SMM News, June 30:

In the metals market:

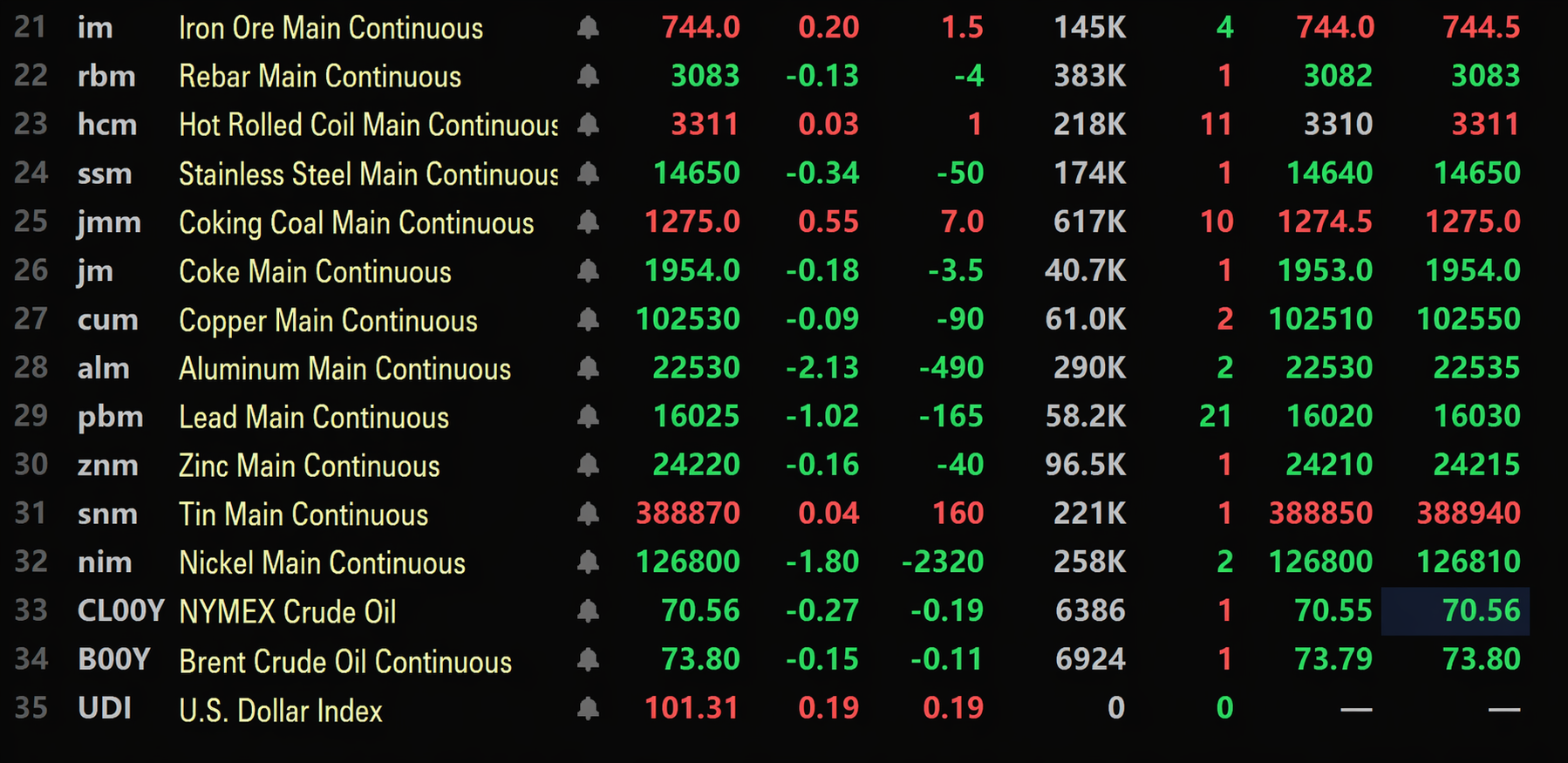

As of the midday close, base metals in the domestic market generally fell. SHFE copper edged down, SHFE aluminum fell 2.13%, SHFE lead fell 1.02%, SHFE zinc fell 0.16%, SHFE tin edged up, and SHFE nickel fell 1.8%.

Additionally, the most-traded cast aluminum futures contract fell 1.41%, the most-traded alumina contract fell 1.56%, the most-traded lithium carbonate contract rose 4.82%, the most-traded silicon metal contract rose 0.24%, and the most-traded polysilicon futures contract rose 0.8%.

Ferrous metals showed mixed performance. Iron ore rose 0.2%, HRC edged up, rebar fell 0.13%, and stainless steel fell 0.34%. For coking coal and coke: the most-traded coking coal contract rose 0.55%, and the most-traded coke contract fell 0.18%.

