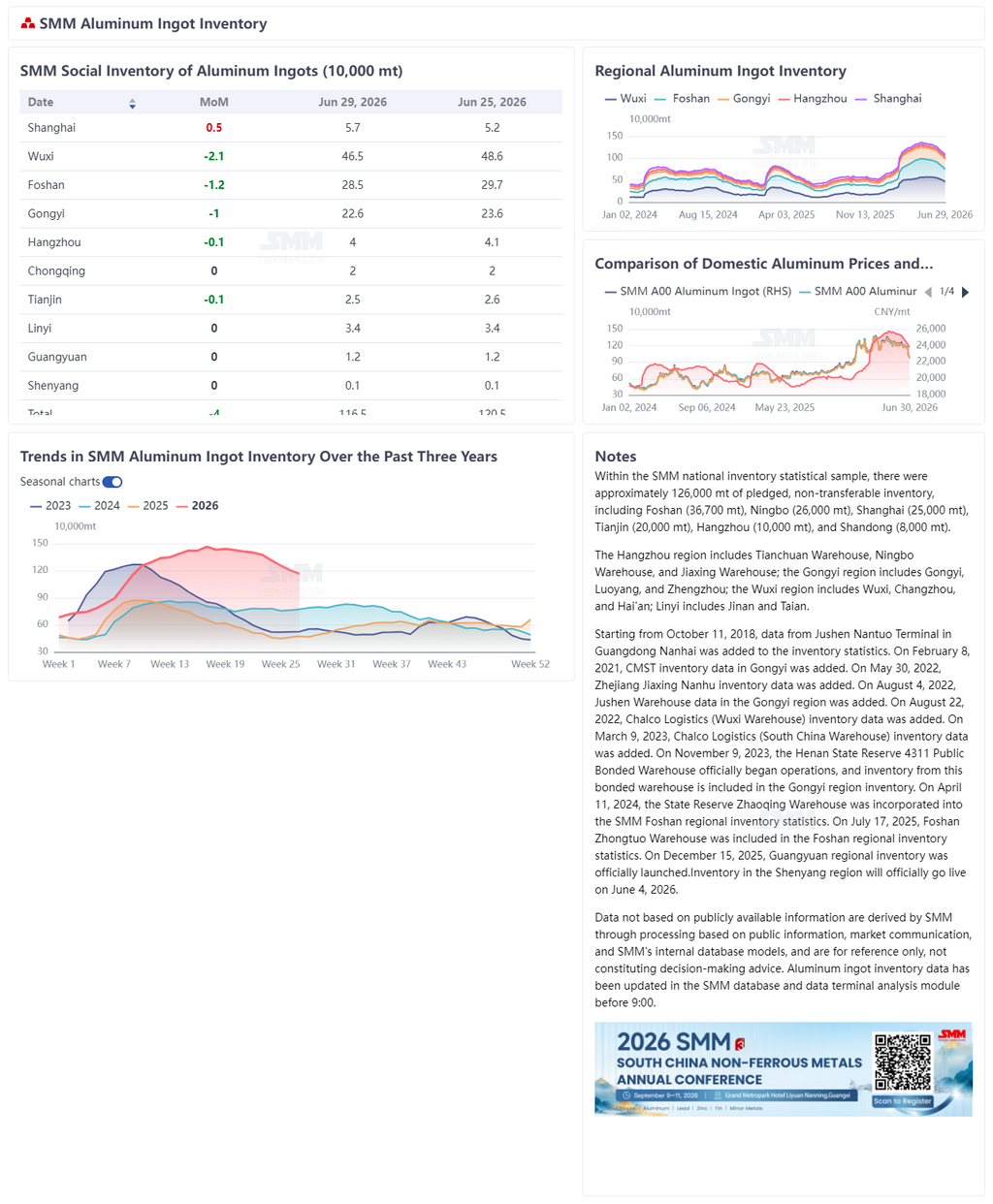

1. Stok Ingot Aluminium: Penurunan 300.000 ton dari Puncak, Laju Pengurangan Stok Meningkat

Menurut SMM, per 30 Juni, stok ingot aluminium China di wilayah konsumsi utama berada di 1.165.000 ton, dengan pengurangan stok mingguan hingga 77.000 ton. Pengurangan stok kumulatif dari puncak tahunan 1.465.000 ton pada awal Mei mencapai 300.000 ton. Pengurangan stok tetap kuat minggu ini—kecuali Shanghai yang terganggu pasokan impor, semua wilayah lain mengalami pengurangan stok secara luas, dengan tiga pusat konsumsi utama (Wuxi, Foshan, dan Gongyi) masing-masing mencatat pengurangan stok mingguan lebih dari 10.000 ton.

Dari segi pola musiman, selama tiga tahun terakhir stok ingot aluminium secara konsisten menunjukkan karakteristik siklus penumpukan stok sekitar Tahun Baru Imlek, mencapai puncak sekitar April-Mei, dan secara bertahap mengurangi stok pada kuartal kedua. Puncak 2024 sekitar 880.000 ton, puncak 2025 sekitar 880.000 ton (hampir sama dengan 2024), sementara puncak 2026 mencapai sekitar 1.480.000 ton, sekitar 600.000 ton lebih tinggi