I. Kịch bản 1: Áp dụng đầy đủ thuế đồng tinh luyện

Nếu Bộ Thương mại Hoa Kỳ chính thức xác nhận lộ trình thuế quan đối với đồng tinh luyện vào ngày 30 tháng 6, thị trường sẽ định giá lại nguồn cung đồng của Mỹ thay vì chỉ đơn thuần phản ứng với mức thuế suất.

Các biện pháp theo Mục 232 hiện nay chủ yếu bao phủ các sản phẩm đồng bán thành phẩm và sản phẩm phái sinh chứa hàm lượng đồng cao. Catốt đồng tinh luyện, tinh quặng đồng, anốt đồng và phế liệu đồng vẫn nằm ngoài phạm vi của mức thuế 50% hiện hành. Vấn đề then chốt là liệu Chính quyền có xác nhận lộ trình thuế quan theo giai đoạn được đề xuất gồm 15% vào năm 2027 và 30% vào năm 2028 đối với nhập khẩu đồng tinh luyện hay không.

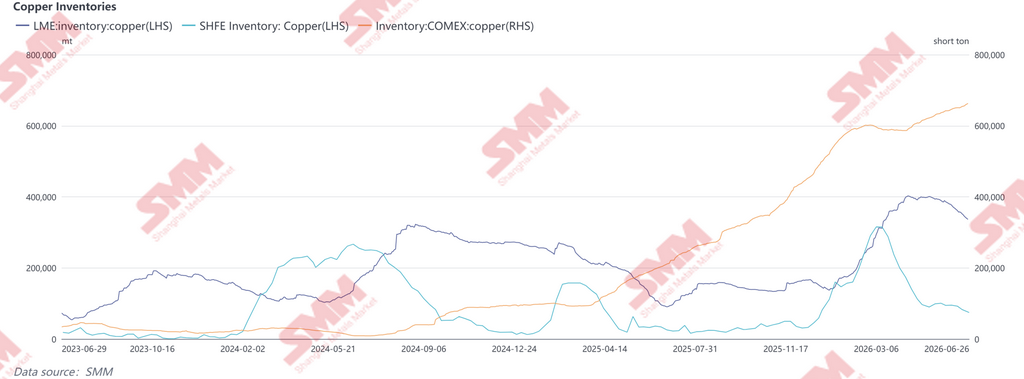

Nếu được thực thi, thị trường giao ngay Mỹ có khả năng phản ứng đầu tiên. Lượng tồn kho COMEX tăng mạnh trong những tháng gần đây phần lớn đến từ nhập khẩu trước hạn và kinh doanh chênh lệch liên thị trường nhằm đón đầu khả năng áp thuế. Sau khi xác nhận, lượng tồn kho này dự kiến sẽ đóng vai trò như lớp đệm cung ngắn hạn, làm dịu tình trạng thắt chặt tức thời tại thị trường nội địa. Tuy vậy, chi phí thay thế cao hơn cho nhập khẩu trong tương lai nhiều khả năng sẽ duy trì mức chênh lệch giá cơ cấu của COMEX so với LME.

Các chuyến hàng đồng tinh luyện truyền thống từ Chile và Peru vào Mỹ cũng có thể bị ảnh hưởng. Khi thuế quan bào mòn tính kinh tế của nhập khẩu, một phần khối lượng này có thể chuyển hướng sang châu Á và châu Âu, làm gia tăng nguồn cung ngắn hạn bên ngoài nước Mỹ, đồng thời gây áp lực tương đối lên giá LME và SHFE, nới rộng chênh lệch giữa các khu vực thị trường.

Sau cùng, tác động sẽ lan từ các luồng thương mại thượng nguồn sang lĩnh vực sản xuất hạ nguồn. Đồng không còn đơn thuần là kim loại công nghiệp – nó đã trở thành đầu vào chiến lược cho hạ tầng AI, điện khí hóa và sản xuất tiên tiến.

II. Kịch bản 2: Thuế quan có chủ đích hoặc theo từng giai đoạn

Nếu Washington không áp thuế toàn diện lên đồng tinh luyện mà thay vào đó chọn các biện pháp mang tính mục tiêu dựa trên mã số HTS, nước xuất xứ, độ tinh khiết hoặc dạng sản phẩm, tác động thị trường có thể khó thấy rõ hơn nhưng lại gây gián đoạn chuỗi cung ứng toàn cầu một cách đáng kể.

