I. Scenario One: Full Implementation of the Refined Copper Tariff

Should the U.S. Department of Commerce formally confirm the proposed tariff roadmap for refined copper on June 30, the market will be repricing U.S. copper supply rather than simply reacting to the tariff rate itself.

The current Section 232 measures primarily cover semi-fabricated copper products and copper-intensive derivative products. Refined copper cathodes, copper concentrates, copper anodes and copper scrap have so far remained outside the scope of the existing 50% tariff. The key issue is whether the Administration confirms the proposed phased tariff schedule of 15% in 2027 and 30% in 2028 on refined copper imports.

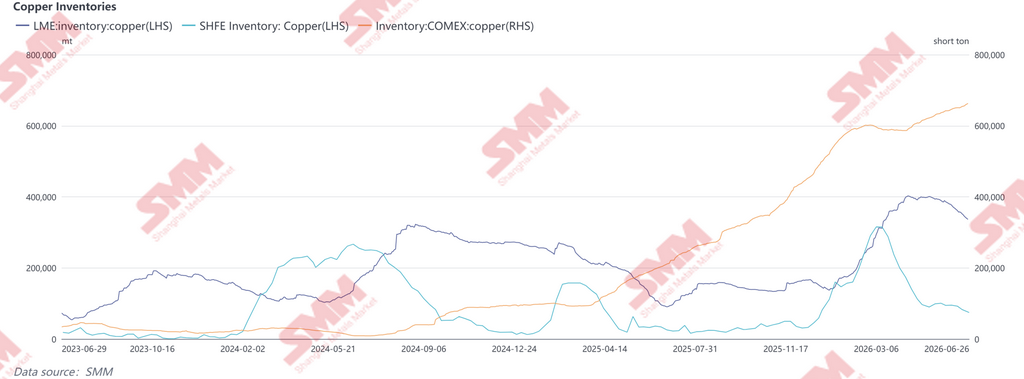

If implemented, the U.S. spot market would likely be the first to react. The substantial build-up of COMEX inventories over recent months has largely been driven by front-loaded imports and cross-market arbitrage ahead of potential tariff implementation. Following confirmation, these inventories are expected to serve as a short-term supply buffer, easing immediate tightness in the domestic market. Nevertheless, higher replacement costs for future imports are likely to support a structural premium for COMEX relative to LME.

Traditional refined copper shipments from Chile and Peru into the U.S. may also be affected. As tariffs erode import economics, part of these volumes could be redirected to Asia and Europe, increasing near-term availability outside the U.S. and placing relative pressure on LME and SHFE prices while widening regional market differentials.

Ultimately, the impact would extend beyond upstream trade flows into downstream manufacturing. Copper is no longer merely an industrial metal—it has become a strategic input for AI infrastructure, electrification and advanced manufacturing.

II. Scenario Two: Targeted or Phased Tariffs

If Washington opts against imposing a blanket tariff on refined copper and instead adopts targeted measures based on HTS classifications, country of origin, purity or product form, the resulting market impact may be less visible but significantly more disruptive to global supply chains.

The first area of risk lies in copper scrap. Should the U.S. tighten export restrictions on high-grade scrap, or impose quotas, tariffs or stricter origin verification on transshipped material, global secondary copper flows would likely undergo significant restructuring. High-quality U.S. scrap has long been an important feedstock for China's and Southeast Asia's recycled copper industries. Any restriction on exports would compress processing margins in Malaysia, Thailand and Vietnam while tightening recycled copper feedstock availability in China.

The second risk concerns origin arbitrage. If USMCA members receive preferential treatment or exemptions, Mexico and Canada could emerge as regional redistribution hubs for refined copper. Traders may increasingly reroute shipments through these markets to optimize tariff exposure, making rules of origin, substantial transformation requirements and HTS classifications more important than the headline tariff rate itself.

The third implication is the increasing segmentation of the copper value chain. Copper concentrates primarily affect domestic smelting security, refined copper directly impacts manufacturing and power infrastructure, while copper scrap underpins the global recycled copper ecosystem. Tightening measures at any stage would likely transmit through the value chain, with downstream processing hubs across Asia expected to bear a disproportionate share of the adjustment.

