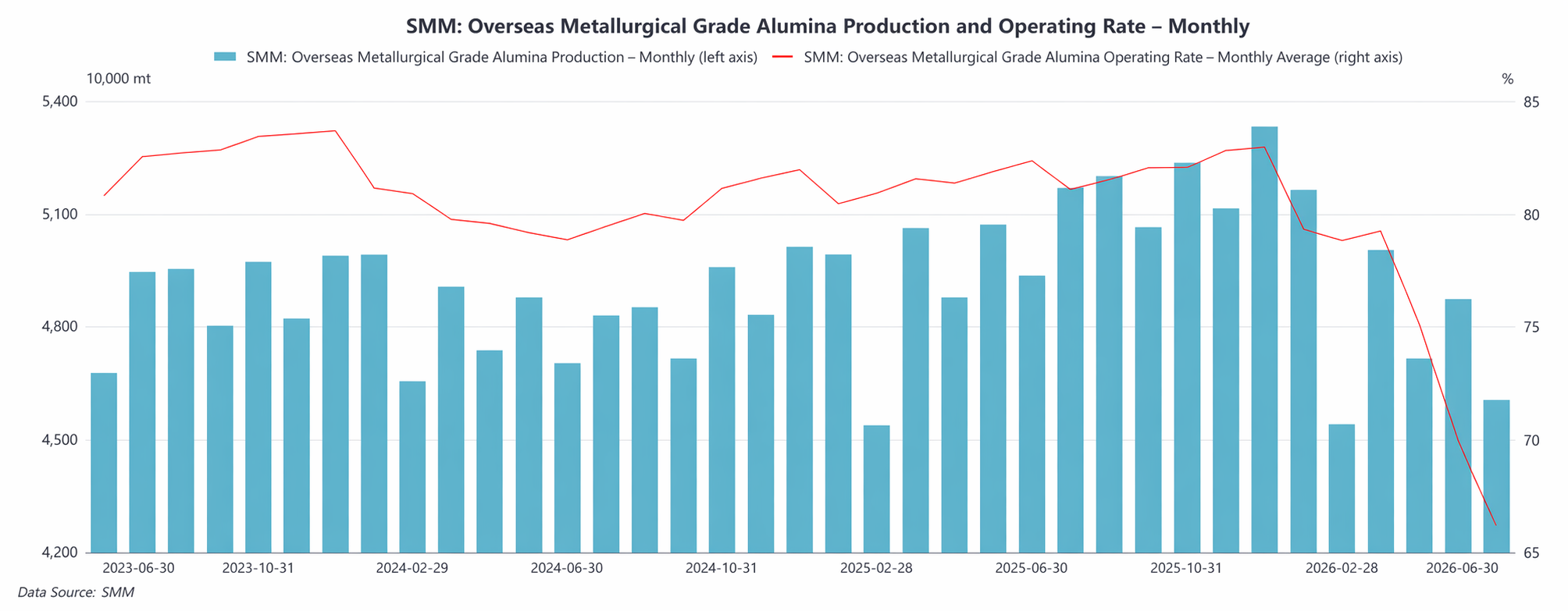

SMM, ngày 30 tháng 6:

Theo thống kê của SMM, tổng sản lượng alumin cấp luyện kim bên ngoài Trung Quốc trong tháng 6 năm 2026 giảm khoảng 6,0% so với cùng kỳ năm ngoái và khoảng 5,5% so với tháng trước. Trong tháng 6, gián đoạn nguồn cung trên thị trường alumin ngoài Trung Quốc trở nên rõ rệt hơn so với tháng 5. Một mặt, do tình hình Trung Đông, tiến độ sản xuất và vận chuyển tại một số doanh nghiệp vẫn chưa hồi phục hoàn toàn; mặt khác, thời tiết và gián đoạn cung cấp khí tự nhiên tại Úc vẫn tiếp diễn, gây áp lực lên sản xuất và vận chuyển alumin tại địa phương.