In the overseas base metals market, as of 11:36, LME metals showed mixed performance. LME copper fell 0.24%, LME aluminum edged up, LME lead fell 0.18%, LME zinc fell 0.19%, LME tin rose 0.44%, and LME nickel rose 0.34%.

In precious metals, as of 11:36, COMEX gold fell 1.48%, COMEX silver fell 1.19%. In domestic precious metals: SHFE gold fell 2.67%; the most-traded SHFE silver contract fell 2.16%.

Additionally, as of the midday close, the most-traded platinum futures contract fell 3.29%, and the most-traded palladium futures contract was flat at 290.65 yuan/g.

As of the midday close, the most-traded container shipping (European route) futures contract fell 1.7% to 3,662.5 points.

As of 11:36 on June 30, some futures midday quotes:

Spot and Fundamentals

Zinc: In the Tianjin market, #0 zinc ingot mainstream traded at 24,030-24,250 yuan/mt, Zijin traded at 24,220-24,530 yuan/mt, #1 zinc ingot traded around 24,100-24,240 yuan/mt, Zijin against the 2608 contract reported a discount of around 30-40 yuan/mt, Huxin quoted at 25,090 yuan/mt, #0 zinc ingot against the 2608 contract reported a discount of around 50-100 yuan/mt, Tianjin market versus Shanghai market reported a discount of around 40 yuan/mt. Today contract rollover quotations...

Macro Front

Domestic side:

[National Bureau of Statistics: June manufacturing PMI at 50.3%, China's economic prosperity level rebounded somewhat] According to NBS data, in June, the manufacturing PMI was 50.3%, up 0.3 percentage points from the previous month, returning to expansion territory. By enterprise size, large enterprises' PMI was 50.7%, down 0.4 percentage points month-on-month, still above the threshold; medium-sized enterprises' PMI was 50.5%, up 1.9 percentage points from the previous month, above the threshold; small enterprises' PMI was 48.2%, down 0.3 percentage points month-on-month, below the threshold. From the sub-indexes perspective, among the five sub-indexes that constitute the manufacturing PMI, the production index and new orders index were above the threshold, while the raw material inventory index, employment index, and supplier delivery time index were all below the threshold. Huo Lihui, chief statistician of the Service Survey Center at the National Bureau of Statistics (NBS), commented on China's PMI for June 2026: In June, the non-manufacturing business activity index stood at 50.2%, up 0.1 percentage point from the previous month, indicating a rebound in non-manufacturing activity. The expansion in the services sector accelerated. The services business activity index was 50.4%, up 0.1 percentage point from the previous month, showing an improvement in activity. By industry, business activity indexes for sectors such as telecommunication, radio and television, and satellite transmission services; internet, software, and information technology services; monetary and financial services; and insurance were all in the higher expansion zone above 55.0%, with relatively rapid growth in business volume. The indexes for air transport and real estate remained below the threshold. The services business activity expectations index was 56.0%, up 0.6 percentage point from the previous month, indicating improving expectations among enterprises regarding market development. The construction sector saw some improvement. The construction business activity index was 49.0%, up 0.2 percentage point from the previous month, a marginal rebound. The construction business activity expectations index was 51.1%, continuing to indicate expansion.

[PBOC conducts 669.5 billion yuan reverse repo in open market, net withdrawal of 155 billion yuan for the day] The PBOC conducted a 69.5 billion yuan 7-day reverse repo operation today, with an operation rate of 1.4%, unchanged from before. Today, 524.5 billion yuan 7-day reverse repos mature. At the same time, the PBOC conducted a 600 billion yuan overnight reverse repo operation, and today 300 billion yuan overnight reverse repos mature.

On the US dollar front:

As of 11:36, the US dollar index rose 0.19% to 101.31. The US Supreme Court blocked Trump's attempt to fire Federal Reserve Governor Cook; the move was a forceful rebuke to the president's attack on the world's most important central bank. The 5-4 ruling is the latest major check on the Trump administration by the Supreme Court. Earlier this year, the court also ruled that the president does not have the authority to impose tariffs using emergency powers, a decision that shook a key pillar of the Trump administration's economic policy. The ruling released on Monday rejected the first-ever attempt by a US president to remove a Fed governor; critics have warned that such a move would undermine the central bank's independence. However, on Monday the US Supreme Court also cleared the way for Trump to fire Federal Trade Commission (FTC) members without cause; a move that grants the White House greater power and tightens control over independent regulatory agencies.

According to CME FedWatch: The probability of the Fed keeping rates unchanged in July is 70.1%, and that of a cumulative 25bp hike is 29.9%. For September, the probability of unchanged rates is 37.2%, that of a 25bp cumulative hike is 48.8%, and that of a 50bp hike is 14.1%. (Jin10 Data APP)

Data:

Today’s releases include the US FHFA House Price Index MoM for April, the US S&P/Case-Shiller 20-City Home Price Index NSA YoY for April, the US Chicago PMI for June, the US JOLTS Job Openings for May, the US Conference Board Consumer Confidence Index for June, the UK Q1 GDP YoY Final, the UK Q1 Current Account, Germany’s June seasonally adjusted unemployment change, Germany’s June seasonally adjusted unemployment rate, Germany’s June CPI MoM Preliminary, France’s June CPI MoM Preliminary, Switzerland’s June KOF Economic Barometer, Canada’s April GDP MoM, Japan’s May unemployment rate, and other data.

