Anti-dumping Investigation Details

On June 22, 2026, India’s Ministry of Commerce and Industry issued a notice announcing the initiation of an anti-dumping investigation concerning imports of Cold Rolled Grain Oriented Electrical Steel (CRGO) and Amorphous Metal (AM) originating in or imported from China, Japan, South Korea, and Russia, in response to an application filed by domestic producer JSW JFE Electrical Steel Nashik Private Limited.

This case primarily covers products under HS codes 72251100, 72261100, and 72269930, as well as certain products under HS codes 72251920, 72251990, 72261920, 72269910, 72261990, 72269910, 72269920, and 72269990.

The dumping investigation period runs from April 1, 2025 to March 31, 2026 (12 months), and the injury investigation period covers April 1, 2022 to March 31, 2023, April 1, 2023 to March 31, 2024, April 1, 2024 to March 31, 2025, and April 1, 2025 to March 31, 2026.

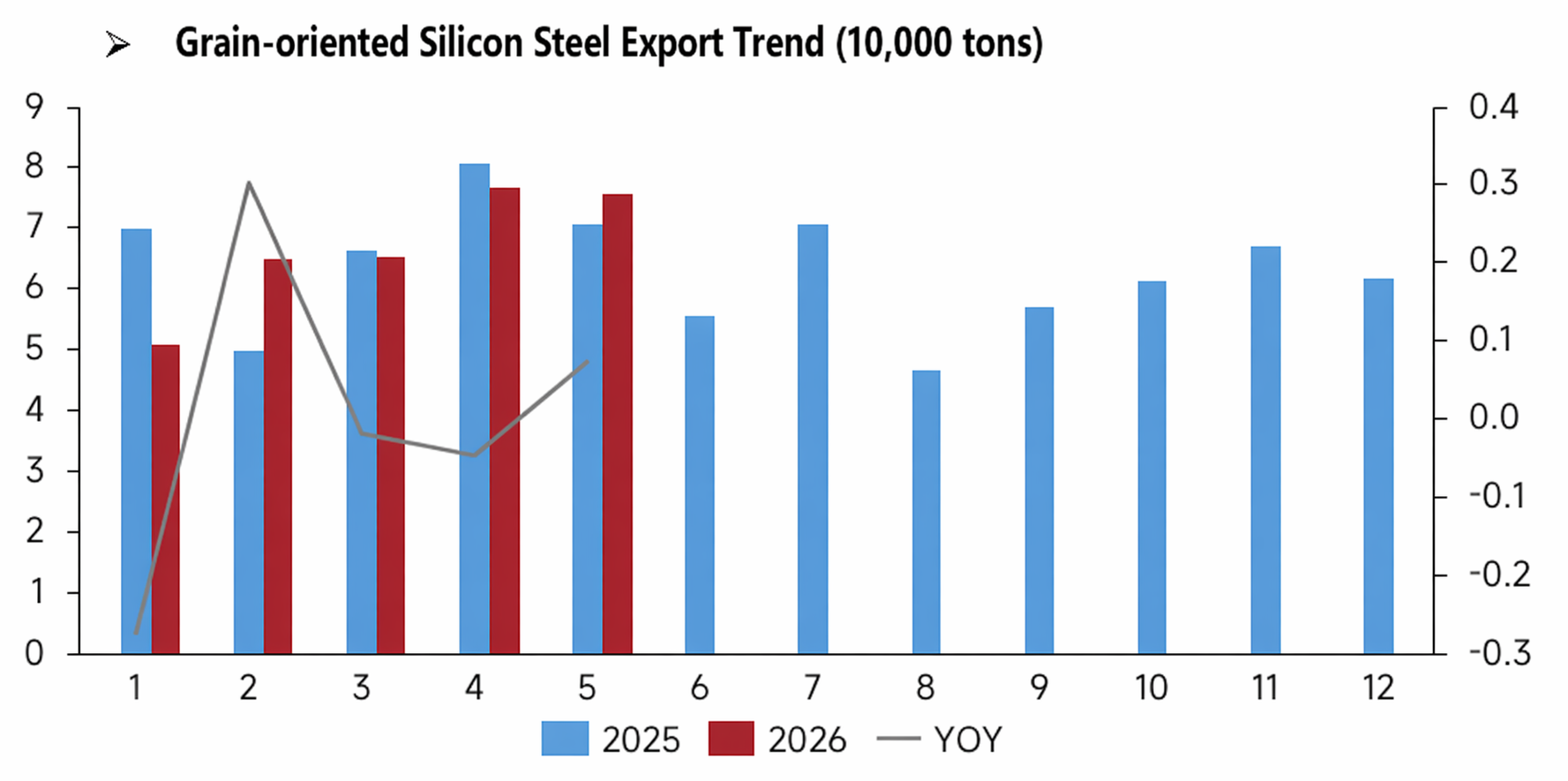

China’s Grain-Oriented Silicon Steel Exports

Source: General Administration of Customs

Comparing January-May exports of grain-oriented silicon steel, monthly exports in the first five months of 2025 fluctuated more sharply, with a notable pullback in February and a peak for the period in April. In the first five months of 2026, monthly exports rose steadily month by month, showing a smoother trend; overall exports for January-May 2026 were similar to those of January-May 2025, and demand outside China remained relatively stable.

