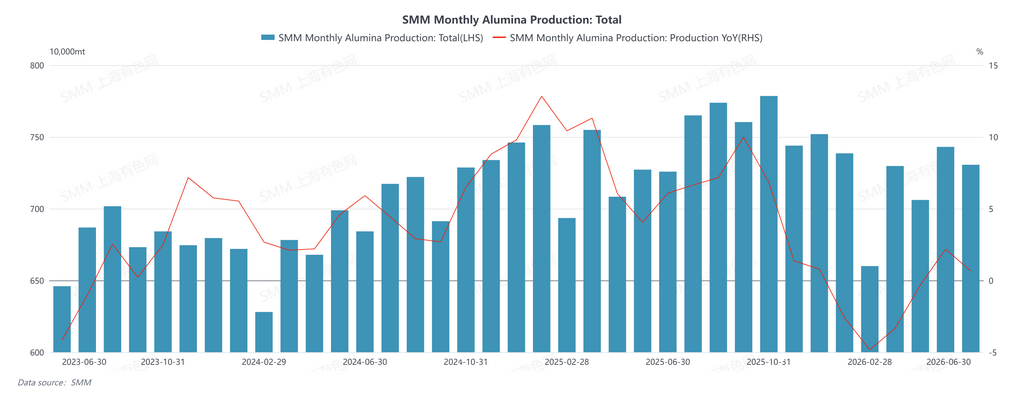

SMM, June 30

In June 2026, China’s metallurgical-grade alumina output fell 1.7% MoM but rose 0.7% YoY. As of the end of June, China’s total built alumina capacity stood at around 118.42 million mt/year. Operating capacity increased 1.6% MoM and 0.7% YoY.

The change in output this month was mainly driven by the offset between new capacity ramp-up and localised production cuts. On the one hand, the second production line of a newly commissioned project in Guangxi continued to ramp up, supporting an increase in alumina output in south China. On the other hand, some capacity in Shanxi was temporarily reduced due to environmental protection-related factors, partially offsetting the output increase from new capacity. Meanwhile, as some calciners in north China completed maintenance, output at relevant producers recovered to some extent. Overall, alumina output in north China edged lower in June, while output in south China increased.

Looking ahead to July, the alumina market is expected to maintain its current supply pattern. Some alumina producers in Guangxi are expected to complete boiler maintenance, which may further lift output in the region. However, affected by the mining accident in Shanxi, domestic bauxite mining has been restricted to some extent. Tight domestic ore supply has prompted some alumina producers that mainly use domestic bauxite to adjust their production plans. In addition, with alumina inventories still at high levels, some producers may arrange maintenance going forward. Overall, alumina operating capacity in July is expected to be around 88.60 million mt/year.

![Aluminum Fluoride Prices Consolidate Amid High Raw Material Costs and Weak Downstream Demand [SMM Analysis]](https://imgqn.smm.cn/usercenter/kRRxA20251217171652.jpg)