When asked, "The company extracts the following by-products during copper smelting: rhenium, germanium, indium, gallium, bismuth, selenium, tellurium, platinum, palladium, antimony, and cadmium. Is this true? And what was the annual production of each in tonnes in 2025? Please reply, thank you!" Tongling Nonferrous Metals responded on the investor interaction platform on June 29 that the company fully leverages its comprehensive resource utilization advantages, recovering associated platinum, palladium, rhenium, and other rare and scattered metals during the copper smelting process to enhance by-product profit contribution, and the overall production volume accounts for a relatively small share. The company's overall operating performance of the rare and scattered metals business in 2025 has been reflected in the annual report.

Tongling Nonferrous Metals replied to investor questions on the investor interaction platform on June 29: (1) The company's main business includes copper ore mining and beneficiation, smelting, and copper processing, and it has competitive advantages in mineral resource reserves, copper smelting, and deep processing. It is one of the most comprehensive integrated copper producers in China, with horizontal expansion and vertical extension of its industry chain, giving it a competitive edge in industry chain integration. (2) As of now, the specific projects related to the industrial park mentioned above are still in the preliminary survey and proposal evaluation stage; no final decisions have been made, nor have internal reviews or relevant administrative approval procedures been carried out. There is a degree of uncertainty about project implementation. The company will strictly comply with information disclosure laws, regulations, and regulatory requirements, and will perform its information disclosure obligations in a timely manner when the projects achieve substantive progress and meet disclosure thresholds. All material matters of the company are subject to the formal announcements published on the designated information disclosure media. Investors are advised to invest rationally and be mindful of investment risks. (3) Regarding the client situation of Jinxin Copper Branch, please refer to the company's announcements on statutory information disclosure platforms.

Tongling Nonferrous Metals stated on the investor interaction platform on June 29:The copper wire rod capacity of Jinxin Copper Branch is in the process of gradual release;subsequently, based on market demand and its existing capacity, it will effectively plan capacity to ensure efficient resource allocation. As of now, Jinxin Copper's orders are normal and all operations are proceeding in an orderly manner. For specific orders and shipment volumes, please refer to the company's announcements on the statutory information disclosure platform.

In response to the questions: "1. What was the average selling price of the 6.21 million mt of sulphuric acid produced in 2025? And what were the sales volume and average selling price of sulphuric acid in the first five months of this year? 2. What is the specific reason for the asset impairment loss of 1.627 billion yuan in Q1 2026? With non-ferrous metal prices generally rising, is the company's earlier provision for inventory impairment hiding profits? After the inventory for which impairment has been provided is sold, will profit be restored by an equivalent amount? 3. The company holds 600 million shares of Tongguan Copper Foil. Based on today's closing price of 200 yuan, the equity position has an unrealized gain of 119 billion yuan. Does the company plan to sell at an opportune time to realize the investment gain?" Tongling Nonferrous Metals replied on the investor interaction platform on June 26: 1. Regarding sulphuric acid sales volume and average selling price:Sulphuric acid is a by-product of the company's smelting process,and its selling price is market-oriented, affected by multiple factors including regional supply-demand patterns and demand from downstream fertilizer and chemical industries. The company's overall operating performance of the sulphuric acid business in 2025 has been reflected in the annual report, and 2026 operating data should be referred to in subsequent periodic reports disclosed by the company. The company will continue to monitor the sulphuric acid market and dynamically optimize production and sales pace to maximize the operating profit of by-products. 2. For the reasons for the Q1 2026 asset impairment provision, please refer to the company's Announcement on Asset Impairment Provision (Announcement No.: 2026-024) disclosed on cninfo.com.cn on April 29, 2026. The company strictly follows accounting standards for enterprise accounting treatment, and there is no hiding of profits. According to accounting standards, when inventory for which a price decline provision has been made is subsequently sold, the corresponding inventory price decline provision is simultaneously written off, reducing the current period's operating costs, thereby positively restoring profit for the period. However, it is not an equivalent amount; the write-off amount is capped at the originally provided amount for that inventory and will not generate additional profit beyond the original provision. 3.Tongguan Copper Foil is a controlled subsidiary of the company, and the company holds 72.38% of its equity. Its financial data are fully consolidated into the company's consolidated financial statements.From an accounting perspective, fluctuations in the secondary market share price of a controlled subsidiary represent changes in market valuation only. In cases where equity is not disposed of, or is partially disposed of without losing control, it will not affect the net profit in the company's consolidated statements for the current period. As of now, the company has no plan to sell Tongguan Copper Foil shares opportunistically. If equity disposal is involved in the future, the company will strictly comply with state-owned asset supervision and securities regulatory requirements, fulfilling review procedures and information disclosure obligations.

