วันที่ 26 มิถุนายน ในการประชุม SMM (ครั้งที่ 14) อุตสาหกรรมโลหะหายาก—ฟอรั่มพลวง ซึ่งจัดโดย SMM Information & Technology Co., Ltd. (SMM) และได้รับการสนับสนุนหลักจาก Guangxi Yusheng Germanium High-tech Co., Ltd., , หลัว เฉิงไฉ ผู้จัดการทั่วไปของ Hunan Hsikwangshan Twinkling Star Antimony Import & Export Co., Ltd. ได้แบ่งปัน “เส้นทางการเปลี่ยนแปลงและพัฒนาของอุตสาหกรรมพลวงท่ามกลางการเปลี่ยนแปลงแห่งศตวรรษ” แก่ผู้เข้าร่วมประชุม

I. การพลิกโฉมภูมิทัศน์อุตสาหกรรมพลวงท่ามกลางการเปลี่ยนแปลงแห่งศตวรรษ

ขับเคลื่อนโดยนโยบาย: การควบคุมการส่งออกทำให้เกิดการแยกตัวของตลาดอย่างลึกซึ้ง

►ตลาดนอกจีน: การขยายกำลังการผลิตอย่างรวดเร็วขับเคลื่อนด้วยราคาสูง

อุปทานจากเหมืองเพิ่มขึ้นอย่างรวดเร็ว: เหมืองซานตาร์ในเมียนมาร์กลายเป็นตัวแปรสำคัญ โดยมีผลผลิตรายเดือนถึง 1,000 เมตริกตันของเนื้อโลหะ และความยืดหยุ่นของอุปทานยังแข็งแกร่ง

การวางกำลังการหลอมเร่งตัวขึ้น: ประเทศในเอเชียตะวันออกเฉียงใต้ เช่น ไทย เมียนมาร์ และเวียดนาม กำลังเพิ่มกำลังการหลอมอย่างรวดเร็ว โดยกำลังการผลิตรวมนอกจีนแตะระดับประมาณ 40,000 เมตริกตัน/ปีแล้ว