dibandingkan dua tahun sebelumnya—level tinggi secara historis secara tahunan, yang menandakan peningkatan tekanan akumulasi pasokan yang signifikan sejak awal tahun ini. Namun, tren stok 2026 jelas berbeda dari dua tahun sebelumnya: meskipun level stok absolut tetap jauh lebih tinggi daripada periode yang sama di dua tahun sebelumnya (sekitar 400.000-450.000 ton lebih tinggi), volume pengurangan stok absolut (300.000 ton) telah melampaui secara substansial pengurangan stok sepanjang tahun pada 2024 dan 2025. Laju pengurangan stok adalah yang paling curam dalam tiga tahun terakhir.

Mengkaji siklus pengurangan stok ini, lajunya berubah dari bertahap menjadi akselerasi: setelah stok mencapai puncak 1.465.000 ton pada awal Mei, laju awal pengurangan stok lambat; mulai pertengahan Juni, pengurangan stok meningkat tajam. Dalam kurang dari tiga minggu dari 11 Juni hingga 30 Juni, stok turun lebih lanjut dari 1.312.000 ton menjadi 1.165.000 ton, dengan pengurangan stok hampir 150.000 ton—rata-rata harian sekitar 7.500 ton—lebih dari dua kali lipat rata-rata harian sekitar 3.000 ton di bulan Mei.

