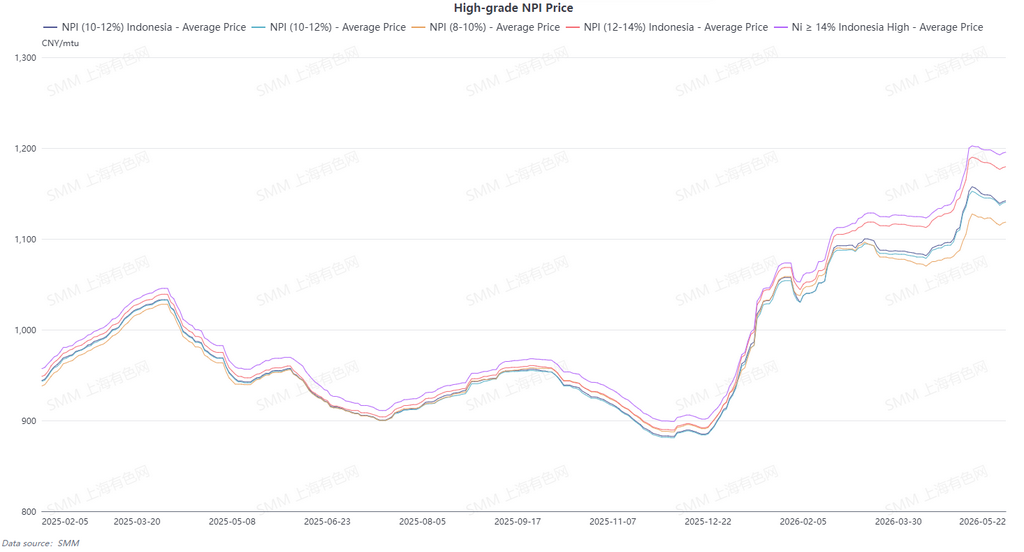

The SMM 10-12% high-grade NPI average price rose WoW by 0.87 yuan/nickel unit to 1,147 yuan/nickel unit (ex-factory, tax included), while the Indonesian NPI FOB index average price fell WoW by $0.06/nickel unit to $147/nickel unit. This week, the high-grade NPI market overall was in the doldrums. Futures continued to weaken, dragging down market sentiment, while the resilience of spot prices to hold firm gradually faded. A tug-of-war between longs and shorts was intense, and the price spread between bids and asks widened, resulting in extremely sluggish overall trading.

At the start of the week, spot prices showed resistance to declines, supported by tight supply, with noticeable divergence from futures. However, bearish factors were released en masse during the week, weakening the support from the tight spot supply logic. The price center slowly moved downward. Downstream, the desire to bargain down prices was strong, and mainstream steel mills' purchasing intentions declined, leaving the supply-demand price spread difficult to narrow for an extended period. Supply side, suppliers overall held prices firm with weak willingness to sell at low prices, and high costs limited the room for deep spot price declines. But the sharp drop in futures fueled a wait-and-see sentiment, with some traders suspending quotations, and market liquidity continued to decline. Demand side, the core bearish factor this week was the larger-than-expected decline in refined nickel and the rising cost-effectiveness of steel scrap, creating a dual substitution effect that significantly diverted rigid NPI demand. Combined with a weakening stainless steel market and pressured steel mill profits, mills had maintenance plans from June to July. Raw material restocking demand remained sluggish, with only sporadic small orders concluded. At the same time, expectations for long-term supply increments from the liberalization of nickel ore quotas continued to ferment, spreading bearish sentiment. Overall, the weak logic for NPI has not reached a turning point. In the short term, the market will continue to consolidate in the doldrums, characterized by a stalemate with no actual transactions. The price center has room to move downward. Market recovery requires futures to stabilize, downstream restocking to begin, or the advantages of substitute raw materials to subside.

