SMM July 1st Report:

According to SMM data, China's refined zinc production in June 2026 fell MoM by around 18,000 mt, or over 3.2%, and was down 3.8% YoY. Smelters' cumulative production from January to June rose over 4% YoY, below expectations. In June, domestic smelters saw a production decline; apart from routine maintenance in places like Hunan, Gansu, Henan, Guangxi, and Liaoning, unexpected and early maintenance in Hunan, Henan, Shaanxi, Yunnan, and Inner Mongolia, etc., contributed to the decrease. The increases were mainly from production resumptions after maintenance in Shaanxi, Anhui, Inner Mongolia, Yunnan, Gansu, Hubei, and Xinjiang, as well as production ramp-ups at the end of H1, while some smelters partially limited production release due to equipment issues and raw material supply. SMM expects domestic refined zinc production in July 2026 to fall MoM by around 13,000 mt, or over 2.3%, and down about 8.8% YoY. Cumulative production from January to July is up 2% YoY. In July, smelter production will decline, with maintenance resumptions in Hunan, Henan, Sichuan, Yunnan, Guangxi, and Xinjiang contributing to increases, while output declines are mainly from Liaoning, Henan, Inner Mongolia, Gansu, Sichuan, Hunan, and Guangxi.

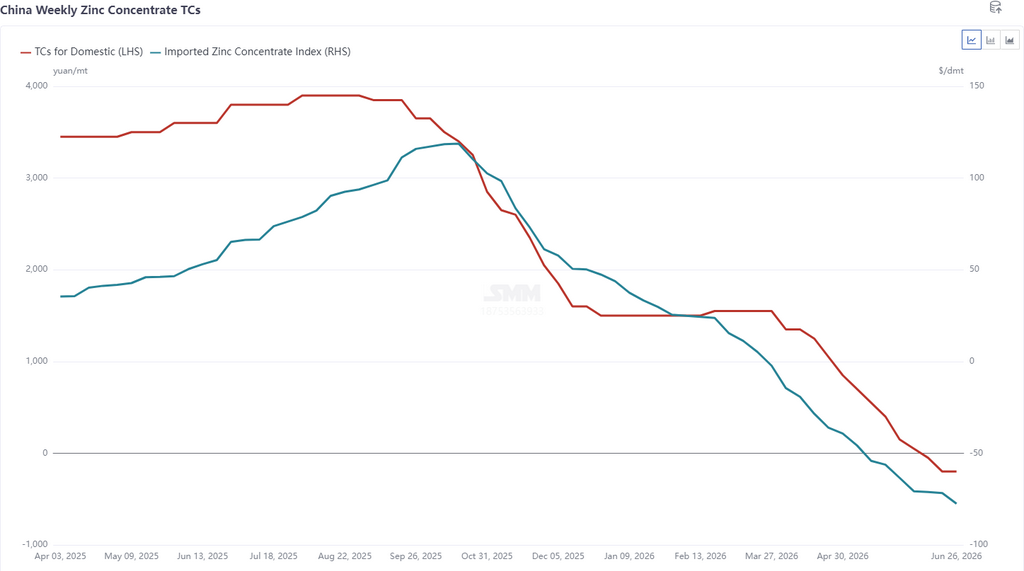

Production side, overall smelter output was below expectations, mainly because capacity releases at some smelters fell short due to equipment issues and temporary early maintenance. In July, planned maintenance at some large smelters is expected to drive further downward revisions to total production. Meanwhile, as TCs continued to fall, China’s July TCs dropped to -500 yuan/mt in metal content and weekly import TCs fell to -$77.5/dmt. Smelter margins were significantly squeezed, with profits mainly supported by sulphuric acid and minor metal earnings. However, silver prices also plunged recently. According to SMM calculations, as of June 30, 2026, domestic refined zinc smelters (using domestic ore) on average incurred a theoretical loss of around 320 yuan/mt including sulphuric acid and minor metal credits, while those using 40% imported ore posted a theoretical loss of over 1,000 yuan/mt. If comprehensive recovery is well managed, earnings hover near the break-even line. If zinc prices and TCs decline further, smelters will face greater earnings pressure. On the raw material side, SMM data show that domestic smelters’ ore inventories fell to 18.16 days in June, the lowest in nearly two years. Against the backdrop of overseas mine production cuts, smelters are also facing increasing raw material pressure.

Going forward, with days of raw material inventories at low levels, if zinc prices and zinc concentrate TCs continue to decline, smelter losses increase, and there is a possibility of further production cuts. Meanwhile, Q3 falls within the traditional maintenance period for smelters, and overall production is expected to remain low, but attention needs to be paid to the release of new capacity from some large smelters.

Data Source Statement: Data other than public information are processed by SMM based on public information, market communication, and SMM's internal database models, for reference only and do not constitute decision-making advice.

![[SMM Flash] Qatar July Sulfur Official Contract Price at $890/mt](https://imgqn.smm.cn/usercenter/HeIuV20251217171708.jpg)

![Supply Side Supports SHFE Zinc Rise, Overnight Price Center Edges Up [SMM Zinc Morning Comment]](https://imgqn.smm.cn/usercenter/eyxqF20251217171756.jpg)