II. Faktor Pendorong: Tiga Kekuatan Beresonansi, Penarikan Gudang Mencapai Level Tertinggi Empat Tahun

1. Sisi Pasokan: Proporsi Aluminium Cair Meningkat, Volume Ingot Tuang Terus Menyusut

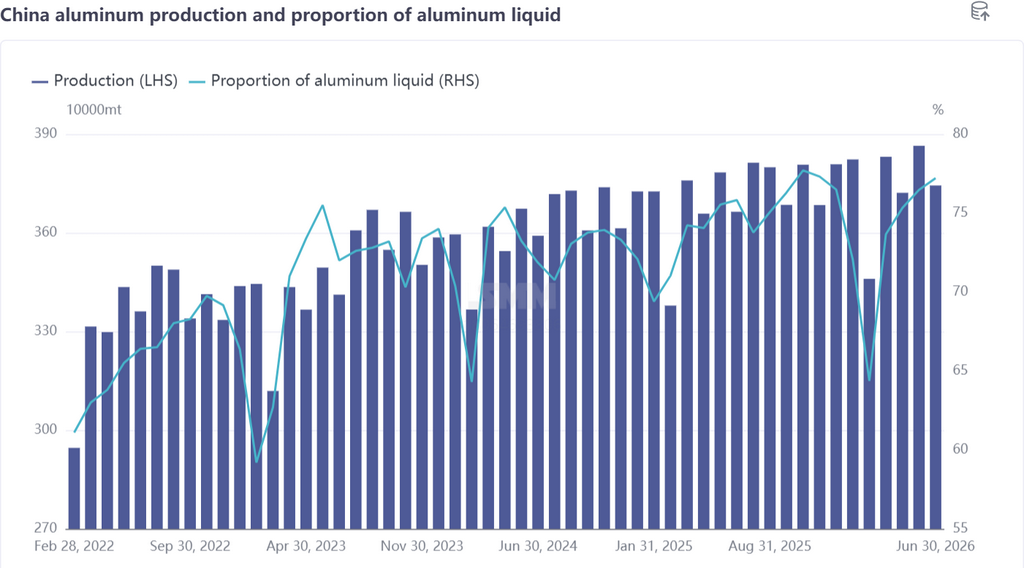

Menurut statistik SMM, output aluminium China pada Juni 2026 (30 hari) meningkat 2,2% YoY dan turun 3,1% MoM. Meskipun permintaan domestik yang lemah menekan berbagai sektor, sehingga secara umum berada di bawah tekanan, permintaan ekspor semis aluminium memberikan dukungan efektif bagi konsumsi aluminium cair domestik. Proporsi aluminium cair sedikit meningkat, dengan rasio bulanan naik 0,7 poin persentase MoM menjadi 77,2%. Pendorong utamanya adalah peningkatan profitabilitas untuk beberapa produk aluminium olahan—terutama biaya pemrosesan billet aluminium yang tetap tinggi, yang mendorong sedikit peningkatan permintaan pengadaan aluminium cair dan secara bersamaan menekan volume ingot tuang. Sementara itu, standardisasi kapasitas aluminium China terus berlanjut, membatasi ruang untuk pertumbuhan pasokan aktual ingot aluminium.

