SMM News on July 1:

Metals market:

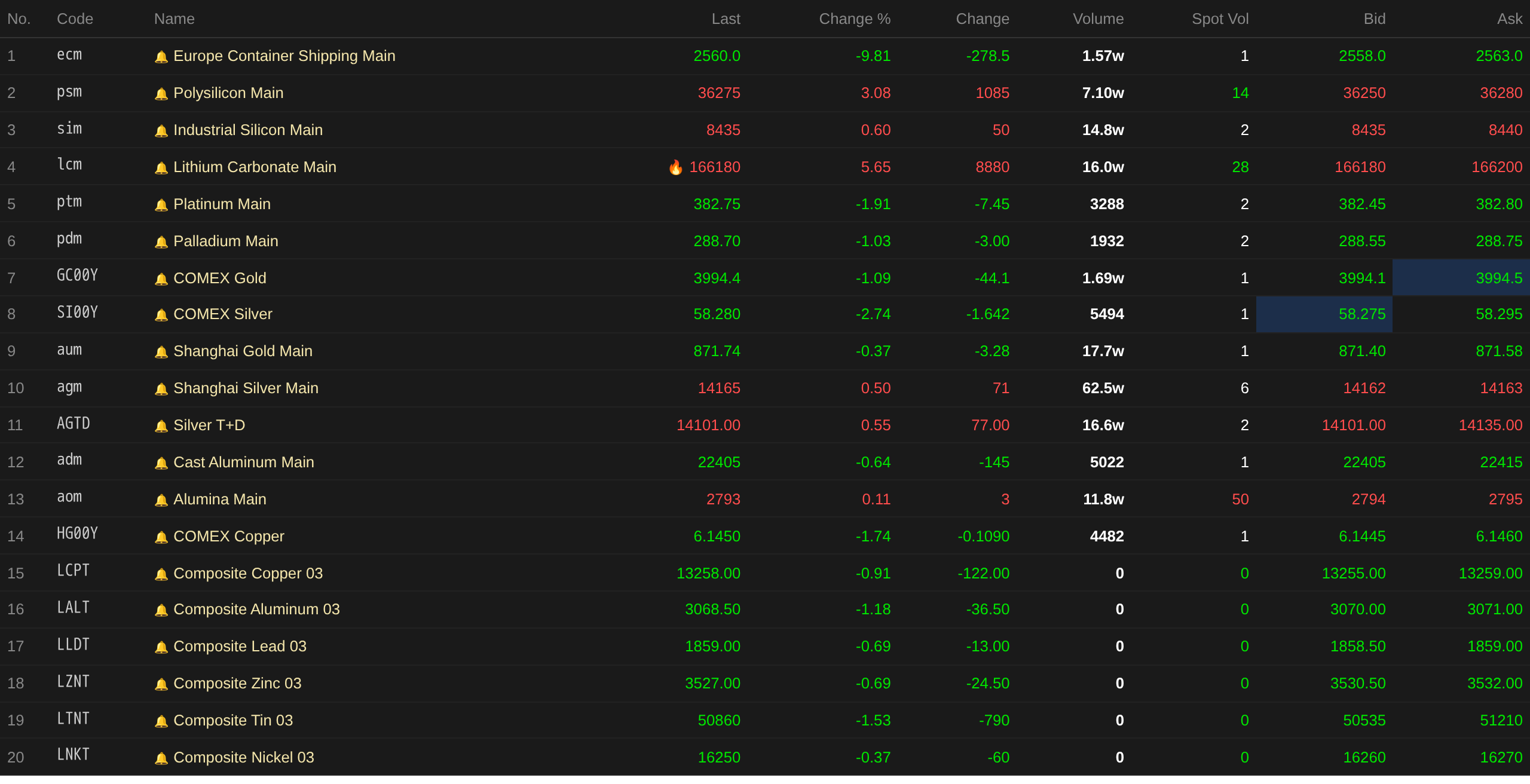

As of midday close, domestic base metals mostly fell. SHFE copper fell 0.44%, SHFE aluminum fell 0.86%. SHFE lead fell 1.46%. SHFE zinc rose 1.01%. SHFE tin rose 0.93%. SHFE nickel fell 0.61%.

Additionally, the most-traded casting aluminum futures fell 0.64%, the most-traded alumina futures rose 0.11%. The most-traded lithium carbonate futures rose 5.65%. The most-traded silicon metal futures rose 0.6%. The most-traded polysilicon futures rose 3.08%.