Xét theo doanh nghiệp và khu vực, Alcoa cho biết, do ảnh hưởng của cơn bão Narelle trước đó tại Úc, nguồn cung LNG cho nhà máy lọc alumin Pinjarra của họ ở Tây Úc tạm thời bị gián đoạn. Công ty dự kiến lượng alumin xuất xưởng quý 2 sẽ thấp hơn quý 1 khoảng 120.000 tấn, và sự gián đoạn này dự kiến sẽ đẩy chi phí sản xuất quý 2 tăng khoảng 30 triệu đô la Mỹ. Ngoài ra, do tình hình Trung Đông, chi phí nhiên liệu tại nhà máy lọc alumin São Luís của công ty ở Brazil cũng tăng. Hiện nay, hoạt động alumin tại Tây Úc của Alcoa vẫn đang chịu nhiều áp lực, bao gồm giá alumin yếu, chất lượng bauxite giảm sút và chi phí năng lượng tăng cao, khiến hoạt động tổng thể của công ty rõ ràng bị ảnh hưởng.

Tại châu Âu, rủi ro địa chính trị tiếp tục leo thang. Trong tháng 6, khi thảo luận về vòng trừng phạt mới của EU đối với Nga, vấn đề xuất khẩu alumin từ nhà máy Aughinish Alumina ở Ireland sang Nga tiếp tục thu hút sự chú ý. Các báo cáo công khai cho thấy gói trừng phạt mới nhất của EU chưa đưa xuất khẩu alumin vào danh sách hạn chế, nhưng nếu sau này các biện pháp trừng phạt được thắt chặt hơn, điều này có thể ảnh hưởng đến dòng chảy thương mại alumin và cục diện cung ứng trong khu vực châu Âu.

Kể từ tháng 6, với sự xuất hiện của một số lượng bauxite từ Malaysia, nguồn cung nguyên liệu tại một số nhà máy lọc alumin địa phương đã được cải thiện, tạo ra một số dư địa cho phục hồi sản xuất, nhưng các vấn đề liên quan đến hạn ngạch xuất khẩu bauxite của Indonesia và sự ổn định hậu cần vẫn cần được theo dõi sát sao.

Ngoài ra, trong tháng 6, Tajikistan và Azerbaijan đã tìm hiểu hợp tác về cung ứng alumin và thương mại sản phẩm nhôm, theo đó Azerbaijan có kế hoạch cung cấp alumin cho Tajikistan và Tajikistan sẽ xuất khẩu sản phẩm nhôm sang Azerbaijan. Hợp tác này sẽ có tác động hạn chế đối với sản lượng alumin bên ngoài Trung Quốc trong ngắn hạn, nhưng nó phản ánh rằng sự điều phối chuỗi ngành nhôm khu vực và các điều chỉnh dòng chảy thương mại vẫn đang được thúc đẩy.

Nhìn sang tháng 7, nguồn cung alumin cấp luyện kim bên ngoài Trung Quốc được kỳ vọng sẽ tăng nhờ phục hồi, với sản lượng phục hồi khoảng 4,5% so với tháng trước. Một mặt, với việc quặng bô-xít cập cảng, các hạn chế nguyên liệu thô tại một số nhà máy tinh luyện alumin ở Indonesia đã được nới lỏng, và sản lượng dự kiến sẽ dần phục hồi; mặt khác, thời tiết và gián đoạn nguồn cung khí đốt tự nhiên tại Úc đang giảm nhẹ, và tốc độ sản xuất và vận chuyển bị ảnh hưởng trước đó có thể hồi phục. Tuy nhiên, rủi ro địa chính trị ở Trung Đông, sự bất ổn về lệnh trừng phạt của EU đối với Nga, áp lực chi phí từ năng lượng ở Úc, và vấn đề hạn ngạch bô-xít của Indonesia vẫn có thể làm gián đoạn sự phục hồi nguồn cung bên ngoài Trung Quốc. Nhìn chung, sản lượng alumin bên ngoài Trung Quốc dự kiến sẽ phục hồi nhẹ vào tháng 7, nhưng sự bất ổn về phía cung vẫn ở mức cao.

(Thông tin trên được thu thập từ dữ liệu thị trường và đánh giá tổng hợp của nhóm nghiên cứu SMM. Thông tin trong bài viết này chỉ mang tính tham khảo. Bài viết không đưa ra lời khuyên trực tiếp cho các quyết định nghiên cứu đầu tư. Khách hàng nên thận trọng khi đưa ra quyết định và không nên sử dụng thông tin này để thay thế cho phán đoán độc lập của mình. Mọi quyết định của khách hàng đều không liên quan đến SMM.)

Nguồn dữ liệu: SMM

![Kỳ vọng nhu cầu robot hình người và động cơ hiệu suất cao thúc đẩy, ngành động cơ tăng mạnh, Jiangxi Special Electric Motor tăng trần [SMM Quick News]](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)