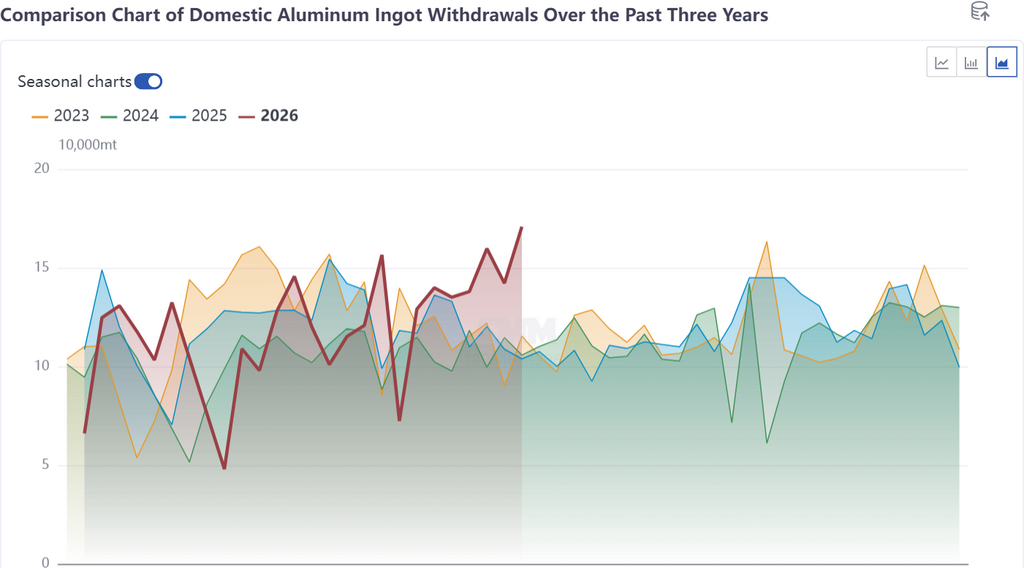

2. Sisi Permintaan: Penarikan Melonjak dalam Pola Denyut, Mencapai Level Tertinggi Hampir Empat Tahun

Minggu ini, penarikan gudang ingot aluminium China melonjak menjadi 170.000 ton (+28.700 ton WoW), mencapai level tertinggi mingguan dalam hampir empat tahun. Dilihat dari pola musiman penarikan gudang selama tiga tahun terakhir, 2026 sebelumnya tidak menunjukkan keunggulan YoY yang jelas, tetapi data terbaru menandai terobosan kualitatif.

Rincian Lonjakan Berdasarkan Wilayah:

Wuxi: Memimpin dengan peningkatan penarikan terbesar, menyumbang sebagian besar kenaikan;

Foshan: Penarikan ikut naik, mencerminkan elastisitas permintaan yang kuat di Tiongkok Selatan;

Gongyi: Penarikan stabil, dengan laju destocking yang relatif ringan.

Namun, lonjakan penarikan tidak mencerminkan pemulihan luas permintaan domestik, melainkan fenomena struktural yang didorong oleh “efek substitusi”. Setelah harga aluminium mundur, keunggulan biaya aluminium ingot dibanding billet menjadi menonjol, mendorong pembeli hilir beralih dari billet ke ingot. Sementara itu, substitusi antara aluminium primer dan skrap alumunium juga berperan—dengan pasokan skrap ketat dan harga tinggi, sebagian perusahaan aluminium sekunder meningkatkan pembelian aluminium primer, semakin mendorong penarikan ingot aluminium.

3. Efek Substitusi: Keterkaitan Segitiga antara Aluminium Ingot, Billet Aluminium, dan Skrap Alumunium

Salah satu pendorong utama di pasar saat ini tetap merupakan substitusi permintaan antara aluminium ingot dan billet aluminium:

Biaya pemrosesan billet aluminium tinggi, dan perusahaan profil hilir, di bawah tekanan biaya, cenderung membeli langsung aluminium ingot untuk dilebur ulang dan diproses;

Tingkat absolut harga aluminium mundur, spread harga spot-futures diperkirakan menguat, dan efektivitas biaya aluminium spot meningkat;

Pasokan skrap alumunium ketat, selisih harga antara logam primer dan skrap menyempit, dan beberapa perusahaan aluminium sekunder meningkatkan proporsi pembelian aluminium primer (aluminium ingot).

