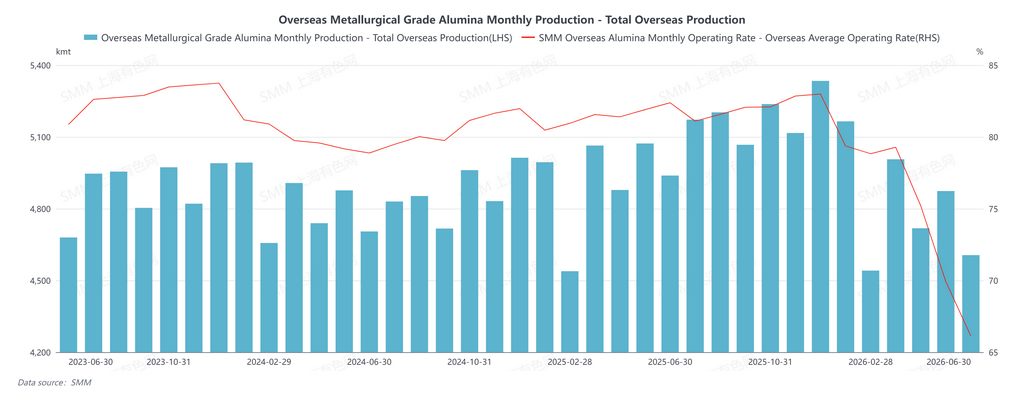

According to SMM statistics, overseas metallurgical-grade alumina output in June 2026 fell by around 6.0% YoY and 5.5% MoM. Supply-side disruptions in the overseas alumina market became more evident compared with May. On the one hand, affected by tensions in the Middle East, production and shipment schedules at some producers have yet to fully recover. On the other hand, weather-related disruptions and natural gas supply issues in Australia continued to weigh on local alumina output and shipments.

By company and region, Alcoa said that due to the impact of Cyclone Narelle in Australia, LNG supply to its Pinjarra alumina refinery in Western Australia was temporarily disrupted. As a result, the company expects its alumina shipments in Q2 to decrease by around 120,000 mt compared with Q1, while the disruption is expected to increase Q2 production costs by around $30 million. In addition, due to tensions in the Middle East, fuel costs at the company’s São Luís alumina refinery in Brazil also increased. Alcoa’s Western Australia alumina operations are currently under significant pressure from weak alumina prices, declining bauxite grades and rising energy costs.

In Europe, geopolitical risks continued to escalate. During the EU’s new round of discussions on sanctions against Russia in June, exports of alumina from Ireland’s Aughinish Alumina to Russia remained under scrutiny. Public reports showed that alumina exports were not included in the latest EU sanctions package for the time being. However, if sanctions are tightened further, this could affect European alumina trade flows and the regional supply landscape.

Entering June, with some Malaysian bauxite cargoes arriving, feedstock availability improved at certain alumina refineries in Indonesia, creating room for a subsequent recovery in output. However, Indonesia’s bauxite quota policy and logistics stability still need to be closely monitored.

In addition, Tajikistan and Azerbaijan also discussed cooperation in alumina supply and aluminium product trade in June. Under the proposed arrangement, Azerbaijan would supply alumina to Tajikistan, while Tajikistan would export aluminium products to Azerbaijan. This cooperation is expected to have limited impact on overseas alumina output in the short term, but it reflects ongoing regional aluminium industry chain coordination and adjustments in trade flows.

Looking ahead to July, overseas metallurgical-grade alumina supply is expected to see a recovery, with output likely to rise by around 4.5% MoM. On the one hand, raw material constraints at some Indonesian alumina refineries have eased following the arrival of bauxite cargoes, and output is expected to recover gradually. On the other hand, weather-related and natural gas supply disruptions in Australia are easing at the margin, which may support the recovery of previously affected production and shipment schedules. However, geopolitical risks in the Middle East, uncertainty over EU sanctions against Russia, energy cost pressure in Australia, and Indonesia’s bauxite quota issues may continue to disrupt the recovery of overseas supply. Overall, overseas alumina output is expected to rebound slightly in July, but supply-side uncertainty remains relatively high.

![Aluminum Fluoride Prices Consolidate Amid High Raw Material Costs and Weak Downstream Demand [SMM Analysis]](https://imgqn.smm.cn/usercenter/kRRxA20251217171652.jpg)