SMM June 27 news:

Metal market:

Overnight, domestic base metals almost all rose. SHFE zinc rose 2.16%, SHFE copper rose 0.9%, SHFE aluminum rose 0.81%, and SHFE tin rose 1.66%. SHFE nickel rose 0.36%. SHFE lead fell 0.37%. In addition, the most-traded alumina futures rose 0.64%, and the most-traded cast aluminum continuous contract rose 1.66%.

Overnight, ferrous metals mostly rose. Stainless steel rose 0.48%, iron ore rose 0.54%, and rebar fell 0.1%. HRC was flat at 3,312 yuan/mt. Coking coal and coke side: the most-traded coking coal contract rose 1.13%, and the most-traded coke contract rose 1.21%.

Overnight, in the overseas metal market, LME base metals generally rose. LME copper edged up. LME aluminum rose 0.39%, LME lead fell 0.58%. LME zinc rose 1.8%. LME tin rose 1.69%. LME nickel fell 0.36%.

Overnight precious metals: COMEX gold rose 1.37%, but posted a four-week losing streak on the weekly chart, down 3.37% for the week; COMEX silver rose 1.37%, but has fallen for seven consecutive weeks, down 10.79% for the week. Overnight, the most-traded SHFE gold continuous contract rose 1.34%, with SHFE gold posting a weekly decline, down 6.33% for the week; the most-traded SHFE silver continuous contract rose 2.61%, with SHFE silver posting a weekly decline, down 15.23% for the week.

Macquarie strategists noted that all eyes are currently on the path of inflation and whether central banks, especially the US Federal Reserve, will tighten policies to control prices. The apparent end of the Middle East conflict, coupled with a more hawkish US Fed stance, led to a pullback in gold prices. The first meeting of new US Fed Chair Walsh had a 'hawkish' tone, and under his leadership, the central bank has the ability to 'drive or suppress' gold market prices. The shock from the Middle East situation is expected to drag on global growth in Q3, after which the eventual recovery in global growth and the start of a monetary easing cycle should drive gold prices lower, as more investor funds shift from precious metals to other assets. Investors have been taking profits and shifting to equities, creating space for them to re-enter the precious metals sector and drive a price rebound, though this may require a major macro event to reignite investor interest in gold. The forecast is for spot gold to average $4,641 in 2026, up 35% YoY, but to decline 9.5% to $4,200 in 2027, and then fall year by year through 2030. The bank lowered its year-end spot gold forecast from $4,400 to $4,300. (Jinshi Data APP)