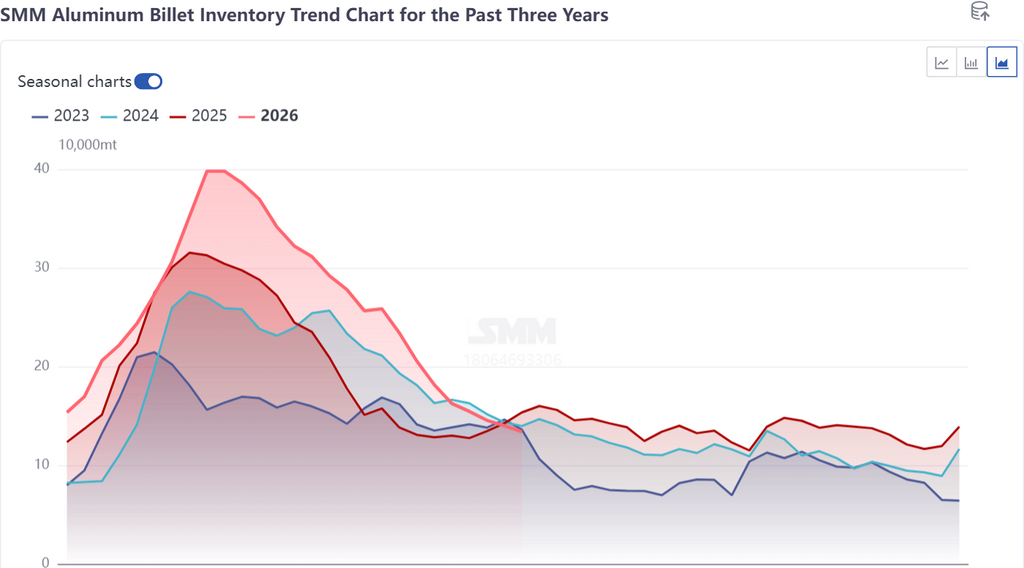

Logika substitusi ini sudah tercermin jelas dalam data inventaris: Saat destocking ingot aluminium meningkat, laju destocking billet aluminium melambat secara nyata. Divergensi antara kedua kurva inventaris ini adalah bukti sampingan bahwa efek substitusi mulai berlaku.

III. Prospek Juli: Logika Destocking Tidak Berubah, Ambang 1 Juta mt di Depan Mata

SMM meyakini bahwa tren destocking untuk inventaris ingot aluminium Tiongkok telah sepenuhnya terbentuk, dengan arah yang tidak berubah. Faktor fundamental berikut akan bersama-sama mendorong kelanjutan destocking:

Proporsi aluminium cair tetap tinggi: Proporsi aluminium cair naik menjadi 77,2% pada bulan Juni dan diperkirakan memiliki sedikit ruang naik di bulan Juli, menjaga produksi ingot cor di bawah tekanan terus-menerus;

Dukungan permintaan ekspor (spesifik pada fase Juni): Kekurangan pasokan aluminium di luar negeri pada Juni mendorong lonjakan pesanan ekspor barang setengah jadi aluminium, secara efektif menyerap kapasitas aluminium cair; namun, pada Juli, seiring menyempitnya selisih harga antara pasar Tiongkok dan luar negeri, momentum ekspor mungkin sedikit melemah;

Normalisasi pasokan: Kemajuan normalisasi kapasitas aluminium Tiongkok membatasi ruang pertumbuhan produksi, dengan tekanan sisi pasokan ingot aluminium yang relatif kecil;

Efek substitusi berlanjut: Biaya pemrosesan billet aluminium yang tinggi dan pasokan skrap aluminium yang ketat kemungkinan tidak akan mereda dalam jangka pendek, menyisakan ruang untuk permintaan substitusi lebih lanjut bagi ingot aluminium.

Jika laju pengosongan stok pada Juli mempertahankan kemiringan saat ini, stok diperkirakan akan turun kembali di bawah 1,1 juta ton pada pertengahan Juli, dan dapat mencapai serta turun di bawah angka 1 juta ton pada akhir bulan. Pada titik itu, level stok absolut akan bergeser dari "tertinggi dalam tiga tahun terakhir" ke kondisi di mana kesenjangan dengan periode yang sama pada 2024-2025 menyempit secara signifikan. Namun, perlu dicatat bahwa Juli adalah musim sepi konsumsi tradisional, dan apakah laju pengosongan stok dapat terus meningkat masih belum pasti. Poin verifikasi utama adalah apakah penarikan dari gudang dapat bertahan di atas 130.000 ton.

Indikator pengamatan utama: ① Apakah tingkat operasi mingguan ekstrusi aluminium dan sektor hilir lainnya berhenti menurun; ② Apakah penarikan absolut dari gudang di Tiongkok, terutama di Tiongkok timur dan selatan, dapat tetap tinggi; ③ Tren harga aluminium, perubahan selisih harga antara pasar Tiongkok dan luar negeri, dan keberlanjutan kekuatan pesanan ekspor; ④ Ruang untuk kenaikan lebih lanjut proporsi aluminium cair.

![[Auto Association] Delta Metal (Holdings) Limited mengundang Anda untuk menghadiri Konferensi Rantai Pasok Otomotif SMM ASCC2026 (ke-8)](https://imgqn.smm.cn/usercenter/TFHUe20251217171651.jpg)