June 26, at the 2026 SMM (14th) Minor Metal Industry Conference—Antimony Industry Forum, hosted by SMM Information & Technology Co., Ltd. (SMM) and with title sponsorship from Guangxi Yusheng Germanium High-tech Co., Ltd., , Luo Chengcai, General Manager of Hunan Hsikwangshan Twinkling Star Antimony Import & Export Co., Ltd., shared with participants the “Path of Transformation and Development for the Antimony Industry Amid Century-Long Changes.”

I. Reshaping the Antimony Industry Landscape Amid Century-Long Changes

Policy-driven: Export Controls Trigger Profound Market Fragmentation

►Markets outside China: Rapid Capacity Expansion Driven by High Prices

Mine supply growing rapidly: The Santar mine in Myanmar has become a key variable, with monthly production reaching 1,000 mt of metal content and strong supply resilience.

Smelting capacity deployment accelerates: Southeast Asian countries such as Thailand, Myanmar, and Vietnam are rapidly boosting smelting capacity, with total ex-China capacity already reaching about 40,000 mt/year.

Policy-driven: Supply-demand imbalance in the Chinese market

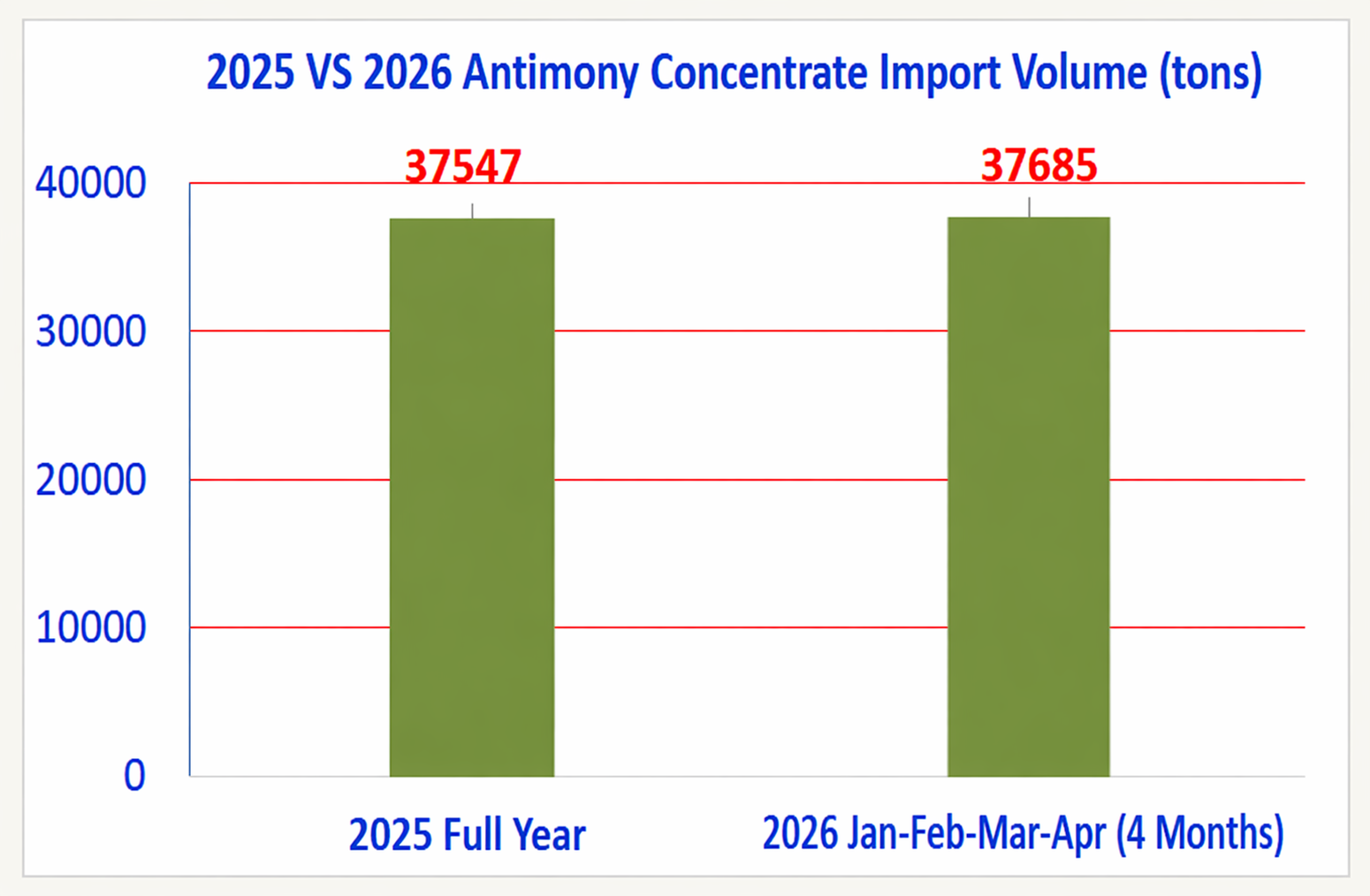

Supply side extremely loose: In 2026, imports in the first four months alone have already matched the total for the full year 2025, creating unprecedented supply pressure on the market.