ขับเคลื่อนโดยนโยบาย: ความไม่สมดุลระหว่างอุปสงค์และอุปทานในตลาดจีน

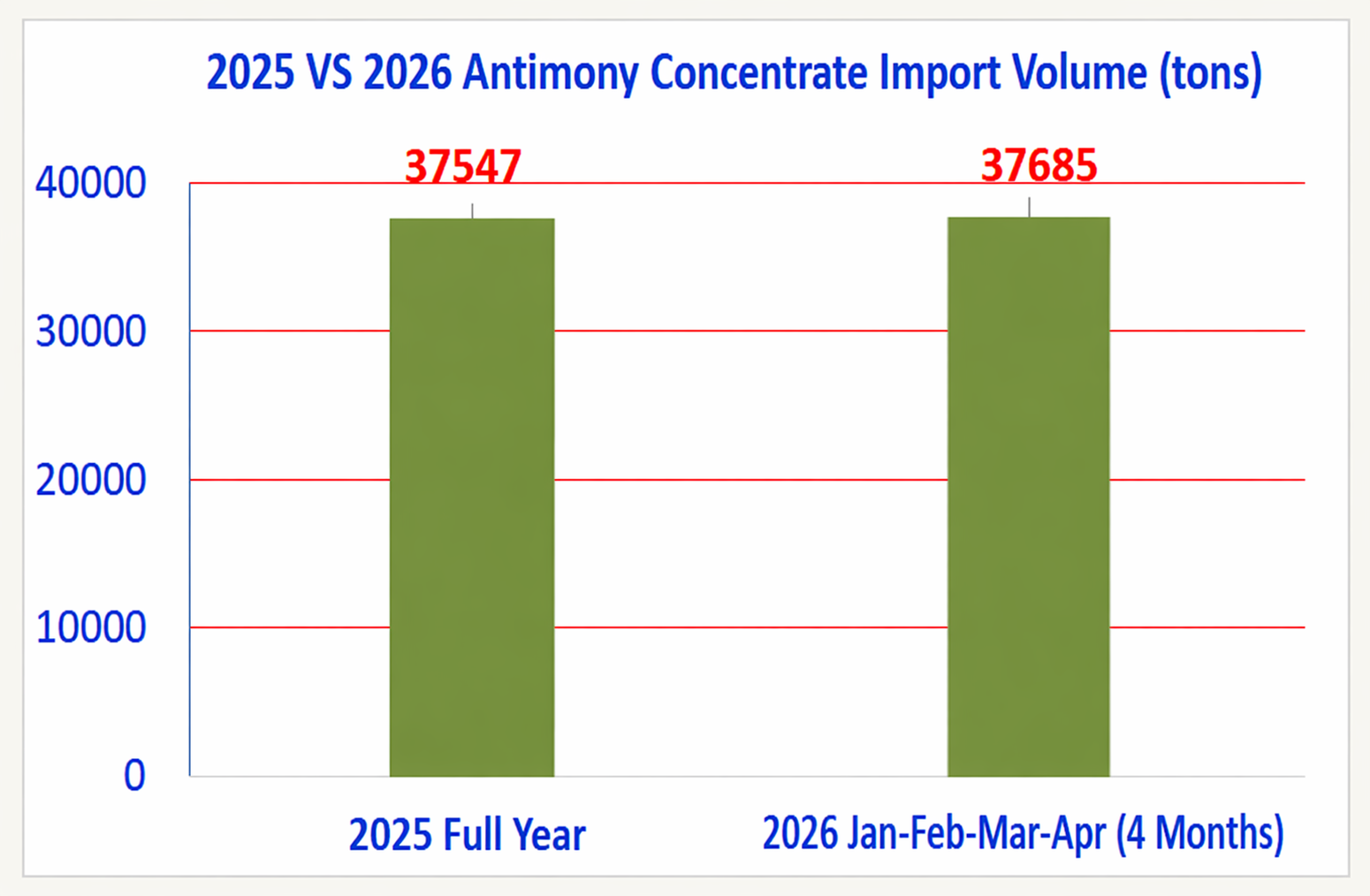

ด้านอุปทานหลวมอย่างมาก: ในปี 2026 เพียงแค่สี่เดือนแรก การนำเข้าก็เทียบเท่ากับตลอดทั้งปี 2025 แล้ว สร้างแรงกดดันด้านอุปทานต่อตลาดอย่างที่ไม่เคยปรากฏมาก่อน

ด้านอุปสงค์มีการแข่งขันสูง: ราคาลดลงอย่างรุนแรง

ผลกระทบทางภูมิรัฐศาสตร์: สงครามในตะวันออกกลางได้สร้างความเสียหายที่ไม่อาจฟื้นคืนได้

►อุตสาหกรรมสารหน่วงไฟ: ความเจ็บปวดระยะสั้น

ราคาโบรมีนพุ่งขึ้นจาก 30,000 เป็น 130,000 ต่อเมตริกตัน ราคาวัตถุดิบปิโตรเคมีพุ่งขึ้นกว่า 50% และการส่งผ่านต้นทุนได้ไม่ดีทำให้เกิดภาวะขาดทุนในวงกว้าง โดยมีการลดกำลังการผลิตประมาณ 30%

►อุตสาหกรรมโพลีเอสเตอร์: เผชิญแรงกดดันจากทั้งต้นทุนและการผลิต

ได้รับผลกระทบจากความผันผวนของราคาวัตถุดิบปิโตรเคมีต้นน้ำ ทำให้ต้นทุนการผลิตของอุตสาหกรรมเพิ่มขึ้นอย่างรวดเร็ว ประกอบกับอุปสงค์ปลายทางที่อ่อนตัว ทำให้ถูกบีบให้ลดกำลังการผลิตประมาณ 30% ส่งผลให้แรงกดดันในการดำเนินงานเพิ่มขึ้นอย่างรุนแรง

►กระจกสำหรับโซลาร์เซลล์: ชะลอตัวระยะสั้นแต่แนวโน้มระยะยาวยังเป็นบวก

ได้รับผลกระทบจากการยกเลิกการคืนภาษีส่งออกสำหรับโมดูลและความไม่แน่นอนในตลาดอินเดีย ทำให้อุปสงค์ระยะสั้นอ่อนแอลง อย่างไรก็ตาม แนวโน้มการเปลี่ยนผ่านพลังงานของโลกยังคงไม่เปลี่ยนแปลง และศักยภาพการเติบโตระยะยาวยังมีอยู่

