SMM June 16 News:

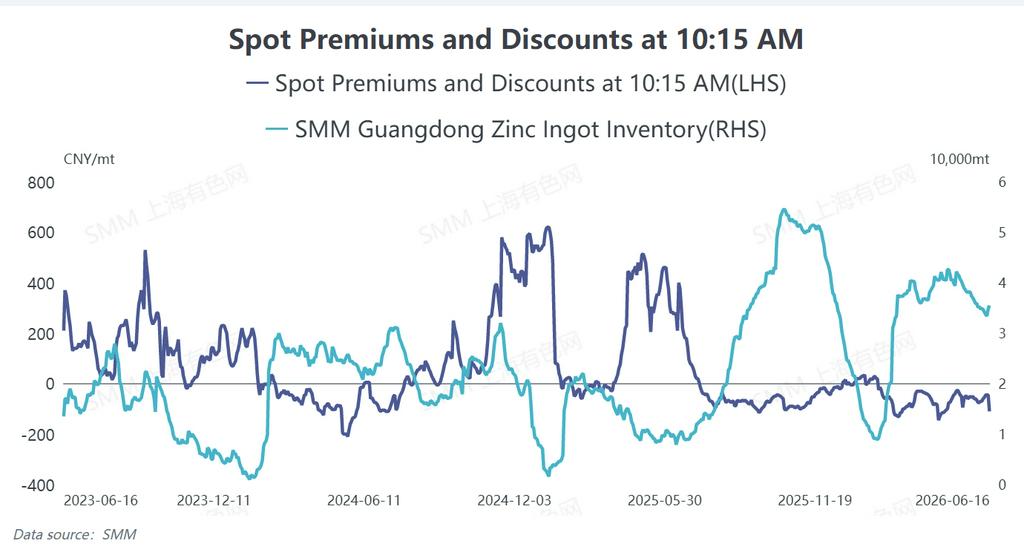

Today, the spot zinc ingot pricing in the Guangdong region has switched to the new front-month contract, with the benchmark contract shifting from the JH2607 contract to the JH2608 contract. Under the contango structure, today's quotes in the Guangdong region are at a discount of 110 yuan/ton to the JH2608 contract. How will the spot premium/discount perform in the coming period?

Looking back at the situation in May and June, the premium/discount in the Guangdong region has remained in negative territory, generally characterized by "ample supply and lackluster demand." Looking ahead, the Guangdong premium/discount is expected to remain in a state of "easier to fall than to rise."

Supply Side:

As of June 16, total inventories in the Guangdong region stood at 35,500 tonnes, with stocks building up. Looking back at the second quarter, some major spot producers in the South China region reduced output to a certain extent, leading to lower arrivals in the Guangdong region last month and a gradual decline in inventories. However, since this week, arrivals in the Guangdong region have gradually increased. Coupled with the fact that some smelters are nearing the end of their maintenance schedules, arrivals in the Guangdong region are expected to rise further, exerting strong downward pressure on the premium/discount.

Demand Side:

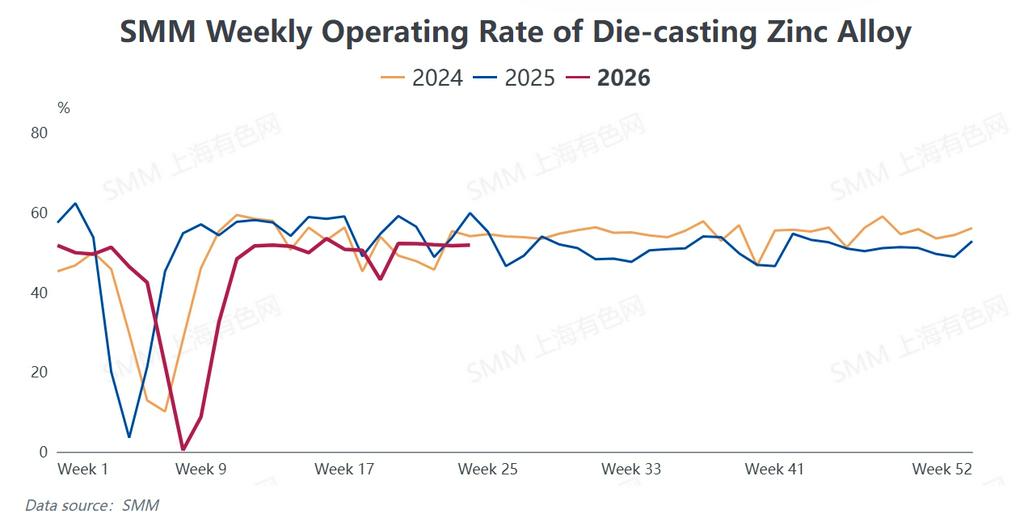

Looking at the current demand in the Guangdong region, the demand from local terminal die-casting zinc alloy enterprises is relatively moderate. The reasons include the following:

- In recent years, the domestic real estate market has weakened, resulting in insufficient domestic demand support for traditional end-use sectors of die-casting zinc alloys, such as furniture fittings, door locks, and bathroom hardware. Since Guangdong accounts for a relatively large share of such orders, it has been more significantly affected.

- The Guangdong region exports a considerable volume of terminal hardware products. According to SMM, due to the heightened tensions in the Middle East, demand for export orders from Guangdong terminals has weakened. However, orders for exports to Southeast Asia have remained generally stable.

- Additionally, the Guangdong region is home to a large number of non-standard zinc alloy producers and smelter-brand alloys. In terms of pricing, both types are offered at lower prices than the national-standard alloys produced by private enterprises. For terminal enterprises that have quality requirements, the brand reputation and pricing advantages of large smelter-brand zinc alloys make them more inclined to purchase smelter-produced alloys.

- Moreover, amid intense low-price competition in the market, an increasing number of private die-casting zinc alloy producers have turned to purchasing smelter-brand alloys in recent years to meet downstream quality standards and low-price demands. As a result, a new purchasing pattern has emerged in response to current market conditions: during downward zinc price cycles, terminal enterprises do not rigidly purchase zinc ingots; instead, they use a pricing mechanism to buy smelter-brand alloys from traders to satisfy restocking needs at lower prices, thereby further diverting direct demand for zinc ingots.

In summary, the Guangdong region is facing strong expectations of supply recovery, while the demand side remains characterized by weak domestic markets and diverging export performance. Coupled with the fact that smelter-brand zinc alloy substitute procurement further weakens direct demand for zinc ingots, the premium/discount lacks upward support in the near term. It is expected that the Guangdong premium/discount will continue to trade at a discount going forward, with significant difficulty in shifting from discount to premium.

![Rate Hike Expectations Disrupt, SHFE/LME Zinc Price Ratio Rebounds to Around 7.0 and Fluctuates [SMM Zinc SHFE/LME Price Ratio Weekly Review]](https://imgqn.smm.cn/usercenter/Txorc20251217171755.jpg)

![Off-Season Shadow Looms, Operating Rates of Galvanising Producers Continue to Weaken [SMM Galvanising Weekly Review]](https://imgqn.smm.cn/usercenter/qTzTI20251217171754.jpg)