I. H1 Trade Overview: Lead Ingot Imports Surge, Exports Remain Sluggish

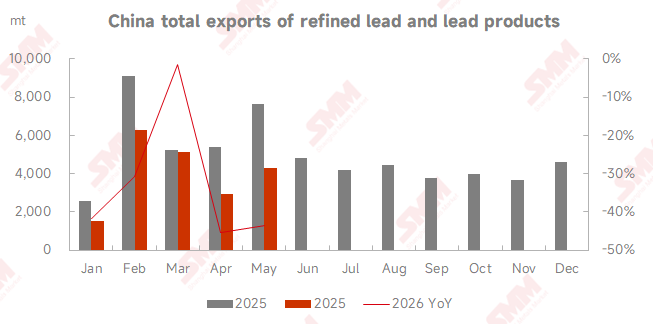

According to data from China Customs, in January-May 2026, China’s combined imports of refined lead and lead products totaled 248,443 mt, surging 291.06% YoY on a cumulative basis. The import window was wide open for most of H1, and overseas cargoes kept pouring in. Total imports had already exceeded the full-year 2025 level. On the export side, combined exports of refined lead and lead products in January-May amounted to only 20,197 mt, down 32.49% YoY, remaining at low levels.

Monthly import data showed a steady uptrend: In January-February, cumulative imports of refined lead were 33,412 mt, and single-month YoY growth in February topped 11 times. In March, combined imports of refined lead and lead alloy reached 49,399 mt. In April, combined imports hit 57,343 mt, up 15.69% MoM and up 680.12% YoY. In May, refined lead imports stood at 36,684 mt, edging down just 0.66% MoM. With lead alloy imports of 23,414 mt, total imports for the month came close to 60,100 mt, soaring 731.65% YoY. The high import level in May was supported by three factors: the elevated SHFE/LME price ratio created a steady import arbitrage window; concentrated arrivals of cargoes from India and South Korea; and a supply gap caused by domestic smelting maintenance and production cuts at secondary lead smelters. During the same period, LME inventories surged to 314,000 mt, and low-quality lead ingots were ample outside China, while spot premiums for high-grade lead ingots in Southeast Asia remained persistently high.

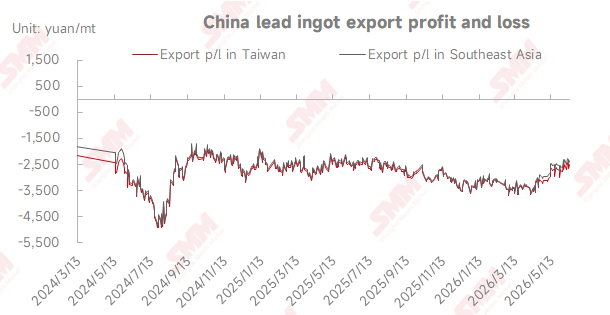

The export market remained weak. In March, refined lead exports were 3,190 mt, then plunged 70.96% MoM to 926.52 mt in April. In May, exports rebounded 128.99% MoM to 2,121.59 mt, but still fell 61.80% YoY. Export cargoes mainly went to Vietnam, Malaysia, and Taiwan, China. The inverted price spread between Chinese and overseas markets had long suppressed export willingness.