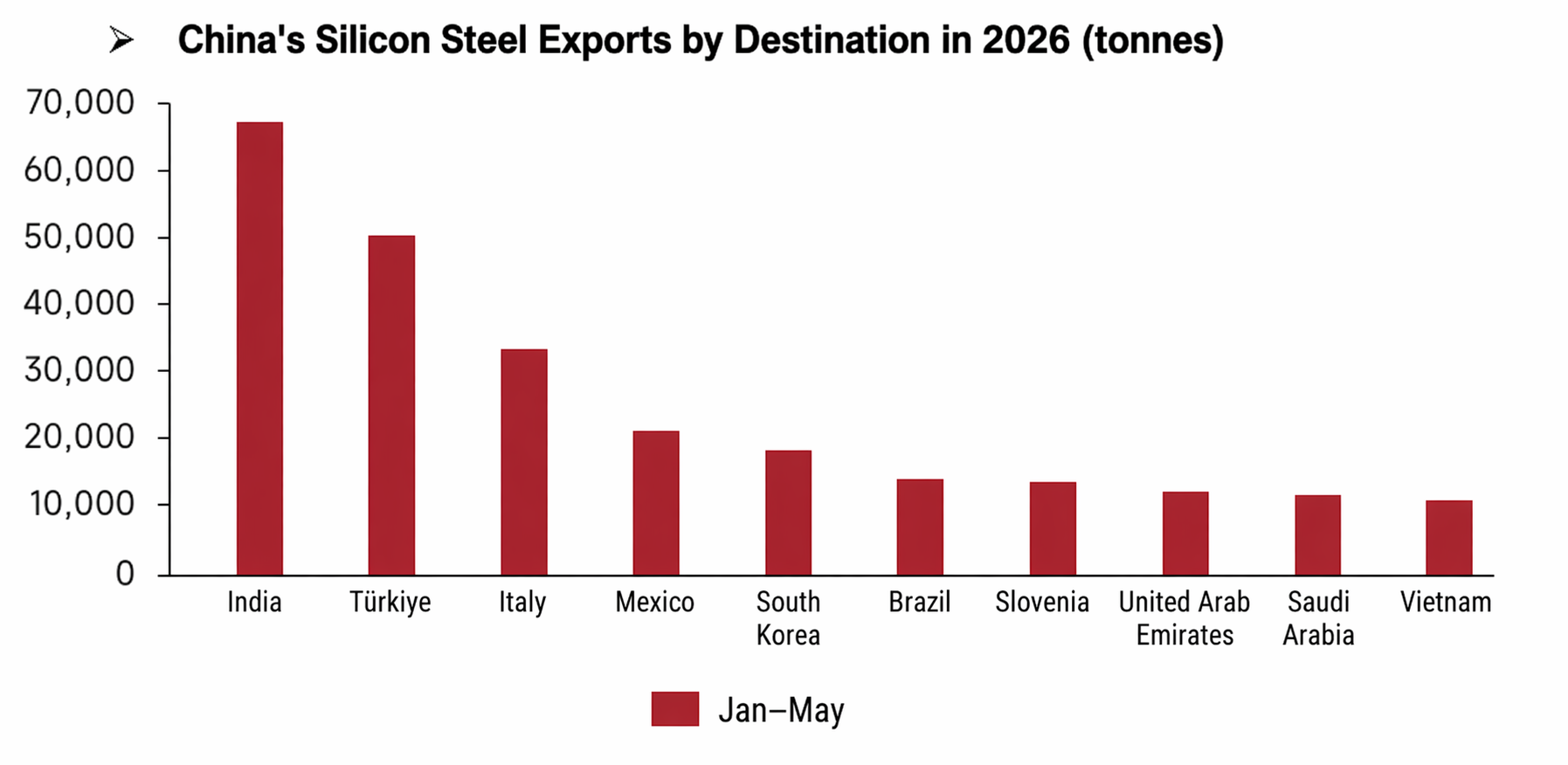

Source: General Administration of Customs

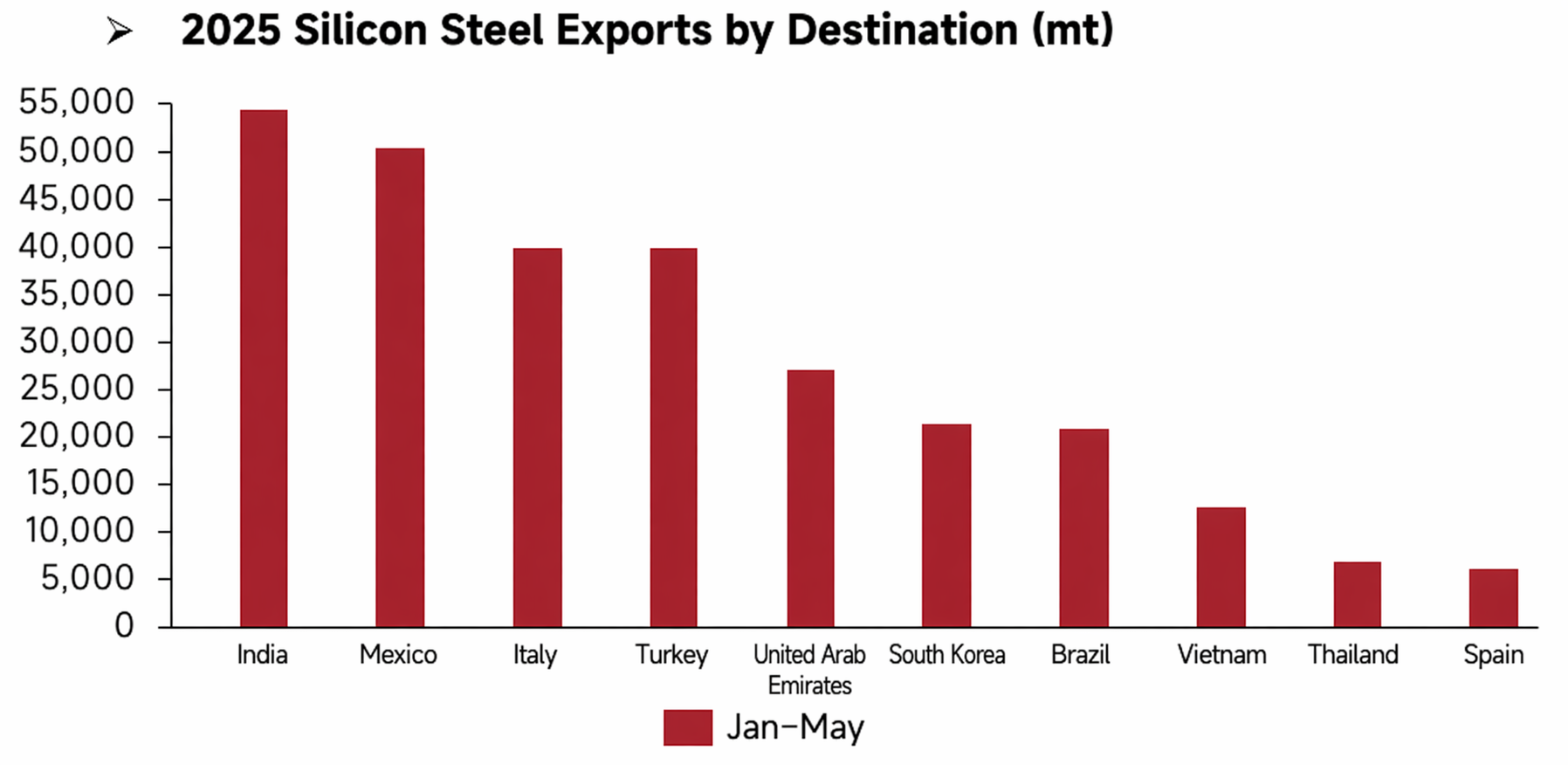

Among the top 10 destinations for grain-oriented silicon steel exports in the first five months of 2025 and 2026, India ranked as the largest market for the second consecutive year, with outstanding growth—exports to India were about 54,400 mt in the first five months of 2025, rising to 67,600 mt in the same period of 2026, a notable increase. Turkey moved significantly up the ranking, and Mexico dropped; Slovenia and Saudi Arabia entered the top 10, while Thailand and Spain fell out of the list. Exports to traditional markets—Italy, Mexico, South Korea, Brazil, the UAE, and Vietnam—generally pulled back YoY, with only India and Turkey recording a YoY increase; India became the sole core overseas demand driver experiencing substantial volume expansion.

