I. Total Import and Export Overview: Deepening Pattern of "Rising Imports, Falling Exports"

In May 2026, China's copper cathode import and export market continued and deepened the pattern of "rising imports, falling exports". Driven by phased changes in domestic demand and the import arbitrage window, copper cathode imports kept climbing steadily, while exports contracted notably following the high base earlier.

According to the total trade data released by the General Administration of Customs:

• Import side (Steady Climb): In May, China's copper cathode imports rebounded to 282,300 mt, up 4.38% MoM and up 10.20% YoY. The continued rebound in May imports effectively eased the tightness in parts of the domestic spot market. However, from a longer-term perspective, cumulative imports from January to May totaled 1.1443 million mt, still down 15.69% YoY, reflecting a structural adjustment in overall long-term contract and spot flows this year compared with previous years.

Export side (Notable Pullback): In May, China's monthly copper cathode exports were 19,900 mt, down sharply by 22.45% MoM and 41.14% YoY. While the monthly export pullback was pronounced, cumulative exports from January to May reached 275,200 mt, still posting positive cumulative growth of 23.35% YoY.

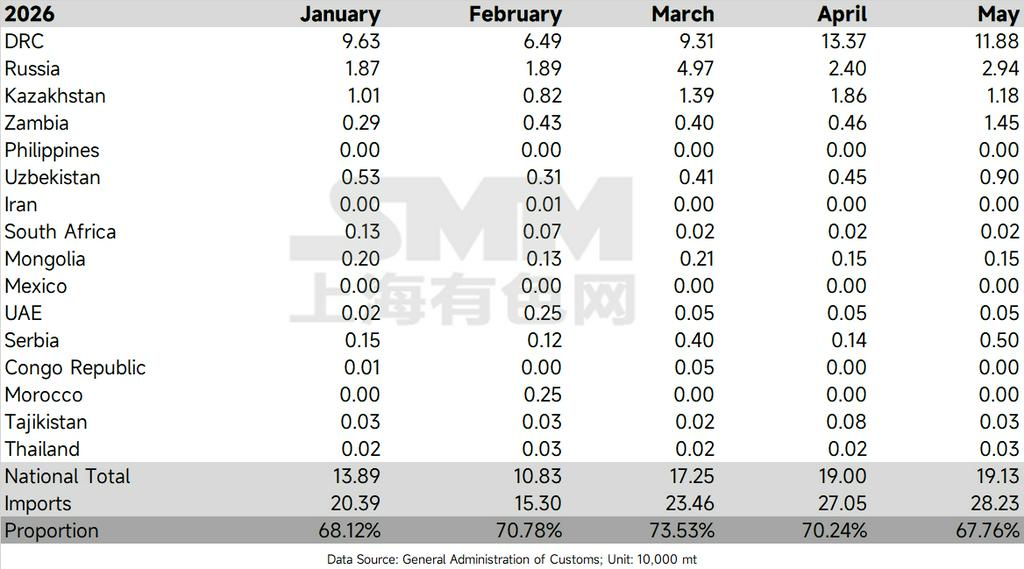

II. Import Structure Analysis: High-Level Fluctuations in Non-Registered Copper Share and Intensifying Country Divergence

A deeper look into the import structure reveals that in May, exports to China from major non-registered copper cathode producing countries showed notable divergence. Driven by this flow shift, total imports from these major non-registered cathode producers reached 191,300 mt in May.

In terms of share, these core shipments accounted for 67.76% of total imports, pulling back 2.48 percentage points from the April high of 70.24%. Although the share edged down slightly, it remained at a high level near 70%, indicating that non-registered copper remains the dominant source of China's copper cathode imports.

Performance by key country:

• DRC — Expected Pullback: The DRC, which had previously stood out, saw its copper cathode exports to China drop to 118,800 mt in May, a notable decline from 133,700 mt in April. This was in line with market expectations for production cuts due to limited hydrometallurgical copper capacity caused by shortages of auxiliary materials such as sulphuric acid and sulfur.

• Russia and Kazakhstan — Stable Fluctuations: In May, copper cathode imports from Russia edged up to 29,400 mt, while supplies from Kazakhstan pulled back to 11,800 mt.

• Zambia — Counter-Trend Surge: Zambia was a structural highlight in May, recording 14,500 mt, a more than doubling from 4,000 mt in March and 4,600 mt in April. The underlying reason was a combination of maintenance scheduling mismatch and full-capacity operations at local smelters. The two major Zambian smelters, Mopani and Chambishi, plan to undertake long-term maintenance in H2, and in preparation for the shutdowns, they accelerated cathode inventory clearance and deliveries in May, creating a typical "export rush" effect. In addition, the Zambian government's relaxation of restrictions on exporting by-product sulphuric acid to the DRC also confirmed their very high smelting operating rates and ample inventory.

III. Market Outlook: Watch for Maintenance-Led Output Reduction and Cross-Market Siphoning Effect

The high-level volatility in the import share from major non-registered cathode producers indicates that changes in overseas supply chains are deepening their penetration into the Chinese market. The MoM rebound in May imports was primarily driven by domestic restocking demand and a phased improvement in the import window.

Going forward, close attention should be paid to the actual output reduction from concentrated maintenance in Zambia in H2 and whether the raw material shortages in the DRC will see marginal improvement. If downstream enterprises in China cannot sustain the absorption of these high inflows of copper cathode as the market enters the off-season, domestic visible inventories may once again face localized inventory buildup pressure.

Moreover, given the persistently wide inter-market spread between COMEX and LME, coupled with the fact that US tariff policy on copper products has yet to be substantively implemented, the "siphoning effect" of the North American market on global copper cathode supplies remains significant. Until tariff policies become clear, the structural diversion of overseas supplies is expected to persist, and any further expansion in China's copper cathode imports will likely continue to be under pressure.

![Price Constraints and Maintenance Drag Down Chinese Copper Anode Imports [SMM Analysis]](https://imgqn.smm.cn/usercenter/mpocQ20251217171712.jpg)