High-carbon Ferrochrome

Price Review

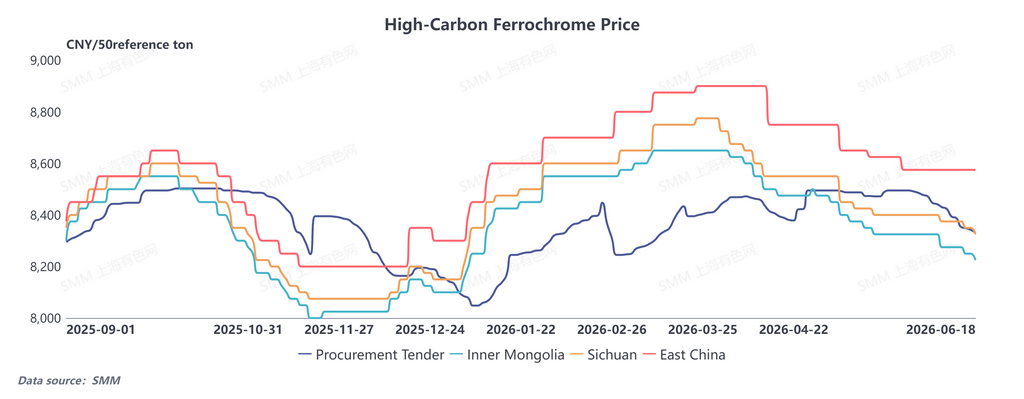

The domestic ferrochrome market trended weaker this week. As of June 18, 2026, price quotations for high-carbon ferrochrome (HC FeCr) stood as follows:

- Inner Mongolia: RMB 8,150–8,300 per 50-base ton, down RMB 50 week-on-week

- Sichuan and Northwest China: RMB 8,250–8,400 per 50-base ton, down RMB 50 week-on-week

- East China: RMB 8,500–8,600 per 50-base ton, down RMB 50 week-on-week

- Kazakh HC-FeCr: RMB 9,550–9,700 per 50-base ton, down RMB 100 week-on-week

The expected tender price index of HC FeCr for steel mills registered RMB 8,331.49 per 50-base ton. The mainstream market consensus forecasts a RMB 200 drop in steel tender prices for the coming month.

Demand Side

Macroeconomic news exerted prominent impacts: stainless steel futures surged then retreated, fluctuating within a narrow range. The market has entered the traditional off-season for consumption, dragging down downstream end-user demand and triggering expectations of production cuts among steel mills. With the Dragon Boat Festival holiday approaching, market participants adopted a wait-and-see stance. Purchasing activity for raw material ferrochrome remained sluggish with limited concluded transactions, failing to underpin ferrochrome prices.

In addition, steel tender prices stayed at relatively high levels recently. Most ferrochrome producers prioritized fulfilling long-term contractual orders, resulting in extremely thin trading in the spot retail market.

Cost Side

Falling chrome ore prices continuously pushed down spot smelting costs of ferrochrome, further eroding cost support for ferrochrome prices. Per SMM statistics:

- Production cost of ferrochrome in Inner Mongolia this week: RMB 7,842–7,897 per 50-base ton, down 0.92% week-on-week

- Lower electricity prices amid the flood season in southern China delivered more notable cost reductions. Sichuan’s ferrochrome production cost reached RMB 7,904–7,932 per 50-base ton, down 2.54% week-on-week.

Supply Side

Tight power supply in Inner Mongolia exerted limited constraints on actual ferrochrome output. With producers still securing modest profit margins, most plants maintained normal operations, keeping output at elevated levels. Overall, the ferrochrome market remains in a supply surplus, capping upside price potential. The ferrochrome market is projected to stay weak and range-bound in the short term; market players will closely monitor price guidance from the next round of steel mill tenders.

Chrome Ore

Price Review

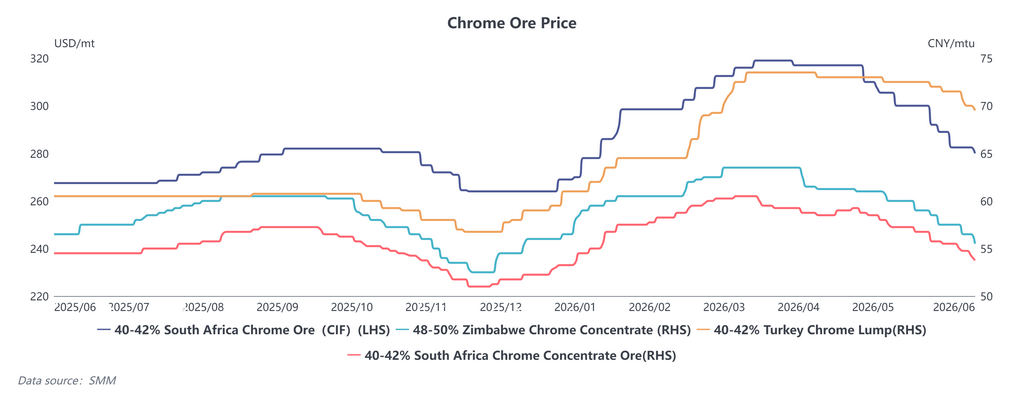

As of June 18, 2026, domestic spot quotations at Tianjin Port are listed below:

- 40–42% South African chrome fine ore: RMB 53.5–54 per unit Cr₂O₃, down RMB 1.25 week-on-week

- 48–50% Zimbabwean chrome fine ore: RMB 55–56 per unit Cr₂O₃, down RMB 2 week-on-week

- 40–42% Turkish chrome lump ore: RMB 69–70 per unit Cr₂O₃, down RMB 2 week-on-week

Overseas ore offers:

- 40–42% South African chrome fine ore: Latest offer USD 280 per ton, down USD 5 week-on-week

- 48–50% Zimbabwean chrome fine ore: USD 360–370 per ton

- 40–42% Turkish chrome lump ore: USD 315–320 per ton, flat week-on-week

Supply Side

Chrome ore port inventories stayed high. SMM data showed national chrome ore port stocks hit 4.5648 million tons this week, up 2.8% week-on-week, among which Tianjin Port held 3.7951 million tons, rising 3.24% week-on-week.

Traders faced mounting inventory liquidation pressure and were forced to cut prices to clear stocks. However, recently arrived ore cargoes carry high cost bases, exposing holders to loss risks. Ore stockholders were reluctant to offer steep discounts, leading to a stalemated market.

Demand Side

Ferrochrome smelters only purchased ore as needed without large-scale stockpiling. Buyers widely pressed down prices during inquiries, while actual concluded trades remained scarce. Pervasive bearish sentiment intensified market hesitation and slowed purchasing activity further. Price games dominated negotiations between buyers and sellers with muted trading, pointing to limited near-term improvement in chrome ore demand.

Overseas Market

Eased US-Iran tensions pulled back fuel prices and ocean freight costs that previously spiked due to Middle East geopolitical risks. Bullish drivers for overseas chrome ore prices faded, and foreign miners held bearish outlooks with steadily declining quotations.

Meanwhile, South Africa's ferrochrome resumption progressed slowly. The country's chrome ore exports will remain elevated in the short run, leaving the loose supply balance unrelieved and adding downward pressure on ore prices. The chrome ore market is expected to operate weakly and steadily in the near term.

Macroeconomic Outlook

South Africa's Industrial Development Strategy has put export taxation on chrome products on the government's agenda. Authorities also plan to establish special economic zones for deep chrome processing and negotiate formal pricing agreements. Detailed policy schemes have not yet been released, yet all market participants are closely tracking subsequent policy developments.