SMM, June 25:

Metal markets:

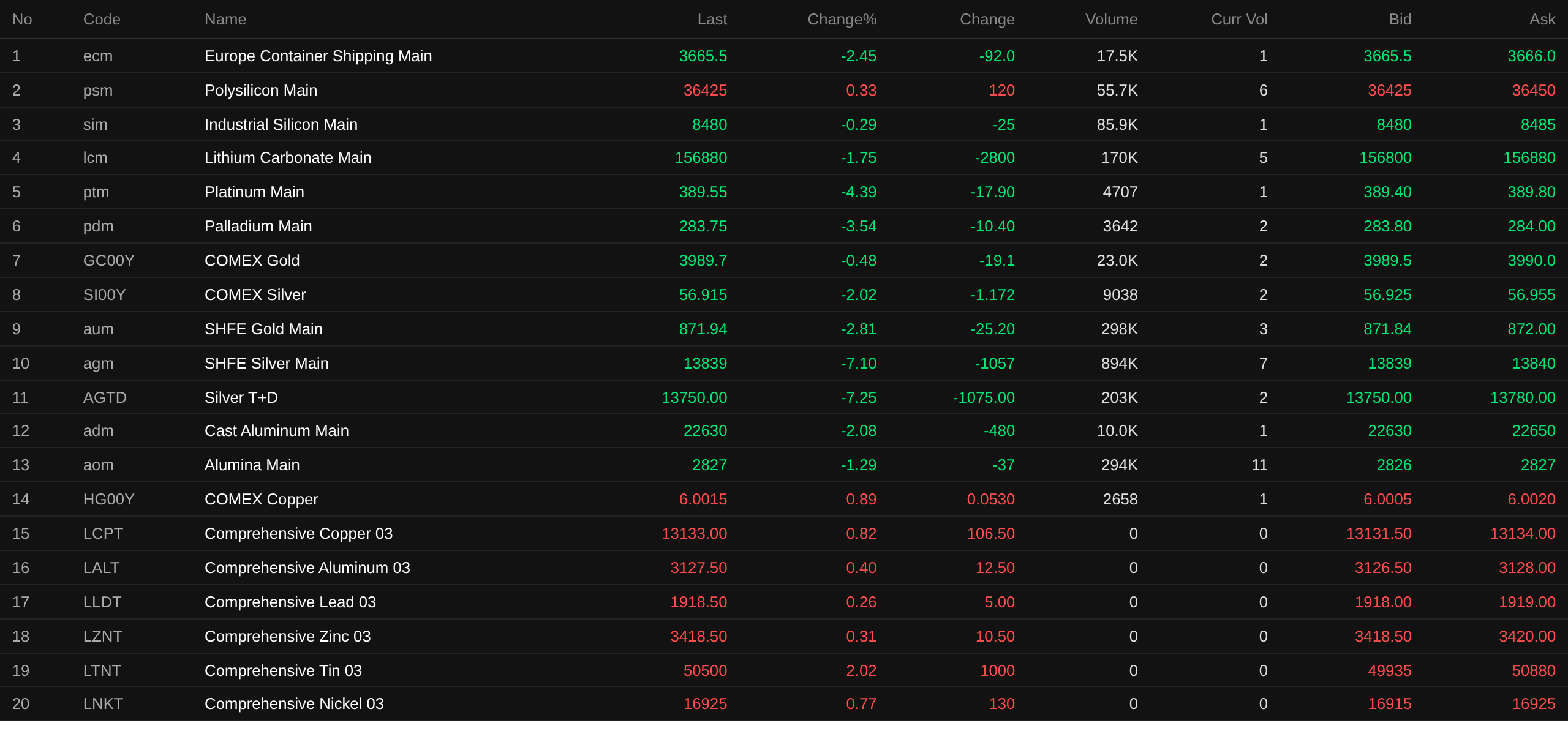

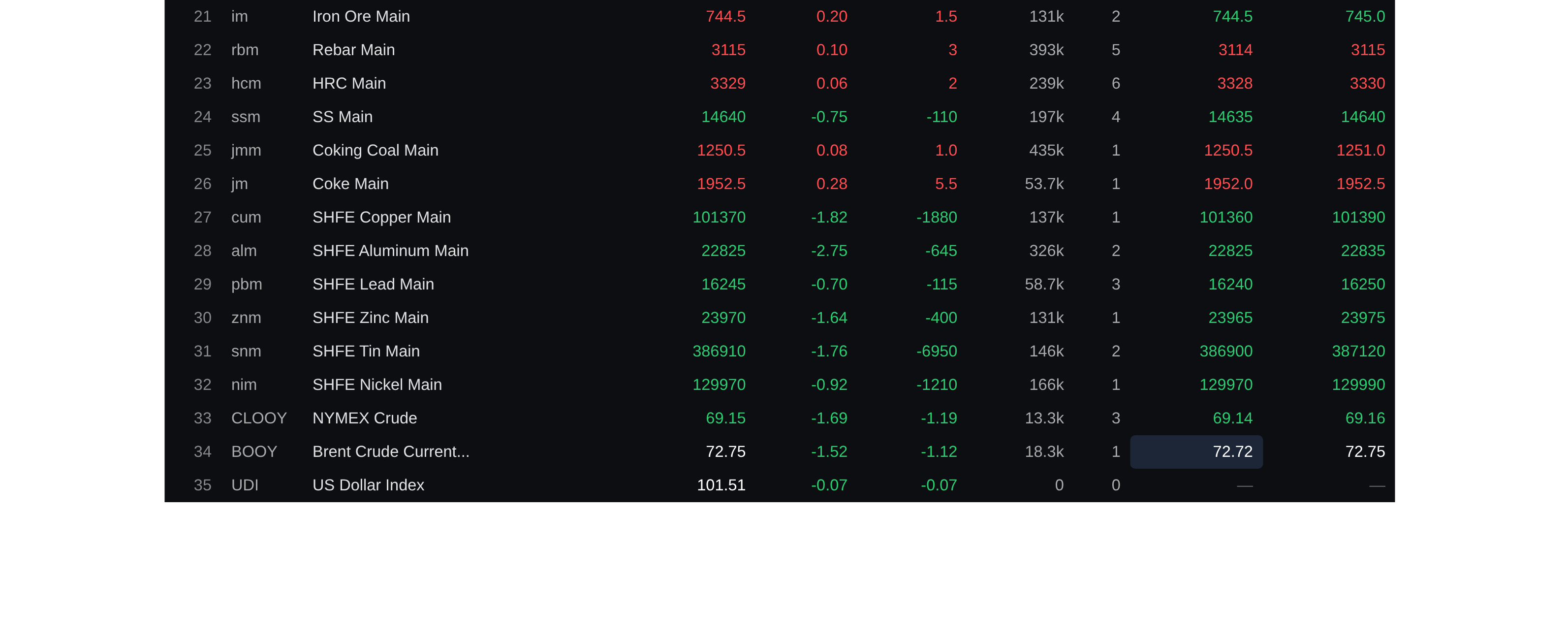

As of the noon close, base metals on the domestic market fell across the board, with SHFE copper down 1.82%, SHFE aluminum down 2.75%, SHFE lead down 0.7%, SHFE zinc down 1.64%, SHFE nickel down 0.92%, and SHFE tin down 1.76%.

Additionally, the most-traded cast aluminum futures fell 2.08%, the most-traded alumina contract fell 1.29%, the most-traded lithium carbonate contract fell 1.75%, the most-traded silicon metal contract fell 0.29%, and the most-traded polysilicon futures rose 0.33%.

Ferrous metals mostly rose, with only stainless steel down 0.75%. Iron ore rose 0.2%, rebar rose 0.1%, and hot-rolled coil edged up. In the coking coal and coke segment: the most-traded coking coal contract inched up 0.08%, and the most-traded coke contract rose 0.28%.

In overseas base metals, as of 11:38, LME metals rose across the board. LME copper rose 0.82%, LME aluminum rose 0.24%, LME lead rose 0.6%, LME zinc rose 0.31%, LME tin rose 2.02%, and LME nickel rose 0.77%.

In precious metals, as of 11:38, COMEX gold fell 0.48%, and COMEX silver fell 2.02%. In domestic precious metals: SHFE gold declined 2.81%, hitting an intraday low of 868.34 yuan/g; the most-traded SHFE silver contract fell 7.1%, with an intraday low of 13,560 yuan/kg.

Additionally, as of the noon close, the most-traded platinum futures fell 4.39%, and the most-traded palladium futures fell 3.54%.