Rủi ro đầu tiên nằm ở phế liệu đồng. Nếu Hoa Kỳ siết chặt hạn chế xuất khẩu phế liệu chất lượng cao, hoặc áp hạn ngạch, thuế quan hay xác minh xuất xứ chặt chẽ hơn đối với hàng trung chuyển, dòng đồng thứ cấp toàn cầu có thể sẽ được tái cơ cấu sâu rộng. Phế liệu chất lượng cao của Mỹ từ lâu đã là nguyên liệu đầu vào quan trọng cho các ngành công nghiệp đồng tái chế của Trung Quốc và Đông Nam Á. Bất kỳ hạn chế xuất khẩu nào cũng sẽ thu hẹp biên lợi nhuận chế biến tại Malaysia, Thái Lan và Việt Nam, đồng thời thắt chặt nguồn cung nguyên liệu đồng tái chế tại Trung Quốc.

Rủi ro thứ hai liên quan đến chênh lệch giá theo xuất xứ. Nếu các nước thành viên USMCA được hưởng ưu đãi hoặc miễn trừ, Mexico và Canada có thể nổi lên thành các trung tâm tái phân phối đồng tinh luyện trong khu vực. Giới thương nhân có thể ngày càng định tuyến lại các chuyến hàng qua những thị trường này để tối ưu hóa mức thuế phải chịu, khiến cho quy tắc xuất xứ, yêu cầu chuyển đổi đáng kể và phân loại HTS trở nên quan trọng hơn chính con số thuế suất danh nghĩa.

Hệ quả thứ ba là sự phân mảnh ngày càng tăng của chuỗi giá trị đồng. Tinh quặng đồng chủ yếu tác động tới an ninh nấu luyện trong nước, đồng tinh luyện ảnh hưởng trực tiếp đến sản xuất và hạ tầng điện năng, còn phế liệu đồng là nền tảng của hệ sinh thái đồng tái chế toàn cầu. Các biện pháp thắt chặt ở bất kỳ khâu nào cũng có thể lan truyền xuyên suốt chuỗi giá trị, và các trung tâm chế biến hạ nguồn khắp châu Á dự kiến sẽ gánh chịu phần điều chỉnh không cân xứng.

III. Kịch bản 3: Miễn trừ hoặc trì hoãn

Nếu Bộ Thương mại cuối cùng khuyến nghị miễn thuế nhập khẩu bổ sung đối với đồng tinh luyện, kỳ vọng thị trường vốn đã được phản ánh vào chênh lệch COMEX-LME nhiều khả năng sẽ thu hẹp trở lại. Nếu việc áp thuế chỉ bị trì hoãn, kỳ vọng về thuế sẽ vẫn tồn tại, kèm theo diễn biến chênh lệch giá đầy biến động. Trong cả hai trường hợp, động lực nhập khẩu trước hạn và kinh doanh chênh lệch liên thị trường được thúc đẩy bởi kỳ vọng thuế quan dự kiến sẽ giảm bớt. Phí bảo hiểm vật chất tại Mỹ có thể chịu sức ép, trong khi một phần hàng tồn kho tích lũy trong những tháng gần đây có thể quay lại các kênh tiêu thụ bình thường, làm tăng nguồn cung khả dụng trên thị trường giao ngay Mỹ. Tuy vậy, điều này sẽ không làm thay đổi triển vọng cơ cấu trung và dài hạn của đồng. Việc trì hoãn áp thuế chỉ trì hoãn quá trình tái cấu hình chuỗi cung ứng chứ không giải quyết được tình trạng thiếu hụt cơ cấu sản xuất đồng tinh luyện trong nước hay sự phụ thuộc dài hạn của Hoa Kỳ vào nguyên liệu nhập khẩu. Trong khi đó, nhu cầu từ sản xuất tiên tiến, điện khí hóa và hạ tầng AI dự kiến vẫn hỗ trợ. Đồng thời, sự tích hợp ngày càng tăng của thiếc, vonfram, tantalum và bạc vào chuỗi cung ứng phần cứng AI tiếp tục củng cố vai trò chiến lược của đồng như một "kim loại hạ tầng tính toán"