An investor asked on the investor interaction platform: Dear Board Secretary, regarding the Mirador Phase II (Mirador) Mining Contract Amendment (Adenda), its status was updated from "awaiting signature" to "signed/notification process" when a shareholder inquired on April 21, 2026. May I ask whether ECSA, controlled by the company, has now received formal notification of the signing of the mining contract for the Mirador Phase II copper mine project? Tongling Nonferrous Metals stated on the investor interaction platform on May 21 that as of now, China Railway Construction Tongguan Investment Co., Ltd. (of which ECSA is the main operating entity for the Mirador copper mine) has not yet received formal notification of the signing of the mining contract for the Mirador Phase II copper mine project. Please refer to the company's announcements on the statutory information disclosure platform for updates.

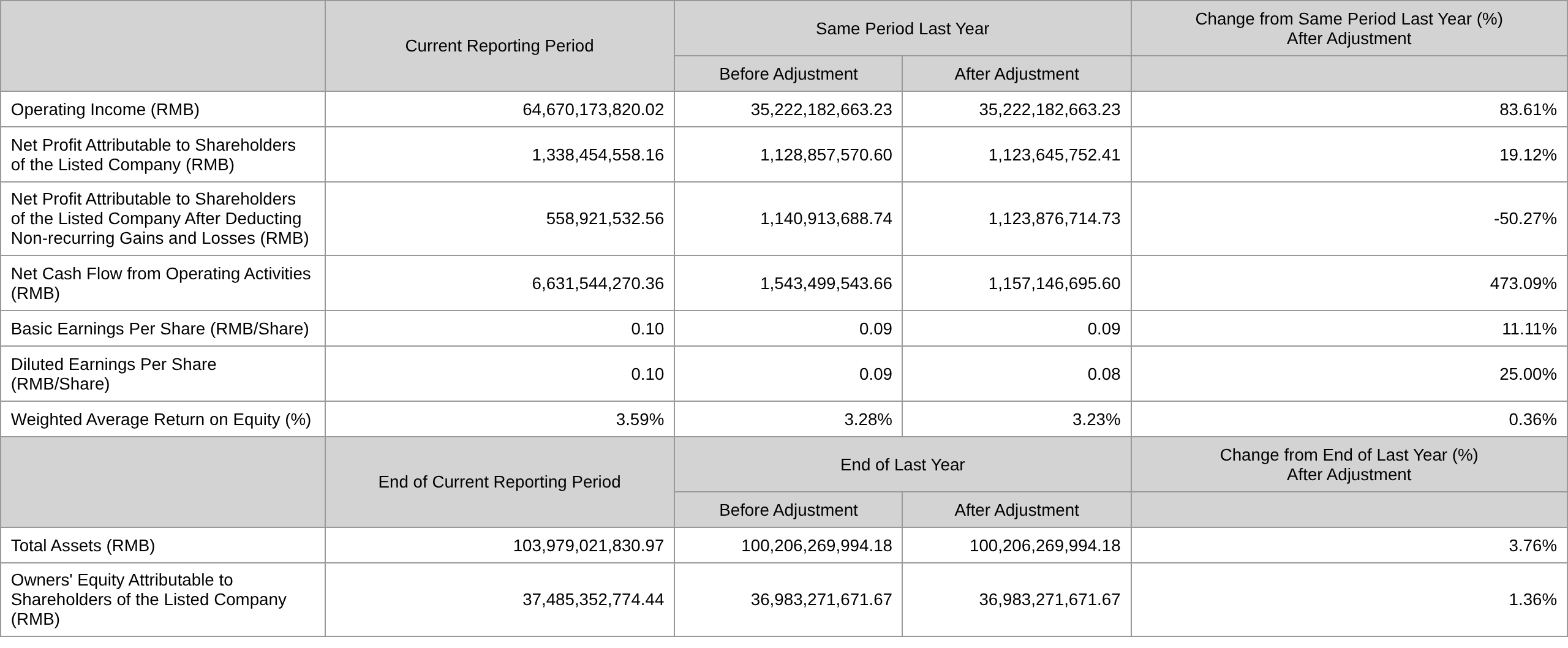

Tongling Nonferrous Metals released its Q1 report showing: The company achieved operating revenue of 64.67 billion yuan in Q1 2026, up 83.61% YoY; net profit attributable to shareholders of the listed company was 1.338 billion yuan, up 19.12% YoY; and net cash flow from operating activities was 6.632 billion yuan, up 473.09% YoY.