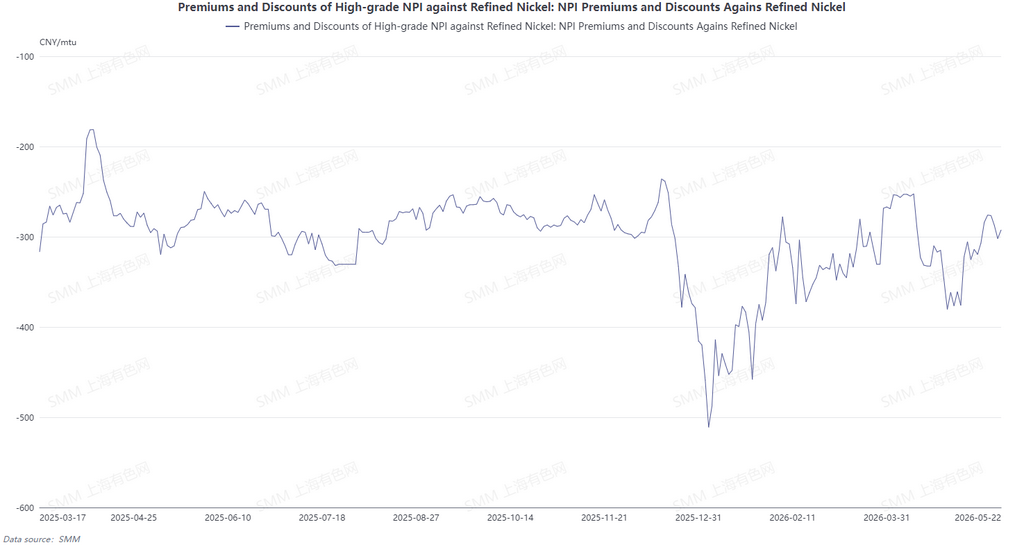

From the perspective of conversion of NPI to high-grade nickel matte, the discount of high-grade NPI relative to refined nickel has continued to narrow recently. Macro side, rising expectations for US Fed interest rate hikes pushed up the US dollar, and rumors of eased Indonesian nickel ore mining quotas brought expectations of long-term nickel ore supply increments. These dual bearish factors continued to pressure refined nickel prices, with futures falling significantly. In contrast, high-grade NPI was supported by tight domestic spot supply, with suppliers holding back from selling and holding prices firm. Spot price declines were notably slower than those of refined nickel, causing the price difference to keep shrinking. The average discount of high-grade NPI to refined nickel narrowed to 164.7 yuan/nickel unit. It is expected that next week, bearish factors at the macro and supply levels will not quickly dissipate. The fundamentals of tight spot supply for high-grade NPI show no improvement, and refined nickel lacks strong drivers for a rebound. The price spread is unlikely to widen again significantly, and there is no driving force for the conversion of high-grade NPI to high-grade nickel matte.

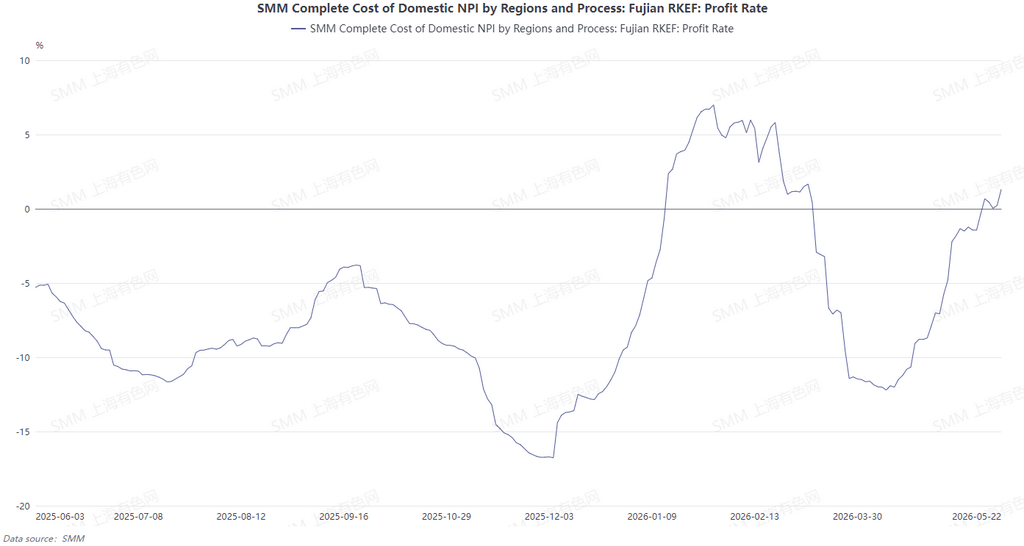

This week, NPI production costs in and outside China continued to diverge. In China, Philippines nickel ore prices edged down MoM, and with coal prices staying stable, cost advantages on the ore side were further consolidated, allowing domestic smelters to maintain profitability. In Indonesia, nickel ore prices edged down slightly, and local plants also increased their purchase ratio of Philippine nickel ore, further lowering ore procurement expenses. However, Indonesia faced upward cost pressure from two fronts: rising coal and electricity prices eroded the cost benefit from cheaper ore, as these were offset by increases in energy and auxiliary material costs. As a result, overall production cost pressure remained difficult to ease, and corporate profit margins stayed limited.

![[SMM Flash News] Canada Nickel Appoints SB1 Markets to Arrange Up to US$600M Debt Financing for Crawford Project](https://imgqn.smm.cn/usercenter/PFIti20251217171734.jpg)

![[SMM Flash News] Swelect Energy Acquires 49% Stake in Gridnex Solar Power to Expand Indian PV Portfolio](https://imgqn.smm.cn/usercenter/WYeHX20251217171733.jpg)

![[SMM Analysis] Nickel Salt Prices Show Weakness, Intermediate Product Coefficient Under Pressure in the Short Term](https://imgqn.smm.cn/usercenter/JjbtE20251217171732.jpeg)