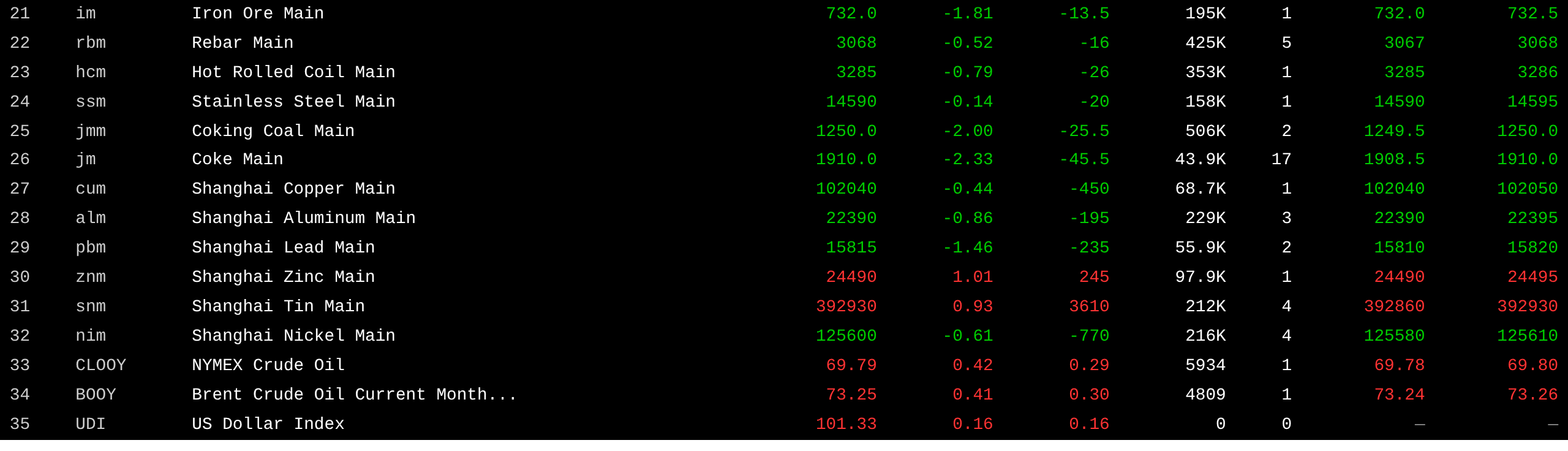

Ferrous metals all fell. Iron ore fell 1.81%, HRC fell 0.52%. Rebar fell 0.79%, stainless steel fell 0.14%. Coking coal and coke: the most-traded coking coal contract fell 2%, the most-traded coke contract fell 2.33%.

Overseas base metals market, as of 11:36, LME metals all fell. LME copper fell 0.91%, LME aluminum fell 1.18%, LME lead fell 0.69%. LME zinc fell 0.69%, LME tin fell 1.53%. LME nickel fell 0.37%.

Precious metals, as of 11:36, COMEX gold fell 1.09%, COMEX silver fell 2.74%. Domestic precious metals: SHFE gold fell 0.37%; the most-traded SHFE silver futures rose 0.5%.

Additionally, as of midday close, the most-traded platinum futures fell 1.91%, and the most-traded palladium futures fell 1.03%.

As of midday close, the most-traded European container shipping futures fell 9.81% to 2,560 points.

As of 11:36 on July 1, midday futures quotes for some contracts:

Spot and fundamentals

Copper: Today, Guangdong #1 copper cathode spot against the front-month contract: high-quality copper reported at a premium of 50 yuan/mt, up 50 yuan/mt from the previous trading day; standard-quality copper reported at parity, up 90 yuan/mt from the previous trading day; SX-EW copper reported at a discount of 60 yuan/mt, up 90 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 102,220 yuan/mt, up 140 yuan/mt from the previous trading day, and the average price of SX-EW copper was 102,135 yuan/mt, up 160 yuan/mt...

Macro front

China:

[The PBOC net withdrew 1,162.5 billion yuan from the open market today.] The PBOC conducted 100 billion yuan in 7-day reverse repo operations today at an unchanged interest rate of 1.4%. Today, 662.5 billion yuan in 7-day and 600 billion yuan in overnight reverse repos matured.