Demand side highly competitive: Prices have fallen sharply.

Geopolitical shocks: The Middle East war has caused irreversible damage

►Flame retardant industry: Short-term pain

Bromine prices surged from 30,000 to 130,000/mt, petrochemical raw material prices jumped over 50%, and poor cost pass-through led to widespread industry losses, with production cuts of around 30%.

►Polyester industry: Under pressure from both costs and production

Affected by wild swings in upstream petrochemical raw material prices, the industry's production costs have climbed sharply; with weak end-use demand, it was forced to cut production by about 30%, sharply increasing operating pressure.

►PV glass: Short-term cooling but long-term positive outlook

Affected by the cancellation of module export tax rebates and uncertainties in the Indian market, short-term demand has weakened; however, the broader trend of global energy transition remains unchanged, and long-term growth potential persists.

II. Opportunities Amid Crisis: New Opportunities for Transformation and Development

Solid fundamentals: Consolidation and optimization in traditional sectors

►High-performance flame retardant materials

Irreplaceability: Still cannot be effectively replaced in engineering plastics such as ABS and XPS.

Market growth: China's annual demand for flame retardants reaches 1.5 million mt, with bromine-antimony flame retardants accounting for 35%, and demand is steadily increasing.

►Polyester industry

Core catalyst: Over 90% of polyester units use antimony-based catalysts, securing a solid position.

New growth areas: Industrial textiles are growing rapidly in sectors such as medical and new energy, with an average annual growth rate exceeding 10%.

►PV Glass

Core Refining Agent: Holding over 80% market share, it delivers high efficiency with controllable costs.

Strong Momentum Outside China: Driven by the global energy transition, demand in markets outside China remains robust, with countries such as India and Indonesia building plants on a large scale.

Summary: The steady demand structure across the three traditional pillar sectors—flame retardants, polyester, and PV—combined with the continued expansion of emerging markets outside China, forms a solid and reliable foundation for the antimony industry.

New Growth Driver: Condensed Matter Batteries, the biggest growth engine going forward

►Technical Pathway: Enterprises such as CATL are planning antimony-based sodium-ion batteries, in which the passenger vehicle segment will use a calcium-antimony composite material as the negative electrode.

►Demand Estimate: CATL has planned 60 GWh of capacity, with 24 GWh allocated to passenger vehicles. Calculated at 1,200 mt of antimony per GWh, annual demand could reach as much as 30,000 mt at full production. This represents a massive potential market.

New Growth Driver: Rapid Growth in High-Value Applications

►AI Computing Power: The explosive growth of AI servers and data centers has driven antimony consumption in the semiconductor sector to over 2,000 mt.

►Military Sector: High-purity antimony is a critical material for infrared detection and missile guidance, commanding a price premium of 3 to 5 times. Against a backdrop of geopolitical conflicts, military-related orders surged 80% YoY.

►Lead-Acid Batteries: Used as a lead-antimony alloy in positive electrode grids, antimony significantly enhances battery performance. China's antimony consumption in this segment stands at approximately 13,000–15,000 mt, with global consumption at around 22,000 mt, providing a stable foundation.

III. Value Normalization: Future Trends and Strategic Outlook

Supply Side: Resource Constraints and Policy Regulation Become the New Normal

►Non-renewable resources and a tight supply are long-term trends

China's domestic reserves are depleting and grades are declining, with production falling year by year.

Incremental supply from outside China is limited and unstable.

►Domestic production restrictions and resource consolidation are the overriding trends

The global static reserve-to-production ratio for antimony is less than 10 years, highlighting its strategic value.

Strengthening environmental protection, implementing production restrictions, and promoting resource consolidation are the inevitable path for the nation.

Market Mechanisms: Moving Toward Stability and Harmonious Coexistence

Conclusions and Outlook

• The antimony industry stands at a new historical starting point. Short-term market fluctuations and price pains are the necessary "drastic remedies" during the process of industrial restructuring.

• We firmly believe that with the tightening of the supply side, the explosion of emerging demand, and the strategic emphasis at the national level, antimony's strategic value will be fully realized and will eventually return to its intrinsic worth in the tug-of-war between sellers and buyers.

• Let us join hands and work together to propel the antimony industry toward a new era of stable, balanced, and high-quality development. The antimony industry is bound to have a bright future!