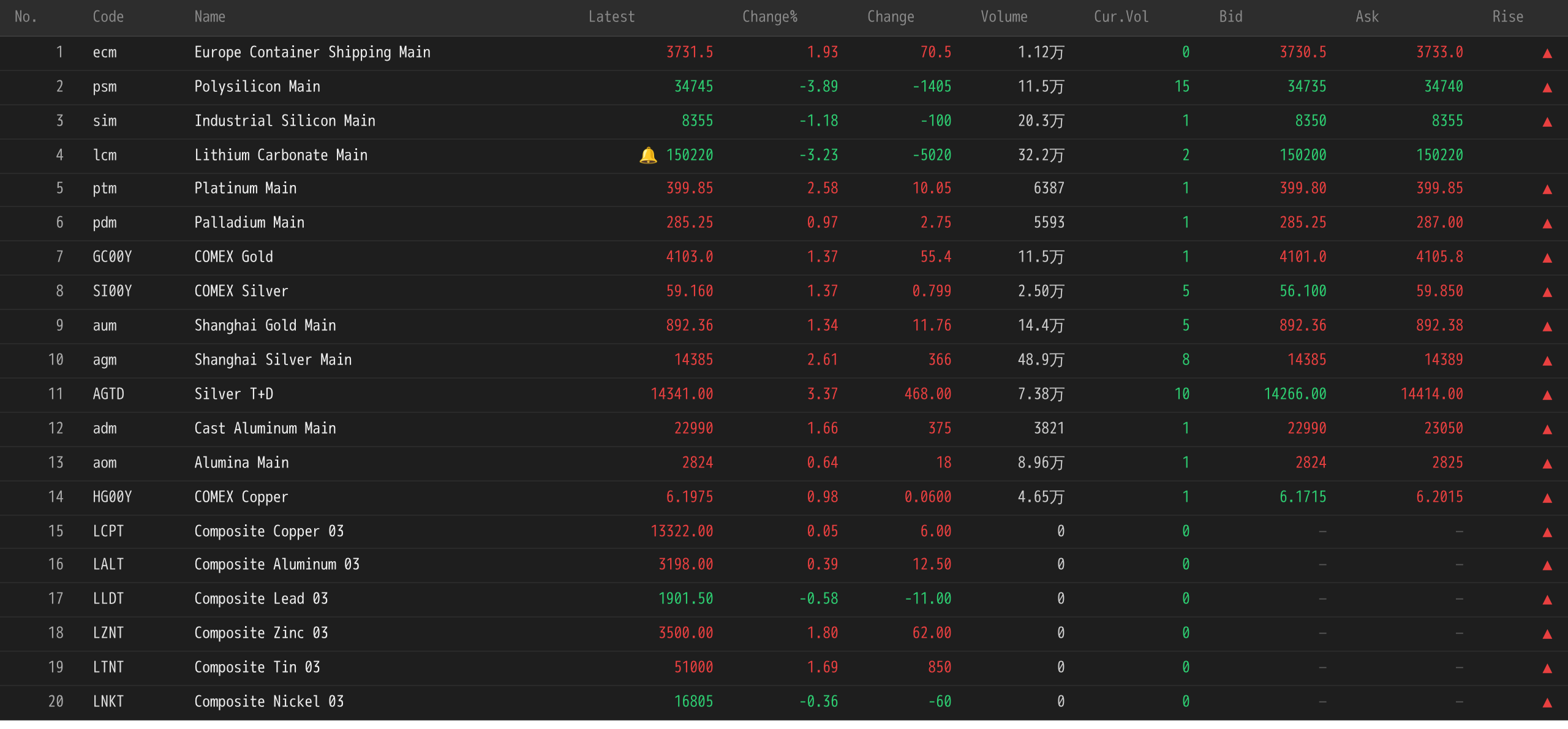

As of 7:46 on June 27, the closing prices for the overnight session:

Macro front

China:

[National Bureau of Statistics (NBS): Profits of China's industrial enterprises above designated size grew 18.8% in January-May, with the electronics industry providing significant support] Data from the National Bureau of Statistics showed that in January-May, the total profits of China's industrial enterprises above designated size reached 3,143.96 billion yuan, up 18.8% YoY. From January to May, among industrial enterprises above designated size, state-controlled enterprises realized total profits of 1,048.66 billion yuan, up 19.6% YoY; joint-stock enterprises realized total profits of 2,434.81 billion yuan, up 24.1% YoY; foreign-invested enterprises and those funded by Hong Kong, Macao, and Taiwan investors realized total profits of 695.72 billion yuan, up 4.2% YoY; and private enterprises realized total profits of 772.65 billion yuan, up 10.7% YoY. Yu Weining, chief statistician of the Industrial Department of the National Bureau of Statistics (NBS), interpreted the profit data of industrial enterprises for January–May 2026. Yu Weining noted that the electronics sector played a significant supporting role. From January to May, profits of the equipment manufacturing industry above designated size increased by 14.1% YoY, boosting the overall profit growth of industrial enterprises above designated size by 5.2 percentage points. From an industry perspective, the global AI technology revolution has led to explosive demand for high-end computing power chips and memory chips, driving rapid profit growth in the electronics sector. From January to May, profits of the electronics industry surged 103.9% YoY, contributing 43.1% to the profit growth of all industrial enterprises above designated size, making it a crucial underpinning for the relatively rapid profit growth of these enterprises.