III. Scenario Three: Exemption or Postponement

Should the Department ultimately recommend exempting refined copper from additional import tariffs, market expectations priced into the COMEX-LME spread are likely to unwind. If implementation is merely postponed, tariff expectations would remain in place, with the spread likely to remain volatile. In either case, the front-loading of imports and cross-market arbitrage driven by tariff expectations is likely to moderate. U.S. physical premiums may come under pressure, while part of the inventories accumulated in recent months could gradually return to normal consumption channels, increasing available supply in the U.S. spot market. However, this would not alter copper's medium- to long-term structural outlook. A delay in tariff implementation would merely postpone supply chain reconfiguration rather than resolve the structural shortage of domestic refined copper production or the U.S.'s long-term reliance on imported material. Meanwhile, demand from advanced manufacturing, electrification and AI infrastructure is expected to remain supportive. At the same time, the growing integration of tin, tungsten, tantalum and silver into AI hardware supply chains continues to reinforce copper's strategic role as a "computing infrastructure metal."

IV. COMEX-LME Spread: The Market Has Already Priced in Tariff Expectations

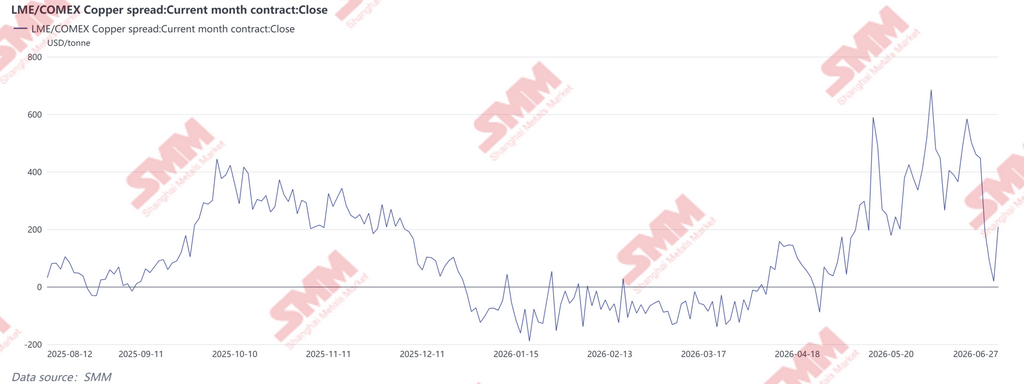

Since April 2026, the COMEX-LME copper spread has widened significantly, repeatedly exceeding US$400/t and reaching nearly US$690/t in early June, reflecting aggressive positioning ahead of a potential refined copper tariff announcement. During the second half of June, as arbitrage cargoes gradually arrived in the United States and the market shifted its focus toward the June 30 policy milestone, the spread narrowed sharply—briefly approaching parity—before rebounding to around US$200/t, suggesting that investors have entered the final phase of policy-driven positioning. Importantly, the volatility in the COMEX-LME spread has not been driven by a material change in global copper fundamentals. Instead, it reflects shifting expectations surrounding U.S. import policy and the resulting reallocation of copper across regions and delivery timelines.

Earlier this year, expectations of future tariffs on refined copper encouraged traders to accelerate shipments into the U.S., driving COMEX inventories sharply higher while sustaining a significant premium over LME prices and creating an unusually wide arbitrage window.

As inventory front-loading has largely run its course, part of the tariff premium has already been priced in. Nevertheless, should the Department formally endorse the phased refined copper tariff framework on June 30, the COMEX-LME spread could widen again. Conversely, any postponement or exemption may trigger a partial unwinding of existing arbitrage positions, increasing the likelihood of normalization in both COMEX physical premiums and cross-market price differentials. Ultimately, the significance of the Section 232 investigation extends beyond copper prices themselves. The real issue is the potential repricing of global copper trade flows, regional physical premiums and cross-market spreads. Regardless of the policy outcome, strengthening the resilience of the U.S. copper supply chain will remain a strategic priority.

![This week, China’s copper social inventory re-entered an inventory buildup trend [SMM weekly data]](https://imgqn.smm.cn/usercenter/CaLPF20251217171713.jpg)