II. โอกาสท่ามกลางวิกฤต: โอกาสใหม่สำหรับการเปลี่ยนแปลงและการพัฒนา

ปัจจัยพื้นฐานที่แข็งแกร่ง: การรวมตัวและการเพิ่มประสิทธิภาพในภาคส่วนดั้งเดิม

►วัสดุหน่วงไฟประสิทธิภาพสูง

ความไม่สามารถทดแทนได้: ยังไม่สามารถทดแทนได้อย่างมีประสิทธิภาพในพลาสติกวิศวกรรม เช่น ABS และ XPS

การเติบโตของตลาด: ความต้องการสารหน่วงไฟประจำปีของจีนสูงถึง 1.5 ล้านเมตริกตัน โดยสารหน่วงไฟชนิดโบรมีน-แอนติโมนีมีสัดส่วน 35% และความต้องการเพิ่มขึ้นอย่างต่อเนื่อง

►อุตสาหกรรมโพลีเอสเตอร์

ตัวเร่งปฏิกิริยาหลัก: หน่วยผลิตโพลีเอสเตอร์มากกว่า 90% ใช้ตัวเร่งปฏิกิริยาที่มีส่วนผสมของแอนติโมนี ทำให้มีสถานะที่มั่นคง

พื้นที่การเติบโตใหม่: สิ่งทออุตสาหกรรมเติบโตอย่างรวดเร็วในภาคส่วนต่างๆ เช่น การแพทย์และพลังงานใหม่ โดยมีอัตราการเติบโตเฉลี่ยต่อปีเกิน 10%

►กระจก PV

สารหลอมหลัก: ครองส่วนแบ่งตลาดมากกว่า 80% ให้ประสิทธิภาพสูงด้วยต้นทุนที่ควบคุมได้

แรงขับเคลื่อนที่แข็งแกร่งนอกประเทศจีน: ด้วยแรงขับเคลื่อนจากการเปลี่ยนผ่านพลังงานระดับโลก ความต้องการในตลาดนอกประเทศจีนยังคงแข็งแกร่ง โดยประเทศต่างๆ เช่น อินเดียและอินโดนีเซียกำลังก่อสร้างโรงงานขนาดใหญ่

สรุป: โครงสร้างอุปสงค์ที่มั่นคงในสามภาคส่วนหลักดั้งเดิม ได้แก่ สารหน่วงไฟ โพลีเอสเตอร์ และ PV ประกอบกับการขยายตัวอย่างต่อเนื่องของตลาดเกิดใหม่นอกประเทศจีน ก่อให้เกิดรากฐานที่มั่นคงและเชื่อถือได้สำหรับอุตสาหกรรมแอนติโมนี

แรงขับเคลื่อนการเติบโตใหม่: แบตเตอรี่สสารควบแน่น กลไกการเติบโตที่ยิ่งใหญ่ที่สุดในอนาคต

►เส้นทางเทคนิค: องค์กรอย่าง CATL กำลังวางแผนแบตเตอรี่โซเดียมไอออนที่ใช้แอนติโมนี โดยส่วนของรถยนต์นั่งจะใช้วัสดุคอมโพสิตแคลเซียม-แอนติโมนีเป็นขั้วลบ

►ประมาณการอุปสงค์: CATL วางแผนกำลังการผลิต 60 กิกะวัตต์-ชั่วโมง โดย 24 กิกะวัตต์-ชั่วโมงจัดสรรให้กับรถยนต์นั่ง หากคำนวณที่การใช้แอนติโมนี 1,200 เมตริกตันต่อกิกะวัตต์-ชั่วโมง อุปสงค์ต่อปีอาจสูงถึง 30,000 เมตริกตันเมื่อผลิตเต็มกำลัง นี่คือตลาดที่มีศักยภาพมหาศาล

แรงขับเคลื่อนการเติบโตใหม่: การเติบโตอย่างรวดเร็วในการใช้งานที่มีมูลค่าสูง

►พลังประมวลผล AI: การเติบโตแบบก้าวกระโดดของเซิร์ฟเวอร์ AI และศูนย์ข้อมูล ทำให้ปริมาณการใช้แอนติโมนีในภาคเซมิคอนดักเตอร์สูงกว่า 2,000 เมตริกตัน