[Series of 7 National Standards for "Artificial Intelligence — Agent Interconnection" Released] At a press conference held by the State Administration for Market Regulation (SAMR), it was announced that the series of national standards "Artificial Intelligence — Agent Interconnection" has been officially released. With the rapid iteration of technologies such as large models, artificial intelligence is accelerating from the stage of perception and understanding into a new phase of generative decision-making and autonomous execution. An agent, as an intelligent system with capabilities in autonomous perception, memory, decision-making, interaction, and execution, represents an important application form of next-generation AI. It is also a key vehicle for AI technology to empower diverse industries and underpin high-quality development of the intelligent economy. The seven national standards in the "Artificial Intelligence — Agent Interconnection" series released this time comprehensively cover core aspects including overall architecture, identity codes, identity management, agent description, agent discovery, agent interaction, and agent tool invocation. They systematically establish a closed-loop standards framework encompassing "identity identification—capability description—supply-demand discovery—collaborative interaction—tool invocation," effectively filling the standard gap in this field. With unified architecture and interaction rules established through these standards, enterprises can reuse standardized components, reduce customized development, and shorten time-to-market. At the same time, they lay an institutional foundation for cross-domain trustworthiness and secure interaction by establishing unified identity authentication and full traceability mechanisms. (CCTV News)

The People's Bank of China and the General Administration of Customs have issued a notice to solicit public opinions on the "Administrative Measures for the Import and Export of Gold and Gold Products (Draft for Comments)."(From Wall Street News APP)

[Three Departments: Further Improve the Collection of Mining Rights Transfer Proceeds] The Ministry of Finance, the Ministry of Natural Resources, and the State Taxation Administration issued a notice on further improving the collection of mining rights transfer proceeds, clarifying that effective August 1, 2026, late payment fees on mining rights transfer proceeds will no longer be collected. If a mining rights holder fails to pay mining rights transfer proceeds on time and in full, a penalty of 0.2% per day will be charged starting from the date of default, and the total penalty will not exceed the principal amount overdue. The penalty for mining rights transfer proceeds shall be paid into the mining rights transfer proceeds revenue category and shared uniformly according to the central-local sharing ratio for mining rights transfer proceeds. Late payment fees incurred before the implementation of this notice shall continue to be paid according to the original regulations, and no penalty shall be imposed.

On the US dollar:

The US dollar index fell 0.1% overnight to 101.36. On a weekly basis, the index posted a second straight weekly gain, rising 0.6% for the week. As oil prices fell and the market reassessed US interest rate prospects, Treasury yields and the dollar moved lower. The CME FedWatch Tool shows that the probability of one rate hike this year remains high at 42%, while the probability of a second rate hike has fallen to 28% from 34% a week ago as inflation expectations have cooled. A Wall Street Journal survey indicates the University of Michigan consumer sentiment index, to be released at 10 a.m. ET (10 p.m. Beijing time), is expected to rise to 49 from 44.8. (Jin10 Data APP)

A Reuters poll showed that 78 of 102 economists surveyed expect the Fed to keep the federal funds rate unchanged at 3.50%-3.75% in 2026, compared with 72 of 102 economists in early June.

Artem Sakhbiev, FX strategist at BCA Research, said in a note that the dollar’s recent rebound appears overdone and lacks the support needed to break out of its trading range of the past year. The Fed revised up its rate forecasts at last week’s meeting and clearly focused on inflation. This pushed real yields sharply higher and eased concerns about political pressure for interest rate cuts, boosting the dollar. However, this move now looks largely exhausted. The Fed is likely to keep rates on hold, and the spread between short- and long-term yields could widen. (Jin10 Data APP)

According to Nick Timiraos, known as the “Fed mouthpiece,” sources say the search for a new president of the Federal Reserve Bank of Atlanta has stalled. The initial slate of candidates failed to produce a final choice, forcing the bank to relaunch a selection process that has already lasted seven months. On the surface, this was just a minor procedural hiccup. But at the same time, the independence of the US Fed is facing a severe test. Reserve Bank presidents are crucial to the Fed's independence: they participate in setting interest rates, and their appointment process is deliberately designed to avoid influence from Washington politics. (Jin10 Data App)