[Shenzhen's June housing transactions hit a near 6-year high.] According to data released by Shenzhen Centaline Research Center today, Shenzhen's new and secondhand home transactions totaled 8,878 units in June, down 11.9% MoM but up 14.2% YoY. The combined new and secondhand home transaction volume hit a new high for the same period since 2021. Among them, first-hand residential (presale + existing) online signings totaled 3,785 units, down 16.7% MoM but up 15.6% YoY; second-hand residential transfers reached 5,093 units, down 8% MoM but up 13.1% YoY. (Jin10 Data APP)

US dollar aspect:

As of 11:36, the US dollar index rose 0.16% to 101.33. Fed’s Hammack said: The labour market is near full employment, with good growth prospects. Inflation remains too high, and the Fed may need to consider rate hikes. Jason Pride, Chief of Investment Strategy at private wealth management and investment firm Glenmede, and Michael Reynolds, Vice President of Investment Strategy, said investors should expect the US June unemployment rate to remain unchanged at 4.3%, with non-farm payrolls increasing by about 87,000. While this represents a pullback from May’s 172,000, in the current labour market environment of “low hiring, low layoffs,” it still counts as a solid outcome. Although employment fundamentals remain largely intact, the Fed’s focus has shifted to inflation, meaning that the timing of any future easing measures will depend more on inflation pressures than on job growth itself. According to CME’s “FedWatch”: The probability of the Fed keeping rates unchanged in July is 66.3%, and the chance of a cumulative 25bp rate hike is 33.7%. For September, the probability of the Fed keeping rates unchanged is 33.1%, the chance of a cumulative 25bp hike is 50.0%, and the chance of a cumulative 50bp hike is 16.9%. (Jin10 Data APP)

Data highlights:

Today will see the release of US June Challenger Job Cuts, US June ADP Employment Change, US June S&P Global Manufacturing PMI (final), US June ISM Manufacturing PMI, US May Construction Spending MoM, UK June Nationwide House Price Index MoM, UK June Manufacturing PMI (final), Switzerland May Real Retail Sales YoY, France June Manufacturing PMI (final), Germany June Manufacturing PMI (final), Eurozone June Manufacturing PMI (final), Eurozone June CPI YoY (preliminary), and Eurozone June CPI MoM (preliminary), among others.

In addition, Fed Chairman Warsh, ECB President Lagarde, Bank of England Governor Bailey, and Bank of Canada Governor Macklem spoke at the “Policy Panel” session of the ECB’s Global Central Bank Forum. The Davos Technology Summit is held from July 1 to 4, with the theme “Physical AI and Robotics.”

It is worth noting that on July 1, the Hong Kong Stock Exchange (China) was closed for the Hong Kong Special Administrative Region Establishment Day, with both northbound and southbound trading suspended. The Toronto Stock Exchange in Canada was closed on July 1 for Canada Day.

Crude Oil:

As of 11:36, both benchmarks edged up, with WTI rising 0.42% and Brent 0.41%.

Preliminary vessel-tracking data from Kpler and Vortexa showed that, shortly after exiting OPEC, the UAE lifted its exports of crude and condensate to a record high in June. Kpler senior oil analyst Rauball said that the UAE’s crude and condensate exports averaged around 3.7 million b/d this month, setting an all-time high and well above the 3.1 million to 3.3 million b/d level before the Middle East conflict erupted. The UAE’s previous export peak was in April 2020, at 3.44 million b/d, when Saudi Arabia and Russia triggered a brief oil price war. Vortexa senior oil analyst Emma Li said that Abu Dhabi’s crude loadings averaged 4 million b/d over the June 1-29 period, exceeding the pre-war level of 3.4 million b/d. Exports also climbed to a record high of 3.7 million b/d, compared with 3.3 million b/d in the first two months of this year. (Jin10 Data APP)

Spot Market at a Glance:

►

►

►

►

►

►

►

►

►

![Restocking Demand Released at the Beginning of the Month, Shanghai Spot Copper Discounts Narrow [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/CJXfS20251217171710.jpg)

![Spot copper supply in the market is limited, and suppliers are holding offers firm [SMM Yangshan spot copper]](https://imgqn.smm.cn/usercenter/ZCsFN20251217171710.jpg)

![The Most-Traded SHFE Tin Contract Pulled Back After Probing Highs, Consolidating Around 390,000 This Morning [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)