As of the noon close, the most-traded containerized freight index (Europe) futures fell 2.45% to 3,665.5 points.

As of 11:38 on June 25, midday quotes for selected futures:

Spot and fundamentals

Silver: In the spot market, downstream consumption recovered somewhat after silver continued to decline. Morning quotes in Shanghai were mainly at TD parity to +20 yuan/kg...

Macro front

Domestic front:

[China's power generation capacity exceeds 4 billion kW] On June 25, the National Energy Administration announced that as of the end of May 2026, China's power generation capacity reached 4.01 billion kW, ranking first globally. Non-fossil energy capacity became the absolute mainstay of capacity additions, and the energy mix continued to improve. The share of coal-fired power capacity fell from 61% in 2010 to 32% in May 2026; the share of non-fossil energy capacity rose from 25% in 2010 to 62% in May 2026; and the share of renewable energy capacity rose from 24% in 2010 to 61% in May 2026. (Xinhua)

[PBOC reverse repo net injection of 322.5 billion yuan today] The PBOC conducted 370.5 billion yuan of 7-day reverse repos and 500 billion yuan of 1-year medium-term lending facility (MLF) operations today. With 300 billion yuan of 1-year MLF and 248 billion yuan of 7-day reverse repos maturing today, this resulted in a net injection of 322.5 billion yuan. ((Jin10 Data APP)