China’s large-scale exports of grain-oriented silicon steel to India, combined with the inability of local Indian producers to compete effectively, prompted India to initiate the anti-dumping case.

Estimated Timeline for Implementation of India’s Anti-Dumping Duties

India’s anti-dumping investigation follows a defined timetable: a preliminary determination and provisional duties are expected within 5 to 6 months of initiation; for complex cases involving multiple countries, such as this one on grain-oriented silicon steel, the final determination can take up to 18 months. After the final recommendation is submitted to the Ministry of Finance, a further 3-month review is required, so the entire process leading to the formal imposition of duties is expected to take approximately one and a half to two years. The fixed tariffs determined by the final ruling are valid for 5 years. Before expiry, local enterprises may initiate a sunset review, with the review period also lasting 12-18 months, during which the original tariffs remain in effect.

Relevant grain-oriented silicon steel export enterprises may negotiate price undertakings within a 3- to 8-month window after case initiation to avoid provisional and definitive duties.

Possible impact of India's anti-dumping on China

From case initiation to preliminary determination:

Once the case is filed, Indian importers will proactively adopt a wait-and-see approach, suspend new long-term contracts, and turn to supply sources from Japan and South Korea, leading to a contraction in orders from China to India. In addition, relevant Chinese enterprises will incur high litigation costs and increase various document compliance expenditures; small and medium-sized mills without the capability to respond to lawsuits will directly exit the Indian market, while top-tier players will bear substantial additional costs in defending the case.

When the preliminary ruling is announced after 5-6 months, a provisional anti-dumping duty (for up to 6 months) will be directly imposed, significantly raising export costs, reducing shipments to India, and causing diverted goods to flow back and impact spot prices of grain-oriented silicon steel in China, hurting steel producers' profits. This will increase the willingness to conduct maintenance and control production, put sector sentiment under pressure, and weaken the valuations of listed grain-oriented silicon steel enterprises.

Downstream power equipment, such as domestic transformers and reactors exported to India, will also face obstacles. Bidding costs for complete equipment will rise, and orders from India for power grids, PV inverters, etc., will be lost. Involution in the domestic market will intensify, as low-end transformer manufacturers cut prices to compete for orders, and profits will contract concurrently.

1-2 year long-term cycle:

After the 18-month final determination and Ministry of Finance approval, a high fixed tariff for 5 years will be imposed, constituting a medium- and long-term structural shock. China will be forced to adjust its grain-oriented capacity structure, explore alternative overseas markets, promote building factories abroad, comprehensively reduce its dependence on the single Indian market, focus on developing incremental grid markets in the Middle East, Southeast Asia, and Latin America, and diversify its export structure. Top-tier steel producers will go global, setting up silicon steel slitting bases and joint-venture steel mills in Southeast Asia, while transformer enterprises will simultaneously build factories overseas to circumvent finished-product tariff barriers.

Overseas aspects:

Indian market

In the short term, Indian importers will shift to supply sources from Japan, South Korea, and Russia, leading to higher procurement costs. With insufficient domestic capacity for low-grade silicon steel, transformer manufacturers will face raw material shortages. Downstream power manufacturing associations will protest against rising costs, infrastructure project bids will rise, and the pace of grid expansion will slow down. High tariffs will raise costs across India's entire industry chain, undermining the competitiveness of its new energy and grid infrastructure compared with Southeast Asia. In the long term, policies will continue to support domestic grain-oriented silicon steel projects such as JSW-JFE. Within 5 years, domestic capacity will expand significantly, and low-end silicon steel will achieve self-sufficiency.

Global Trade Market

Enterprises from Japan and South Korea and Russia are seizing China’s original share in India, creating a supply substitution, while China shifts to the Middle East, Southeast Asia, and Latin America to form differentiated competition tracks. The processing of transformers and silicon steel is relocating to Vietnam, Indonesia, and Malaysia, forming a Southeast Asian power equipment manufacturing cluster. Third-country deep processing and origin-based tariff circumvention will become a long-term conventional trade model.

Data Source Statement:

The other data in this report, beyond publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, NBS data, customs import and export data, and various data published by major associations and institutions), market communication, and reliance on SMM’s internal database models, have been comprehensively analyzed and reasonably inferred by the research team. They are for reference only and do not constitute decision-making advice.

Shanghai Metals Market reserves the final right to interpret the terms of this statement and the right to adjust and modify its content based on actual circumstances.

![[ArcelorMittal Urges EU to Extend CBAM and TRQs to Downstream Steel]](https://imgqn.smm.cn/usercenter/GfiYT20251217171720.jpg)