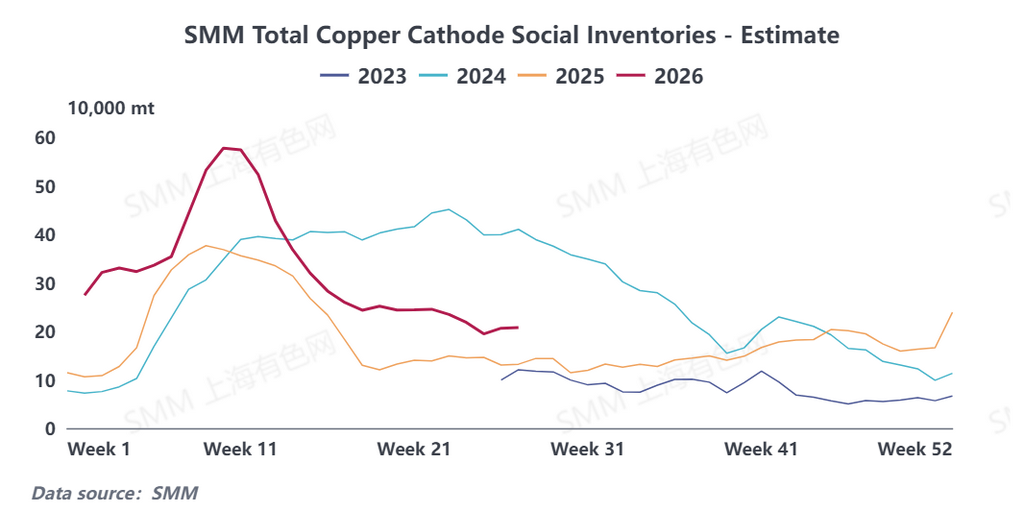

As of Thursday, June 25, social copper inventories in major regions of China increased by 11,700 mt WoW to 206,000 mt, while regional inventory trends diverged significantly. Copper price pullbacks have spurred a recovery in downstream purchasing demand, and coupled with ongoing adjustments in the market's supply-demand pattern, inventory performance varied across regions.

By region, inventory trends in China's key copper consumption areas showed pronounced divergence. In Shanghai and Jiangsu, the two core markets, inventories pulled back in tandem, signaling a notable recovery in demand. Recently, domestic copper prices fell sharply, with lower prices effectively stimulating downstream enterprises' restocking willingness. In Shanghai, buoyed by favorable prices, downstream purchasing activity increased significantly, continuously drawing down spot inventories; meanwhile, combined with relatively low regional arrivals in the prior period, the market maintained a destocking pattern. Jiangsu's market situation was largely in line with Shanghai's—falling copper prices prompted end-users to concentrate on pricing and purchasing, with rigid-demand orders released intensively, effectively driving steady destocking of regional inventories and markedly improving spot market liquidity.

In stark contrast to Shanghai and Jiangsu, inventories in Guangdong continued to climb, becoming the main drag on the national inventory increase. According to market analysis, as the year entered the mid-year phase, consumption by downstream copper semis enterprises in Guangdong gradually slowed, end-user order growth pulled back, and overall willingness to purchase remained weak. Meanwhile, domestic smelters accelerated their shipment pace, concentrating deliveries into Guangdong warehouses, driving a significant increase in regional arrivals. Under the dual impact of weakening downstream consumption and concentrated inflows of upstream supply, copper inventories in Guangdong continued to accumulate.

Looking ahead, China's copper market will see structural adjustments on both supply and demand sides in the short term, with a destocking trend essentially in place. On the supply side, the domestic copper cathode market has recently seen somewhat looser supply, with port arrivals of imported cathode steadily rising. Meanwhile, domestic smelters have maintained steady production and shipment pace, with domestic supply arrivals continuing to increase, resulting in ample overall spot supply.

The outlook for demand improvement is more definitive. After this round of sharp copper price declines, downstream enterprises' cost pressure has eased significantly. Coupled with previously accumulated orders on hand awaiting execution, market stockpiling sentiment continues to recover, and end-user restocking demand for rigid needs is set to be released intensively, continuously consuming spot cargo circulating in the market.

Overall, the current domestic copper spot market is characterized by a favorable pattern of "ample supply and recovering demand," with downstream restocking momentum sufficient to offset pressure from short-term new supply. SMM expects that next week, national copper social inventories will shift to a destocking pace, and overall inventories are likely to pull back steadily. Going forward, the market should closely monitor the magnitude of copper price fluctuations, the sustainability of downstream purchasing intensity, and the pace of imported supply arrivals.

![[SMM Analysis]Canada’s Sulfur Export Data – 2026 Exports Projected at 5.2 Million Tons](https://imgqn.smm.cn/usercenter/uoTGi20251217171713.jpg)