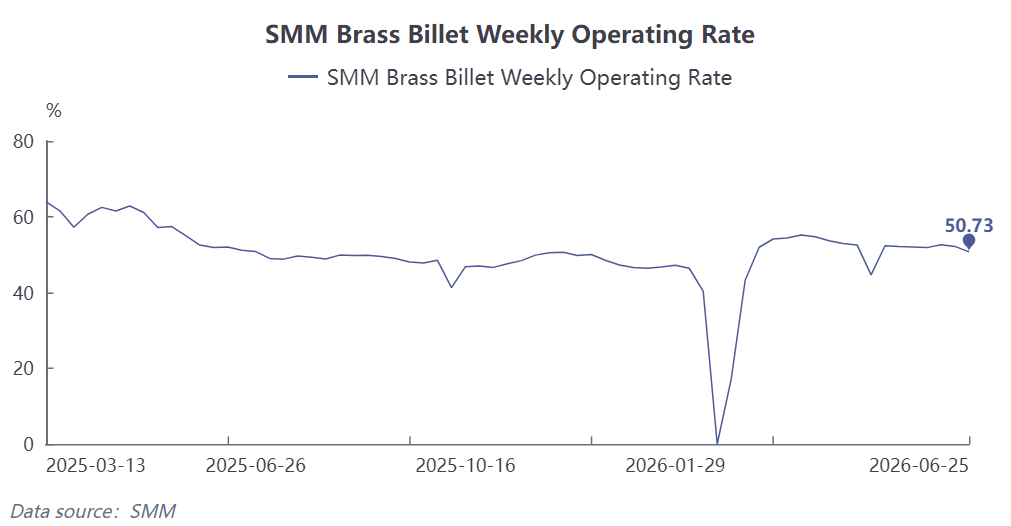

The brass billet industry is currently deep in the traditional consumption off-season. Weighed down by weak demand, tight raw material supply, and fluctuating costs, production in the sector remained under pressure. According to SMM data, the operating rate of China’s brass billet industry fell to 50.73% last week, down 1.44 percentage points MoM, broadly in line with earlier forecasts.

The tight supply of recycled brass raw materials saw no significant improvement. Imported and domestic secondary brass remained at low circulation levels, keeping procurement difficulties high. Although copper prices pulled back at certain stages, prompting some producers to engage in limited stockpiling and driving raw material inventory days at sampled enterprises slightly higher to 3.84 days, most firms were generally concerned about insufficient processing margins and refrained from large-scale restocking. Most factories only purchased raw materials as needed, maintaining low inventory levels for production. Raw material shortages continued to constrain capacity release at small and medium-sized producers.

Meanwhile, the off-season effect fully materialized among downstream end-users in the home appliance, sanitary ware, and hardware fittings sectors. The overall procurement pace continued to slow down. The vast majority of brass billet producers could only sustain production schedules with existing past orders, while new orders were few and far between.

Last week, only after a sharp pullback in copper prices did long-waiting downstream players ease slightly, releasing a concentrated batch of small-scale restocking orders based on rigid demand. However, the incremental order volume was extremely limited, nowhere near enough to reverse the overall pattern of sluggish transactions. With downstream cargo pick-up slow, finished product destocking was hindered. Finished product inventory days at sampled enterprises remained at 5.32 days, and the financial pressure from inventory buildup persisted.

Looking ahead to this week (6.26–7.02), the traditional industry off-season is unlikely to end quickly. End-users will likely remain cautious and on the sidelines amid consolidating copper prices, making it difficult for orders to see a meaningful recovery. The tightness in recycled brass raw material supply is also unlikely to ease in the near term, with persistent cost disruptions. SMM expects the operating rate of brass billet producers to edge up 0.29 percentage points MoM to 51.02% this week. Overall industry production schedules will remain low, and operational pressures on enterprises are unlikely to ease in the short term.

![Sluggish Trading on the Mid-Year Settlement Day, with Neither Buyers nor Sellers Being Active [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/kvwSZ20251217171710.jpg)

![Copper prices pull back slightly and weaken, while month-end downstream wait-and-see keeps discounts steady [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/vcsIC20251217171710.jpg)

![[SMM Flash] Kazakhstan Follows Russia in Full Suspension of Sulfur Exports](https://imgqn.smm.cn/usercenter/fEiiq20251217171711.jpg)