II. Review of the Interplay Among Prices, Inventories, and Trade Window Dynamics

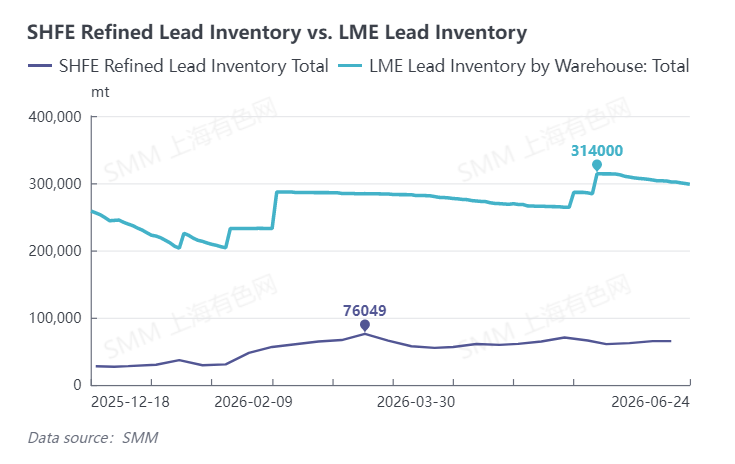

In H1, the market persistently exhibited a pattern where LME outperformed SHFE, with LME lead trading consistently above SHFE lead, which was the root cause of the persistently open import window. From January to March, both the overseas and domestic markets fell in tandem. In April, LME lead continued to strengthen while SHFE lead was in the doldrums, significantly widening the SHFE/LME price ratio and offering ample import arbitrage space. In May, the situation reversed, with the SHFE/LME price ratio declining, import profits shrinking markedly, and the price spread logic between Chinese and overseas markets gradually reversing. Inventory trends diverged sharply in and outside China: LME inventory outside China surged to 314,000 mt at end-May, hitting a 13-year high, then pulled back slightly to 300,700 mt in June, reflecting a global oversupply of low-end lead ingots; China's SMM social inventory across five regions exceeded 70,000 mt in mid-May and slowly destocked to 67,700 mt in June, with SHFE warrants rising in tandem, keeping domestic spot supply pressure persistent.

III. Short-term Import and Export Forecast for June

Import side: Combined imports of refined lead and lead materials are expected to pull back to 35,000-45,000 mt in June. On the one hand, the lower LME lead price and LME spot discounts have squeezed import profits, while production resumptions at some domestic secondary lead smelters have filled supply gaps, weakening the drive for imports; on the other hand, export orders placed in May are still arriving with a lag, preventing a cliff-like drop in imports. Export side: Exports are expected to remain low at 2,500-3,500 mt. The domestic battery off-season continues, EXW cargoes from smelters are scarce, and anti-dumping tariffs from the Middle East make it difficult for the export window to open substantively.

IV. Key Variables to Monitor in H2

1. SHFE/LME price ratio fluctuations: directly determine the opening/closing of import-export arbitrage windows and trade flows;

2. Progress of secondary lead production resumptions in China: determine the size of the domestic supply gap, indirectly affecting import demand;

3. Actual fulfillment of end-use consumption in Q3: restocking in the peak season exceeding expectations will provide periodic boosts to imports;

4. Supply chain disruptions outside China: Middle East situations and shipping cost changes affect spot premiums for lead ingots outside China;

5. US Fed monetary policy: US dollar fluctuations indirectly shift the central tendency of the price ratio in and outside China.

Q3 (July-September): Batteries enter their traditional peak consumption season, and downstream restocking will provide periodic import support. However, considering the concentrated resumption of secondary lead production in China, self-sufficiency in raw materials will improve, and import dependency will marginally decline, with average monthly imports expected at 30,000-40,000 mt. Q4 (October-December): If the SHFE/LME price ratio continues to pull back and the import window closes periodically, monthly refined lead imports will further shrink to 20,000-30,000 mt. According to comprehensive calculations, total imports of refined lead and lead materials for full-year 2026 will fall within the range of 320,000-360,000 mt.

![Holiday Factors Drive Significant Decline in Lead-Acid Battery Weekly Operating Rate [SMM Lead-Acid Battery Weekly Operating Comment]](https://imgqn.smm.cn/usercenter/mfCMp20251217171721.jpeg)

![End-user procurement is weak and inventories are rising, and destocking space is limited in the short term [SMM Secondary Lead Inventory Weekly Review]](https://imgqn.smm.cn/usercenter/TmYox20251217171721.jpeg)

![SHFE/LME Price Ratio Rebounds, Import Crude Lead Supply Activity Rises [SMM Secondary Crude Lead Weekly Review]](https://imgqn.smm.cn/usercenter/riosq20251217171722.jpg)