IV. Chênh lệch COMEX-LME: Thị trường đã định giá kỳ vọng thuế quan

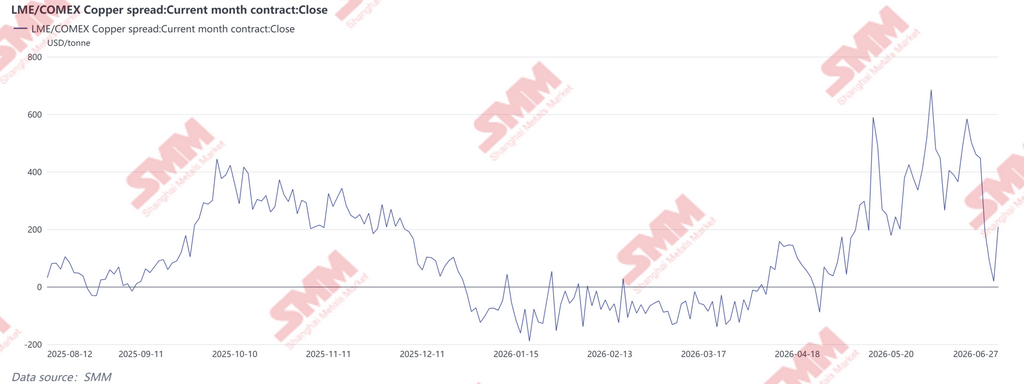

Kể từ tháng 4 năm 2026, chênh lệch đồng COMEX-LME đã nới rộng đáng kể, nhiều lần vượt mức 400 USD/tấn và chạm gần 690 USD/tấn vào đầu tháng 6, phản ánh hoạt động đặt cược quyết liệt trước thềm công bố tiềm năng về thuế đồng tinh luyện. Trong nửa cuối tháng 6, khi hàng kinh doanh chênh lệch dần cập cảng Hoa Kỳ và thị trường chuyển trọng tâm sang cột mốc chính sách ngày 30 tháng 6, mức chênh lệch thu hẹp mạnh – có lúc tiến sát ngang bằng – trước khi bật tăng trở lại quanh mức 200 USD/tấn, cho thấy giới đầu tư đã bước vào giai đoạn cuối của quá trình định vị dựa trên chính sách. Đáng chú ý, biến động của chênh lệch COMEX-LME không xuất phát từ thay đổi đáng kể nào trong các yếu tố cơ bản của đồng toàn cầu. Thay vào đó, nó phản ánh kỳ vọng xoay chiều xung quanh chính sách nhập khẩu của Hoa Kỳ và kết quả phân bổ lại đồng giữa các khu vực và tiến độ giao hàng.

Đầu năm nay, triển vọng về thuế đồng tinh luyện trong tương lai đã khuyến khích giới thương nhân đẩy nhanh giao hàng vào Mỹ, đẩy tồn kho COMEX tăng vọt, đồng thời duy trì mức phí bảo hiểm đáng kể so với giá LME và tạo ra cửa sổ chênh lệch giá rộng bất thường.

Khi đợt nhập khẩu trước hạn phần lớn đã hoàn tất, một phần chiết khấu thuế quan đã được phản ánh vào giá. Tuy nhiên, nếu Bộ Thương mại chính thức thông qua khuôn khổ thuế đồng tinh luyện theo giai đoạn vào ngày 30 tháng 6, chênh lệch COMEX-LME có thể nới rộng trở lại. Ngược lại, bất kỳ sự trì hoãn hay miễn trừ nào cũng có thể kích hoạt việc thu hẹp một phần các vị thế chênh lệch, làm tăng khả năng bình thường hóa cả phí bảo hiểm vật chất COMEX lẫn chênh lệch giá liên thị trường. Sau cùng, tầm quan trọng của cuộc điều tra theo Mục 232 vượt xa bản thân giá đồng. Vấn đề thực sự là khả năng định giá lại các luồng thương mại đồng toàn cầu, phí bảo hiểm vật chất theo khu vực và chênh lệch liên thị trường. Bất kể kết quả chính sách ra sao, việc củng cố sức chống chịu của chuỗi cung ứng đồng Hoa Kỳ vẫn sẽ là ưu tiên chiến lược.

![Nguồn cung châu Phi phân hóa: Nhập khẩu anode đồng của Trung Quốc trong tháng 6 phục hồi, bảo dưỡng quý 3 có thể gây áp lực lên nhập khẩu [Phân tích SMM]](https://imgqn.smm.cn/usercenter/Bwtty20251217171714.jpeg)

![Giá đồng tiếp tục tăng, các nhà cung cấp phế liệu đồng tích cực bán ra [Báo cáo hàng ngày đồng thứ cấp của SMM]](https://imgqn.smm.cn/usercenter/EFLYr20251217171714.jpeg)