Fed official Kashkari stated that signs of widespread inflation led him to expect one rate hike this year in the Fed economic forecasts released earlier this month. Rates are expected to remain unchanged in 2027. In a media interview on Friday, Kashkari said: "I am concerned about inflation, not just related to the Middle East situation, but signs of broader inflationary pressures in the economy." The Iran war pushed up oil prices, and prices rose across many categories. This has intensified concerns among some Fed officials that inflation is becoming more broad-based and persistent, potentially requiring stronger action from the central bank. A report released earlier this week showed the May PCE annual rate came in at 4.1%, the largest increase since April 2023. Prices have exceeded the Fed's 2% target for over five years. In the dot plot forecasts released by the Fed last week, half of the officials who submitted dot plot projections expected at least one rate hike this year. (Jin10 Data App)

The US goods trade deficit widened to its highest level in over a year in May, as exports fell and imports rose. Data released by the Commerce Department on Friday showed the goods trade deficit expanded 27.4% from the previous month to $105.8 billion, compared to an expected deficit of $85 billion. US goods exports fell 5.4% in May, dragged down mainly by declines in multiple categories, including shipments of industrial supplies. This category covers crude oil and petroleum products. Over the same period, imports rose 3.6%. (From Wall Street CN APP)

In other currency news:

As London experiences record-breaking heat, Bank of England officials are starting to worry that weather could become the next shock driving up inflation, just as the previous supply shock is fading. Climate scientists increasingly expect a strong El Niño event to form later this year into 2027, disrupting global weather patterns. Now, economists are also concerned this could trigger a new round of supply shocks, push up food inflation, and once again frustrate global central banks' efforts to fight inflation. (From Wall Street CN APP)

On the macro front:

This week will see the release of data including the Eurozone June industrial sentiment index, Eurozone June economic sentiment index, US June Dallas Fed business activity index, Japan May unemployment rate, China June official manufacturing PMI, UK Q1 GDP annual rate final, UK Q1 current account, France June CPI monthly rate preliminary, Switzerland June KOF economic leading indicator, Germany June seasonally adjusted unemployment change, Germany June seasonally adjusted unemployment rate, Germany June CPI monthly rate preliminary, Canada April GDP monthly rate, US April FHFA house price index monthly rate, US April S&P/CS 20-City non-seasonally adjusted house price index annual rate, US June Chicago PMI, US May JOLTS job openings, US June Conference Board consumer confidence index, China June RatingDog manufacturing PMI, France June manufacturing PMI final, Germany June manufacturing PMI final, Eurozone June manufacturing PMI final, UK June manufacturing PMI final, Eurozone June CPI annual rate preliminary, Eurozone June CPI monthly rate preliminary, US June Challenger job cuts, US June ADP employment change, US June S&P Global manufacturing PMI final, US June ISM manufacturing PMI, US May construction spending monthly rate, Switzerland June CPI monthly rate, Eurozone May unemployment rate, US June unemployment rate, US June seasonally adjusted nonfarm payrolls, US initial jobless claims for the week ending June 27, US June average hourly earnings annual rate, US June average hourly earnings monthly rate, US May factory orders monthly rate, China June RatingDog services PMI, France May industrial output monthly rate, France June services PMI final, Germany June services PMI final, Eurozone June services PMI final, UK June services PMI final, and other data.

Also worth watching this week: 2027 FOMC voting member and Richmond Fed President Barkin delivers a speech; The ECB holds its Central Banking Forum in Sintra, running through July 1; The 2026 Beijing Space Computing Conference takes place from June 29–30; ECB President Lagarde speaks in Sintra; The Reserve Bank of Australia releases its June monetary policy meeting minutes; The ECB holds its Central Banking Forum in Sintra; Technical talks between the US and Iran (pending); Fed Chairman Warsh, ECB President Lagarde, Bank of England Governor Bailey, and Bank of Canada Governor Macklem speak at the ECB Forum; The ECB holds its Central Banking Forum in Sintra; ECB President Lagarde delivers a speech; Bank of England Governor Bailey speaks on the coordination of fiscal and monetary policy; And China will initiate a new round of adjustments to its refined oil product pricing window.