Tongling Nonferrous Metals announced in its Q1 report matters concerning project delays at a controlled subsidiary: In recent years, Ecuador's political situation has been volatile with frequent personnel changes, and leadership changes at the competent ministry have led to personnel changes at the working level, greatly affecting policy continuity and administrative efficiency, thereby impacting the progress of signing the Mining Contract for the Mirador Phase II copper mine project. Since 2025, the company and ECSA have strengthened engagement with the relevant authorities of Ecuador's new government through multiple channels and at various levels. The latest round of preliminary negotiations for the Mining Contract for the Mirador Phase II copper mine project has been completed and submitted to the competent ministry for review. Given the significant differences in investment and operating environments between Ecuador and China, the volatile political situation, and the lack of stability in the legal environment, the specific timing for signing the Mining Contract for the Mirador Phase II project is still uncertain. As a result of the aforementioned factors, the formal commissioning of the Mirador Phase II project, once completed, can only commence after its Mining Contract is signed. For details, please refer to the company's Announcement on Subsidiary Project Delay disclosed on cninfo.com.cn on January 5, 2026.

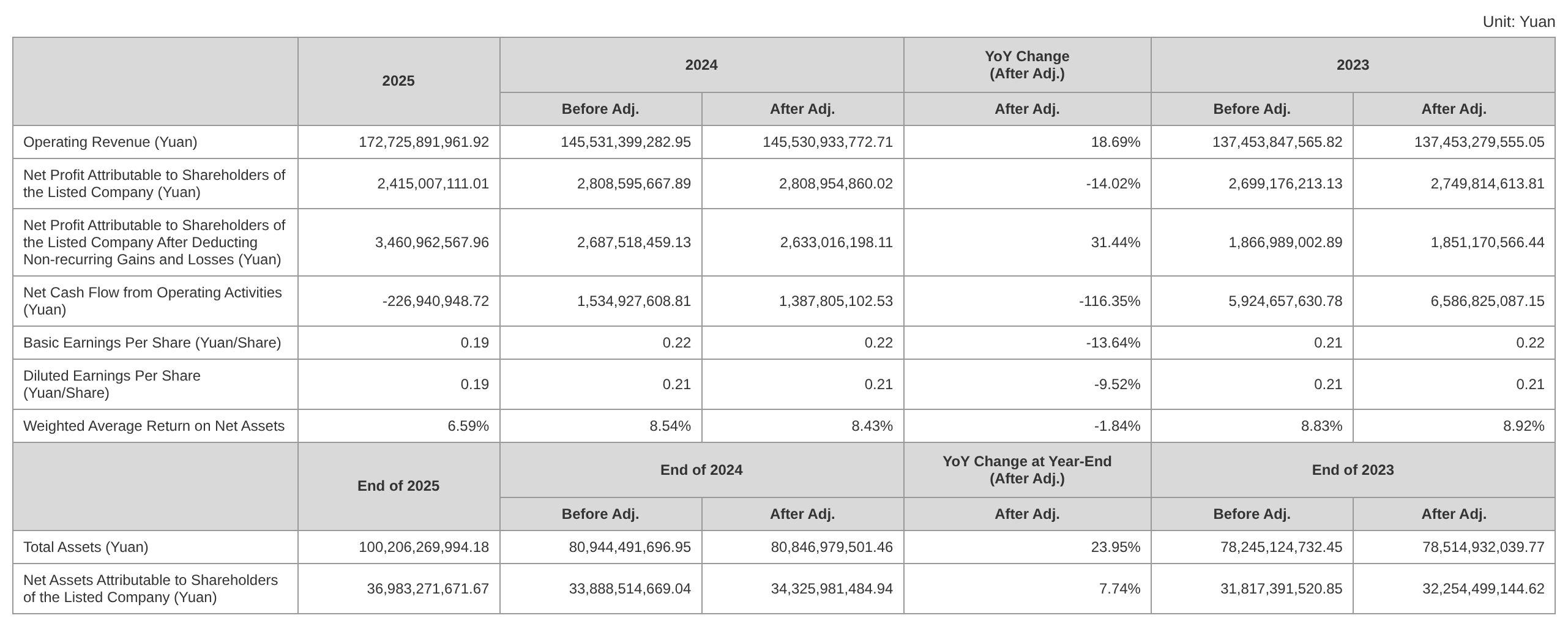

Tongling Nonferrous Metals disclosed in its 2025 annual report: In 2025, the company achieved total operating revenue of 172.825 billion yuan, up 18.68% YoY; net profit attributable to the parent company was 2.415 billion yuan, down 14.02% YoY.

Tongling Nonferrous Metals announced: In 2025, the company overcame unfavourable factors such as tight copper concentrate supply and low TCs, and carried out in-depth activities to increase production and efficiency, and reduce costs and tap potential.In 2025, the company produced 197,700 mt of copper in self-produced copper concentrates, 1.9548 million mt of copper cathode, 400,700 mt of semi-finished copper products, 6.2185 million mt of sulphuric acid, 20.51 mt of gold, 579.55 mt of silver, 376,200 mt of iron ore concentrates, and 382,100 mt of sulphur concentrates, successfully achieving the annual production tasks.

Regarding its main business activities, Tongling Nonferrous Metals stated in its 2025 annual report: The company is a large-scale integrated copper producer covering copper mining and beneficiation, smelting, processing, and trading, with main products including copper cathode, sulphuric acid, gold, silver, copper foil, and copper plate/sheet and strip. The company has deep technical accumulation, a leading industry position, and significant competitive advantages in copper mining and beneficiation, copper smelting, and copper foil processing.

