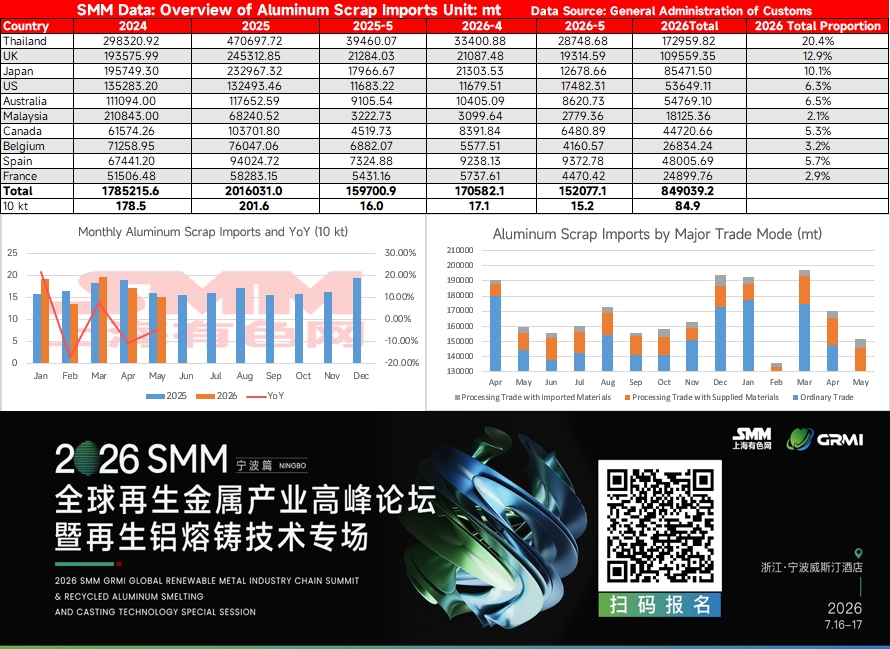

General Administration of Customs data showed that aluminum scrap imports in May 2026 stood at approximately 152,000 mt, down 11.1% MoM from 171,000 mt in April and also below the 160,000 mt recorded in May 2025, initially establishing a pullback trend in imports this year.

Escalating US-Iran tensions recently fueled risk-off sentiment, driving LME aluminum prices sharply higher and directly lifting spot aluminum scrap quotations outside China. Since aluminum scrap pricing generally tracks LME aluminum, overseas suppliers' willingness to hold prices firm strengthened notably, pushing up procurement costs for Chinese import traders. Traders reported that overall landed costs for imported aluminum scrap were already significantly above early-year levels and above domestic aluminum scrap prices, directly curbing procurement appetite.

Meanwhile, energy prices in Europe stayed high, with aluminum capacity in multiple countries remaining constrained by electricity cost pressures and primary aluminum resources generally tight. To fill the raw material gap, secondary aluminum enterprises in Europe intensified competition for aluminum scrap feedstock, reducing the willingness to export scrap to external markets and indirectly tightening supply channels to China. Shipments to China from European sources—including the UK, Spain, Belgium, and France—all pulled back to varying degrees in May 2026, with the combined effect of these factors not to be overlooked.

By source country structure, in January-May 2026, Thailand remained the top supplier at approximately 173,000 mt, accounting for 20.4%; the UK, Japan, and Australia ranked second through fourth, accounting for 12.9%, 10.1%, and 6.5%, respectively. In May, however, arrivals from major sources broadly contracted: Thailand's arrivals were about 28,700 mt, down 14% from 33,400 mt in April; monthly arrivals from the UK and Japan also pulled back in tandem, while declines from the US and Australia were equally pronounced. Notably, imported aluminum scrap typically involves a 1–3 month ocean freight lead time. The impact of traders' sharply reduced procurement volumes will transmit through this lead time and is expected to concentrate in Q3. If China's aluminum scrap demand does not weaken in tandem by then, the supply gap for imported cargo could widen, providing some support for domestic aluminum scrap prices.

Overall, under the combined influence of multiple factors—the upward shift in LME aluminum price center, restricted aluminum scrap exports from Europe, and domestic import traders proactively reducing inventory risk exposure—the contraction in imported aluminum scrap supply is unlikely to rapidly reverse in the near term. If downstream aluminum processing demand recovers seasonally as expected in Q3, the "scissors gap" between the import side and the demand side could periodically drive up aluminum scrap spot premiums. It is recommended to keep monitoring the changes in offering prices from key source countries and the pace of vessel arrivals.

![Aluminum Fluoride Prices Consolidate Amid High Raw Material Costs and Weak Downstream Demand [SMM Analysis]](https://imgqn.smm.cn/usercenter/kRRxA20251217171652.jpg)