Notably, on July 1, China-Hong Kong Stock Connect will be closed for the day in observance of the Hong Kong Special Administrative Region Establishment Day, with both Northbound and Southbound trading shut. On July 3, the US-New York Stock Exchange will close for the US Independence Day holiday; Trading in precious metals, energy, forex, US Treasury, and equity index futures contracts on the US-Chicago Mercantile Exchange (CME) will end early on July 4 at 01:00 Beijing time due to the US Independence Day holiday; Trading in Brent crude oil futures contracts on the US-Intercontinental Exchange (ICE) will end early on July 4 at 01:30 Beijing time for the same reason.

In crude oil:

Overnight, both oil futures declined, with WTI falling 2.34% and Brent falling 2.52%. On a weekly basis, WTI futures posted a third straight weekly decline, dropping 7.4% for the week; Brent futures also fell for a third straight week, losing 8.06%.

Spot Brent crude oil prices have fallen back to pre-war levels, and the market for near-month contracts has been in contango—where near-term prices are lower than longer-term ones—for seven consecutive days, reflecting temporary oversupply. Tariq Zahir, a managing member at Tyche Capital Advisors, noted that oil prices "fell too far, too fast," that the ceasefire remains fragile and uncertainty persists in the Strait of Hormuz, and that he expects volatility to continue. Rich Privorotsky, head of One-Delta at Goldman Sachs, pointed out that Iran has begun shows of force near the Strait of Hormuz, some vessels have altered their routes, and the inventory buildup in the Gulf is gradually flowing into the market. He believes that upside potential for oil prices is limited in the near term, but that the case for significantly further downside from current levels is equally weak. (From Wallstreetcn APP)

US natural gas drilling rigs recorded their largest single-week increase in four years. Data from Baker Hughes showed that the number of active oil drilling rigs operated by US energy enterprises reached 440 last week, marking a two-week consecutive increase, up from 433 the previous week. Active natural gas drilling rigs rose to 573, recording the largest gain since June 2022, compared with the prior figure of 563. (From Wall Street Cn APP)

A report from the US Energy Information Administration (EIA) indicated that US refining capacity decreased by 263,000 barrels per day (bpd) in 2025, a decline of 1.43%. This was primarily driven by the planned conversion of a major refinery in Houston and the closure of a refinery in the Los Angeles area due to market dynamics, which is known for strict environmental regulations. Marathon Petroleum, headquartered in Findlay, Ohio, maintained its position as the largest US refiner with a total refining capacity of 2.986 million bpd, accounting for 16.4% of the nation’s total capacity. (From Wall Street Cn APP)

Furthermore, Iraq’s Ministry of Oil stated that OPEC has begun to gradually restore Iraq’s pre-war production quota, a move which will strengthen Iraq’s output capabilities and support the recovery of the oil sector. A high-level consensus has been reached within OPEC, fully taking into account Iraq’s past special circumstances and current actual needs. (From Wall Street Cn APP)

Barclays said it has lowered its Brent crude oil price forecasts, cutting the 2026 estimate from $100 per barrel to $96, and the 2027 estimate from $88 to $85, citing the recovery of oil shipments through the Strait of Hormuz. Oil flows through the Strait of Hormuz have rebounded substantially, reaching about 80% of pre-war levels. However, this normalization process remains incomplete. The bank noted that Iran’s assertion of control through fee impositions and coordination mechanisms has created frictions and may potentially delay a full recovery. A temporary deal reached last week aimed at ending the US-Israeli war against Iran has allowed traffic on the Strait of Hormuz shipping route to resume. (From Wall Street Cn APP)

Recommended Reading:

![[SMM Flash News] Germany's BSH Amends Offshore Wind Plan to Enhance Viability for 4 GW 2027 Auction](https://imgqn.smm.cn/usercenter/QnbfL20251217171735.jpeg)

![[SMM Flash News] NexMetals' Selkirk Project Resource Surges by Nearly 70%, Boosting Copper Equivalent to 1.1 Billion Lbs](https://imgqn.smm.cn/usercenter/JMPtY20251217171734.jpeg)

![[SMM Flash News] UK's Ofgem Selects 16 LDES Projects Totaling 7.6 GW Under Cap and Floor Regime](https://imgqn.smm.cn/usercenter/VphiQ20251217171736.jpg)