►ภาคการทหาร: พลวงความบริสุทธิ์สูงเป็นวัสดุสำคัญสำหรับการตรวจจับอินฟราเรดและการนำวิถีขีปนาวุธ มีราคาพรีเมียมสูงกว่า 3 ถึง 5 เท่า ในบริบทของความขัดแย้งทางภูมิรัฐศาสตร์ คำสั่งซื้อที่เกี่ยวข้องกับการทหารพุ่งขึ้น 80% เมื่อเทียบเป็นรายปี

►แบตเตอรี่ตะกั่ว-กรด: ใช้เป็นโลหะผสมตะกั่ว-พลวงในกริดขั้วบวก พลวงช่วยเพิ่มประสิทธิภาพของแบตเตอรี่อย่างมาก การบริโภคพลวงของจีนในส่วนนี้อยู่ที่ประมาณ 13,000–15,000 ตัน ในขณะที่การบริโภคทั่วโลกอยู่ที่ประมาณ 22,000 ตัน ซึ่งเป็นรากฐานที่มั่นคง

III. การปรับเป็นมูลค่าปกติ: แนวโน้มในอนาคตและมุมมองเชิงกลยุทธ์

ด้านอุปทาน: ข้อจำกัดด้านทรัพยากรและการควบคุมนโยบายกลายเป็นภาวะปกติใหม่

►ทรัพยากรที่ไม่สามารถหมุนเวียนได้และอุปทานที่ตึงตัวเป็นแนวโน้มระยะยาว

ปริมาณสำรองในประเทศของจีนกำลังหมดลงและคุณภาพแร่ลดลง โดยผลผลิตลดลงทุกปี

อุปทานเพิ่มเติมจากนอกประเทศจีนมีจำกัดและไม่เสถียร

►การจำกัดการผลิตในประเทศและการรวมทรัพยากรเป็นแนวโน้มที่สำคัญ

อัตราส่วนปริมาณสำรองคงเหลือต่อการผลิตทั่วโลกของพลวงน้อยกว่า 10 ปี ซึ่งเน้นย้ำถึงมูลค่าเชิงกลยุทธ์

การเสริมการปกป้องสิ่งแวดล้อม การใช้ข้อจำกัดการผลิต และการส่งเสริมการรวมทรัพยากรเป็นเส้นทางที่หลีกเลี่ยงไม่ได้สำหรับประเทศ

กลไกตลาด: ก้าวสู่เสถียรภาพและการอยู่ร่วมกันอย่างกลมกลืน

ข้อสรุปและมุมมอง

• อุตสาหกรรมพลวงยืนอยู่ ณ จุดเริ่มต้นประวัติศาสตร์ใหม่ ความผันผวนของตลาดระยะสั้นและความเจ็บปวดด้านราคาเป็น "การรักษาที่รุนแรง" ที่จำเป็นในระหว่างกระบวนการปรับโครงสร้างอุตสาหกรรม

• เราเชื่อมั่นว่าเมื่ออุปทานตึงตัวขึ้น การระเบิดของอุปสงค์ใหม่ และการเน้นย้ำเชิงกลยุทธ์ในระดับประเทศ มูลค่าเชิงกลยุทธ์ของพลวงจะถูกตระหนักอย่างเต็มที่และจะกลับคืนสู่มูลค่าที่แท้จริงในที่สุด ท่ามกลางการต่อสู้ระหว่างผู้ขายและผู้ซื้อ

• ให้เราจับมือกันและร่วมมือกันขับเคลื่อนอุตสาหกรรมพลวงเข้าสู่ยุคใหม่ของการพัฒนาที่มั่นคง สมดุล และมีคุณภาพสูง อุตสาหกรรมพลวงจะมีอนาคตที่สดใสอย่างแน่นอน!

![ข้อมูล SMM ระบุว่า ผลผลิตแท่งพลวงของจีนที่ประเมินโดย SMM เพิ่มขึ้นประมาณ 30% เมื่อเทียบรายเดือนในเดือนกรกฎาคม 2026 [ข้อมูล SMM]](https://imgqn.smm.cn/usercenter/qbMSp20251217171722.jpeg)