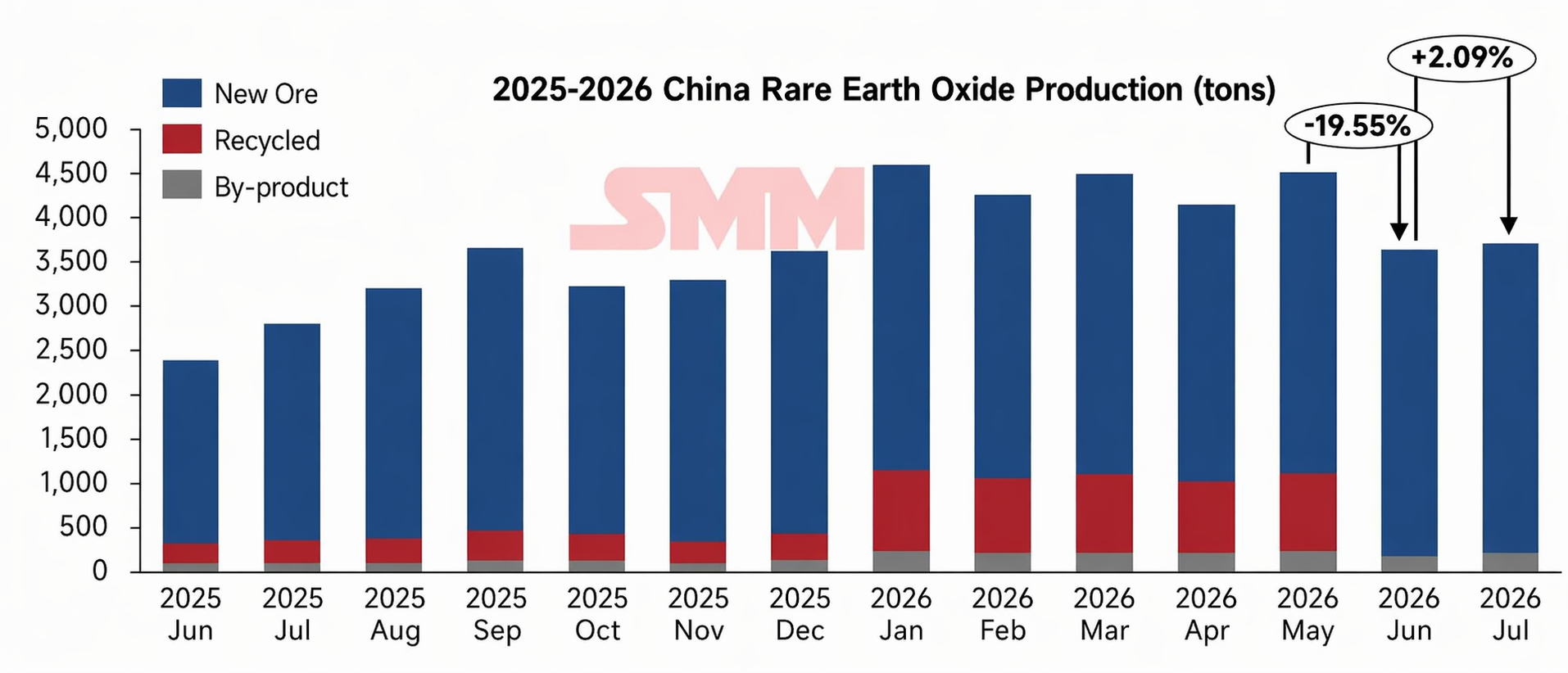

The new national standard arrives amid drastic industry changes. Since H2 2025, local fiscal rebates have been canceled, and the industry tax burden has risen from 9% to 13%; tax compliance audits continued to intensify in 2026. Recycling enterprises have largely suspended purchases of untaxed scrap, which previously accounted for about 50% of the total, including old scrap (20–30%) and scrap from small and medium-sized magnetic material enterprises and traders (30–40%). The industry is generally facing the dilemma of “no invoices to purchase.” The sharp supply contraction quickly fed through to production: in June, secondary oxide production fell 19.5% MoM, and the proportion of Pr-Nd oxide dropped from 42% to 37%.

Against this backdrop, the significance of the new national standard’s implementation becomes particularly pronounced. Previously, rare earth secondary resources long lacked a unified classification and coding system, with scrap from diverse sources and inconsistent naming, creating severe difficulties for compliant transactions and tax administration. The “SRRE” three-level coding system established by the new standard assigns a clear “identity” to each type of secondary resource. This is not only an upgrade of technical specifications but also an infrastructure for industry governance—when every batch of scrap can be accurately classified, coded, and traced, the compliance cost for taxed transactions will drop significantly, and tax audits will have a clear basis.

Looking ahead, the recovery of secondary supply will not happen overnight. The recycling market is undergoing rectification of scrap invoicing and tax compliance, and overall operating rates will remain low in the near term. Although the subsequent peak demand season may raise operating rates at magnetic material enterprises and thereby increase taxed scrap supply, it will be difficult to fully offset the production cut gap. H2 production of secondary Pr-Nd oxide is expected to fall short of H1 levels. Against the backdrop of steadily advancing raw ore capacity, the proportion of secondary Pr-Nd oxide will continue to decline, with the full-year proportion estimated at around 40%. Over a longer horizon, as the new national standard promotes standardized and tax-compliant scrap trading, and capacity concentration at major magnetic material plants gradually increases, the rare earth scrap recycling industry is expected to move from “chaos” to “order” after short-term pain.

![Pr-Nd prices surge, while medium-heavy rare earth market prices remain relatively stable [SMM Rare Earth Weekly Review]](https://imgqn.smm.cn/usercenter/OJvHl20251217171744.jpeg)