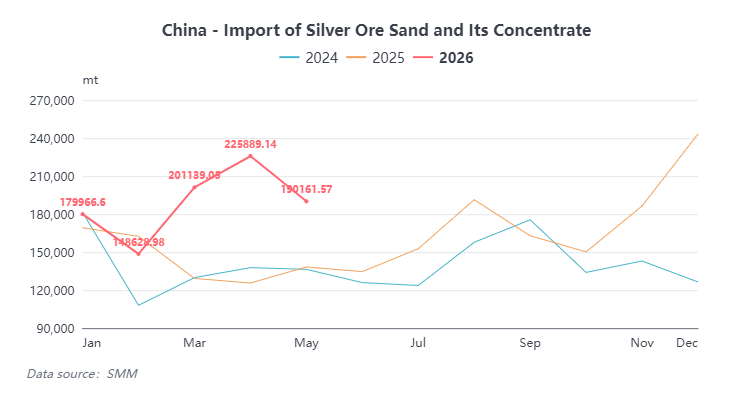

China Silver-Bearing Concentrate Imports Analysis: May Pullback MoM, Peru Remains Top Source

In May 2026, China's imports of silver-bearing concentrates stood at 190,000 mt, down 15.8% MoM; cumulative imports from January to May reached 946,000 mt, up 30.4% YoY. Imports have been expanding since the beginning of this year, mainly due to the persistent premium between SGE and LBMA spot silver prices, which encouraged overseas miners to increase exports to China. However, since May, the premium has narrowed, and imports subsequently pulled back.

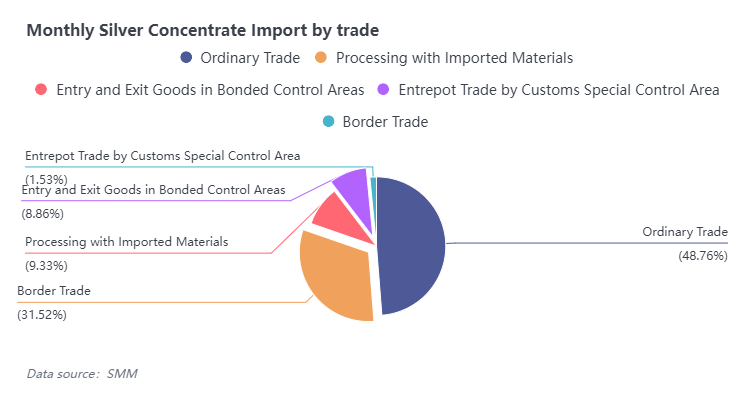

By trade mode, Ordinary Trade accounted for 48% of imports in May, indicating continued inflows of speculative mine resources, while processing trade with imported materials, in which domestic smelters are mainly involved, accounted for only 9.33%, sliding MoM.

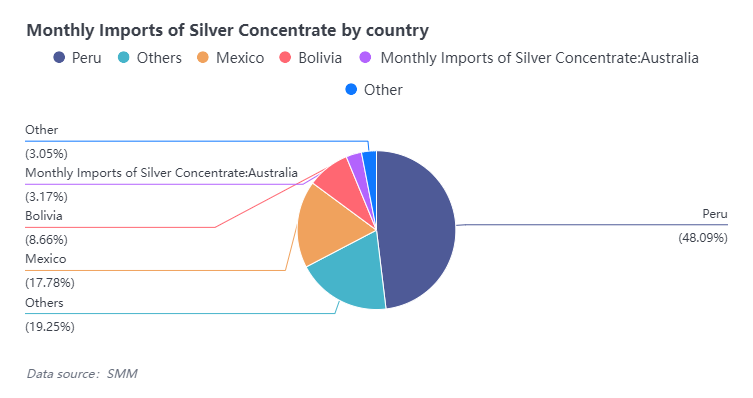

By origin, Peru remained the largest source of imports, accounting for 48%. On May 11, 2026, the Peruvian Presidency issued Emergency Decree No. 003-2026, providing emergency assistance to the state-owned oil company Petroperú through a combination of fiscal guarantees and innovative financial instruments to address a nationwide energy shortage crisis. In the short term, this event had limited impact on silver ore supply in May, but it could pose potential risks to the output of small and medium-sized mines in the long run.

Refined Silver Trade Analysis: Exports Pulled Back in May, Imports Contracted Sharply, Trade Window Gradually Returning to Normal