The 2026 operating plan disclosed by Tongling Nonferrous Metals in its 2025 annual report shows: 1. Core operating indicators In 2026, the company will strive to achieve various core product production targets, specifically: 227,600 mt of copper in self-produced copper concentrates, 2.108 million mt of copper cathode, 455,000 mt of semi-finished copper products, 22,000 kg of gold, 650 mt of silver, 7.07 million mt of sulphuric acid, 344,000 mt of iron ore concentrates (60%), and 308,000 mt of sulphur concentrates (35%), anchoring production and operational objectives with quantified indicators.

A research report from Guosen Securities published on April 22 indicated that the company's copper smelting segment's profitability is industry-leading. In 2025, Jinlong Copper achieved a net profit of 800 million yuan; if simply converted by capacity, Jinguan Copper Branch's net profit was approximately 1.22 billion yuan. Excluding the newly commissioned Jinxin Branch, the three existing smelters had a combined annual net profit of 2.64 billion yuan. The decent profit of copper smelters including the company in 2025 can be attributed to factors such as raw material inventory cycles, high sulphuric acid prices, high copper smelting recovery rates, and high prices for by-product gold and silver. Compared with several other large copper smelters, whose main smelters had net profit margins mostly around 0.5%, Tongling Nonferrous Metals' main smelters all had net profit margins around 2%, significantly above the industry average. Mirador Phase II may come online in August. The company expects to produce 228,000 mt of copper concentrates in 2026. Based on past trends, domestic copper ore production is 50,000 mt per year, and Mirador Phase I production is 130,000 mt per year, so Mirador Phase II is scheduled to produce 50,000 mt in 2026, implying production start-up around August 2026. In 2025, China Railway Construction Tongguan Investment achieved a net profit of 1.93 billion yuan, and the Mirador project company reached a net profit of 3.79 billion yuan, demonstrating strong profitability. Mirador Phase II mining and beneficiation costs are only about 70% of Phase I. If Phase I costs are 28,000 yuan/mt, a rough calculation puts Phase II costs at 19,600 yuan/mt. If by-product gold and silver partially offset copper costs, Mirador Phase II costs could be negative. Risk warnings: risk of wild swings in copper prices, risk of copper concentrate TC declines.

![[SMM Steel] 7.24 SMM Global Steel Daily Report](https://imgqn.smm.cn/usercenter/zbJUC20251217171718.jpg)