HRC prices:

Over the coming year, from 2026 to 2027, China has nearly 40 million mt of HRC capacity projects under planning and construction, with production expected to increase further in 2026. Demand side, China's macro policies are expected to remain accommodative, and the manufacturing sector is likely to continue introducing policies to stimulate consumption, with demand expectations staying resilient. However, affected by anti-dumping measures and export structure adjustments, the decline in HRC exports will weigh on the domestic high-supply pattern. Overall, HRC prices are expected to continue hovering at lows in 2026. But considering that overseas geopolitical conflicts are pushing up inflation expectations and transmitting to commodity prices, coupled with coal and coke prices hitting bottom in 2025 and entering a new recovery uptick cycle, against the backdrop of cost push, the average HRC price may rebound slightly compared to 2025.

Looking ahead to the next five years, considering that the peak period of new production capacity has passed, with the accelerated promotion of industry mergers and reorganizations and the continuous optimization of the capacity structure, HRC supply growth is expected to gradually slow down and stabilize starting from 2027. SMM expects that around 2028, a policy package of supply-side production restrictions plus steel export scale tightening may re-emerge, and the improvement in the overcapacity contradiction may bring about a round of upside opportunities for HRC prices.

However, unlike the intensity of the 2015 supply-side reforms that were coupled with real estate easing and shantytown renovation destocking policies, after the phased capacity removal ends, the overall downward trend in China's steel consumption will be hard to reverse, which will limit the upside room of this HRC price rally driven by supply-demand imbalance easing. Additionally, the supply-demand pattern of iron ore trending looser will also pull down costs, and HRC prices are expected to come under pressure again after a brief rise.

Steel mill profits:

Considering that China's surplus steel capacity is resolved through steel exports, this necessitates China's steel prices to stay relatively low to support price advantages and orders, which will also limit the upside room of China's steel prices, steel mill profits are expected to remain at low marginal levels in H2 2026.

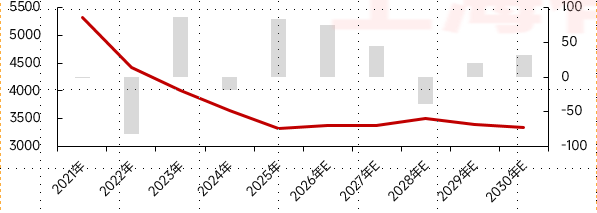

China Hot-Rolled Coil Annual Supply-Demand Balance

(The line chart represents China's HRC price, and the bar chart represents the HRC balance.)

![[SMM Steel] Turkey Rebar Prices Pause Decline as Mills Prioritize Cash Flow Amid Geopolitical Wait-and-See](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)

![[SMM Lecong HRC Inventory] This week, inventory destocking in Lecong slowed down.](https://imgqn.smm.cn/usercenter/ikbxI20251217171718.jpg)