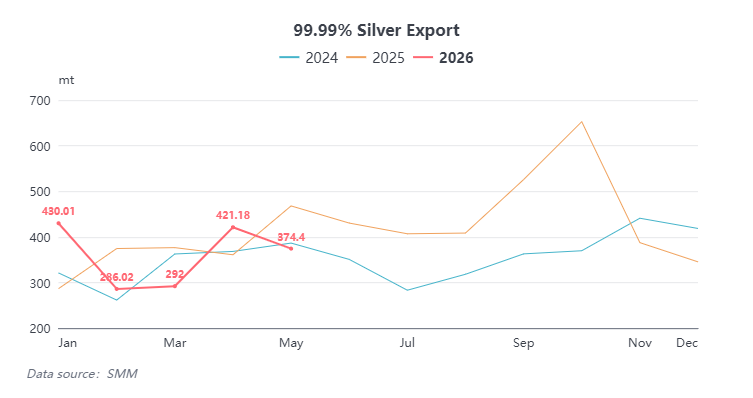

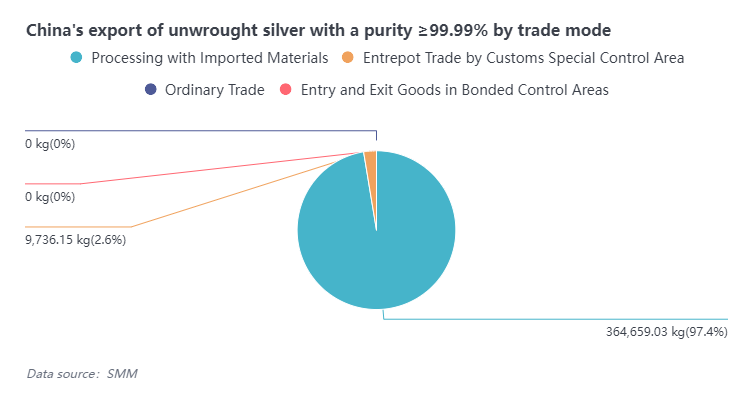

On the export side, China's exports of 99.99% refined silver in May 2026 reached 374.4 mt, down 11% MoM, and cumulative exports from January to May totaled 1,803 mt, down 3.38% YoY, of which 97.4% was under processing trade with imported materials.

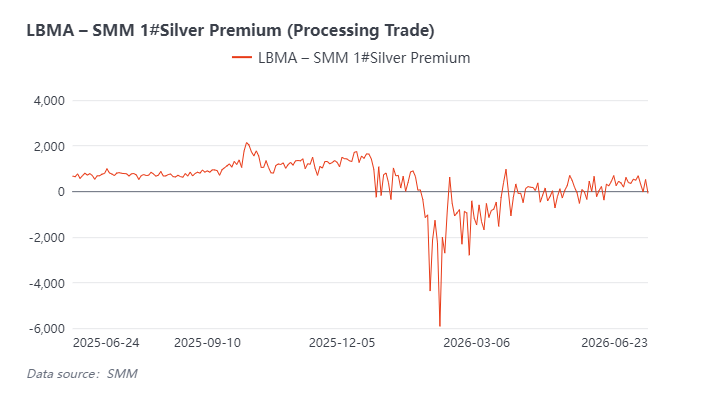

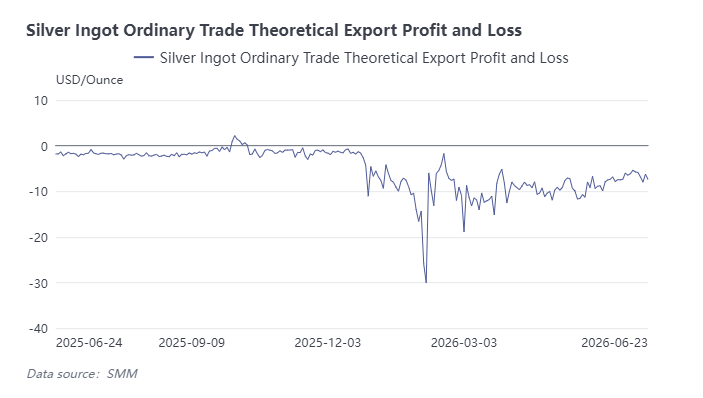

According to SMM's profit and loss model, the export window for processing trade with imported materials remained open in May, prompting some smelters to export during the month; meanwhile, Ordinary Trade remained in a loss zone, around $10/oz, but the premium was gradually narrowing.

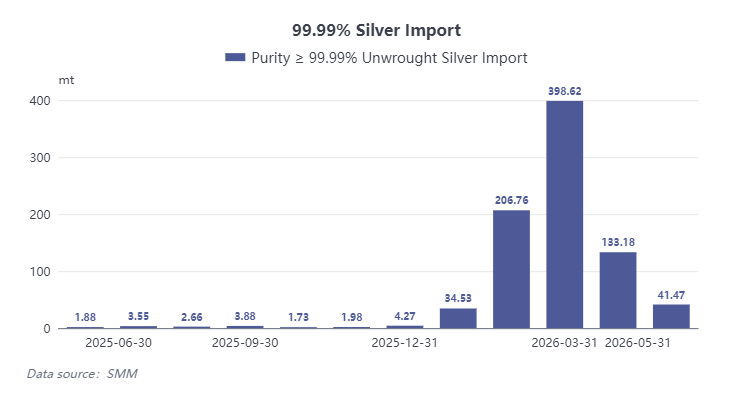

On the import side, imports of refined silver in May were 41.47 mt, down sharply by 69% MoM, and cumulative imports from January to May reached 814.56 mt, surging 4,919% YoY. As the premium narrowed, the import window gradually closed in May, curbing market stockpiling demand. The high premiums in February-March this year had front-loaded some of Q2's actual demand, and the large volume of imported refined silver increased social inventory pressure. Coupled with weak industrial demand, this caused spot premiums to shift to a wide discount in April-May.

Looking ahead, trade in June is expected to gradually return to normal, and full-year refined silver exports are still expected to remain at a relatively high level, supported by steady demand for jewelry and electronic components in Southeast Asia and other regions. On the spot premiums front, the LBMA Hong Kong premium had already pulled back to a discount of 20-30¢/oz by mid-to-late June, and some smelters will opt to export as the processing trade export window reopens, easing domestic inventory pressure. Currently, market quotes for T+D have shifted from a wide discount in May to parity to a slight premium.

![[SMM Analysis] Hawkish Fed Pressures Gold & Silver; Long-Term Bullish Outlook Intact](https://imgqn.smm.cn/usercenter/gePcx20251217171735.jpg)