Also, watch for: ECB President Lagarde delivers opening remarks at the ECB Forum on Central Banking in Sintra, the Reserve Bank of Australia releases the minutes of its June monetary policy meeting, and the US and Iran hold technical negotiations.

It is also worth noting that on July 1, the Hong Kong Stock Exchange will be closed for the Hong Kong Special Administrative Region Establishment Day, with northbound and southbound trading shut. The Toronto Stock Exchange will be closed for Canada Day.

Other currencies:

The minutes of the Reserve Bank of Australia’s June meeting showed the bank believed monetary policy needed to remain tight to eliminate surplus demand in the economy. As the minutes were compiled before Brent crude prices fell more than 10% last week, the hawkish tone reflected in them has become notably disconnected from current market moves. Currently, the market is pricing in only 10bp of further tightening by year-end, while the probability of easing by 2027 stands at 17bp. The tension for the Australian dollar lies in that, on one hand, the RBA clearly stated it is prepared to hike again if needed; on the other, the market believes rates have likely peaked. If upcoming data confirms that weaker oil prices are gradually feeding through to inflation expectations, the Australian dollar could face a repricing. Meanwhile, falling house prices in Sydney and Melbourne are adding to domestic growth risks and could reinforce the market’s dovish repricing, even as the RBA board’s rhetoric remains distinctly hawkish.((Jinshi Data APP)

Crude oil:

As of 11:36, oil prices in both markets edged down, with WTI falling 0.27% and Brent down 0.15%. The market was focused on possible talks between the US and Iran.

An Iranian Foreign Ministry spokesperson said that Iran’s top priority at that time was to ensure the implementation of all provisions of the memorandum of understanding. With regard to Article 10 of the memorandum concerning the US commitment to allow Iranian oil exports, the US side had already issued the necessary permits, and Iran was following up on the implementation progress. As for Article 11 regarding the unfreezing of Iranian assets, the relevant implementation procedures were also progressing. This week, Iran would send a technical delegation to Qatar for consultations on the implementation of the memorandum of understanding, including Article 11. The spokesperson said that Iran had not yet initiated negotiations on a final agreement. According to Article 13 of the memorandum, the precondition for initiating final agreement negotiations was the commencement and continued implementation of Articles 1, 4, 5, 10, and 11. Furthermore, the spokesperson stressed that there would be no negotiations at any level between Iran and the US in the coming days. The trip by US representatives to Qatar was unrelated to the Iranian technical delegation’s visit; the Iranian delegation’s purpose in going to Qatar was to follow up on the implementation of the memorandum of understanding, including Article 11. (CCTV)

According to trade sources and a document, Iraq’s State Oil Marketing Organization (SOMO) had sharply reduced its official selling prices to attract long-term buyers to lift Basrah crude from its terminals in the Middle East Gulf in July. The discount for Basrah Medium was $14 to $16 per barrel, and for Basrah Heavy, it was $16.8 to $18.8 per barrel, depending on the loading date. Discounts were larger for loadings from July 1 to 5, and smaller for loadings from July 6 to 10, and from July 11 to 31. SOMO said that buyers needed to submit their order quantities within one day of receiving the notification letter. Trade sources said that the steep discounts might attract buyers, but it remained to be seen whether passage through the Strait of Hormuz would be possible. (Jinshi Data APP)

According to data from the US Department of Energy (DOE), crude oil inventories in the US Strategic Petroleum Reserve (SPR) fell by 5.5 million barrels to 325.7 million barrels, the lowest level since May 1983. The inventory decline was part of a US agreement to release 172 million barrels of crude from the reserve to fill a gap in global inventories following the Iran conflict and help push down fuel prices. US crude inventories fell rapidly in recent weeks due to strong crude exports and refining demand. From the outbreak of the conflict in late February to June 19, total US inventories, including commercial stocks and the SPR, had fallen by 111.4 million barrels to 743.3 million barrels, the lowest level since 1984. (Jin10 Data APP)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

►

![[SMM Flash News] Indonesia's Industry Ministry to Establish National Industrial Zone Council Led by the President](https://imgqn.smm.cn/usercenter/SSKOK20251217171734.jpeg)

![Shanghai Spot Copper Premiums Remain Under Pressure amid Weak Month-End Consumption [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/aMTzL20251217171710.jpg)

![Bullish and bearish factors interweave and SHFE tin maintains wild swings, while downstream enterprises' purchase willingness is currently weak [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/tyydv20251217171753.jpg)