US dollar:

As of 11:38, the US dollar index fell 0.07% to 101.51. All large US banks passed the Fed's annual stress test, paving the way for banks to boost share buybacks and dividends by tens of billions of dollars. The stress test aims to assess how Wall Street lenders would fare under hypothetical financial system shocks. Unlike in previous years, the 2026 test results will not affect capital requirements, as the Fed is continuously revising the test to make it more friendly to banks. This year's test examined how 32 large lenders would withstand a severe global shock amid greater stress in commercial and residential real estate markets and corporate debt markets. The hypothetical scenario included a severe global recession, a 39% drop in commercial real estate prices, and a 30% decline in residential prices. The unemployment rate also surged to a peak of 10%, with a corresponding decline in economic output. The regulators said, "Despite absorbing over $708 billion in loan losses under this year's hypothetical scenario, total capital fell by just 1.6 percentage points, still above the minimum capital requirement."

According to CME FedWatch, the probability that the Fed keeps rates unchanged in July is 65.8%, while the chance of a cumulative 25bp rate hike is 34.2%. By September, the probability of rates remaining unchanged is 33.6%, of a cumulative 25bp hike is 49.7%, and of a cumulative 50bp hike is 16.7%.

US Treasury Secretary Bessent praised Fed Chairman Warsh for eliminating forward guidance, and said no one should make dot plot forecasts. On the economy, he expects real wage growth to return to the pace seen before April and expects the economy to accelerate for the rest of the year without fueling inflation. He stressed that the dominance of the US dollar is crucial. He believes that once the situation in Ukraine is over, Russia will want to return to the dollar system, while a new Venezuela is returning to that system. During a period of rate cuts, the dollar can still remain strong, and the US is willing to take the right measures to keep the dollar strong. (Jin10 Data APP)

On the data front:

Today will see the release of Australia's May seasonally adjusted unemployment rate, Germany's July GfK Consumer Confidence Index, US initial jobless claims for the week ending June 20, US May core PCE price index year-on-year, US May personal spending month-on-month, the final reading of US Q1 real GDP annualized quarter-on-quarter, the final reading of US Q1 real personal consumption expenditures quarter-on-quarter, the final reading of US Q1 core PCE price index annualized quarter-on-quarter, US May core PCE price index month-on-month, US May durable goods orders month-on-month, and other data.

Additionally, attention should be paid to: Nvidia's annual shareholder meeting; the Bank of Canada's release of monetary policy meeting minutes; the US Federal Reserve's release of annual bank stress test results; Bank of Japan Governor Ueda Kazuo's attendance at a central bank lecture event hosted by the International Monetary Fund (IMF); Micron Technology's fiscal 2026 Q3 earnings call; and 300 billion yuan in 1-year medium-term lending facility (MLF) and 248 billion yuan in 7-day reverse repos maturing today.

Crude oil:

As of 11:38, oil prices on both exchanges continued to decline, extending losses from the previous three trading days, with WTI falling 1.69% and Brent falling 1.53%. Oil prices pulled back their wartime gains on Thursday as the market bet on improving global crude supply, with tankers that had been stranded in the Persian Gulf for months beginning to sail out of the Strait of Hormuz. According to data from maritime analytics firm Kpler, more than 20 tankers carrying approximately 35 million barrels of crude oil have passed through the Strait of Hormuz since a US-Iran agreement reopened this critical shipping lane. These non-Iranian tankers had been stuck in the Persian Gulf for over three months after Tehran effectively blockaded the waterway early in the conflict. Most of these tankers are expected to arrive at Asian destinations by early August. Citigroup stated that the worst may be over for commodity futures carry trade strategies, which suffered massive losses during the US-Iran war as short positions in near-month contracts were hit hard by soaring prices, while long positions in forward contracts were bought. Citi noted that the current base case is for significant de-escalation, and predicts that as Strait of Hormuz shipping normalizes, Brent crude prices will fall to $60-$65 per barrel over the next 6 to 12 months. (Jin10 Data APP)

Spot market overview:

►

►

►

►

►

►

►

►

►

►

►

►

►

►

![[SMM Computing Power Flash] An Intelligent Computing Company Quoted Monthly Rental Prices for Multiple GPU Models Including H100, A100, RTX 5090, All Requiring Annual Contracts](https://imgqn.smm.cn/usercenter/kLgYV20251217171736.jpg)

![During last night's night session, the SHFE/LME price ratio surged once again, and in the morning market, active demand drove premiums to continue rising. [SMM Yangshan spot copper]](https://imgqn.smm.cn/usercenter/JYzFE20251217171714.jpeg)

![SHFE Aluminum Futures Continued Sharp Decline, Purchasing Sentiment in East China Rises [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/LFPBA20251217171653.jpg)