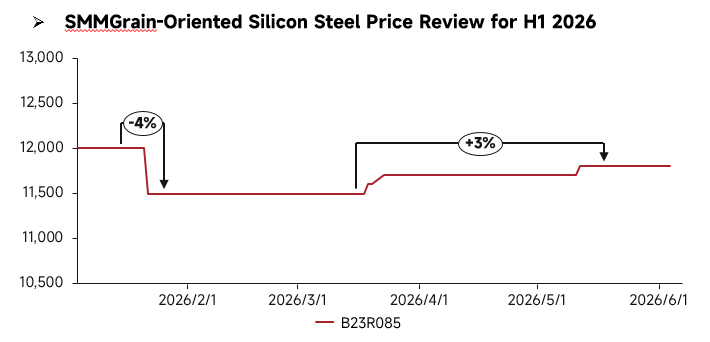

H1 Price Review:

In H1 2026, China’s grain-oriented silicon steel market fluctuated overall, with prices first suppressed and then rebounding. At the start of the year, market prices edged down, but as downstream demand gradually recovered, prices saw a rebound. Performance diverged notably by product type: competition intensified for regular grades amid mediocre demand, keeping prices generally weak; high-end high-permeability grades, supported by rigid demand from power infrastructure, remained firm throughout. On the supply side, regular grades were in ample supply and competition intensified, while high-end products, limited by technological barriers, saw constrained capacity deployment and persistently tight supply. The demand side showed pronounced structural divergence, with ongoing UHV construction and power grid upgrades sustaining solid rigid demand for high-end products, whereas demand for regular grades remained weak.

H1 Fundamentals Review:

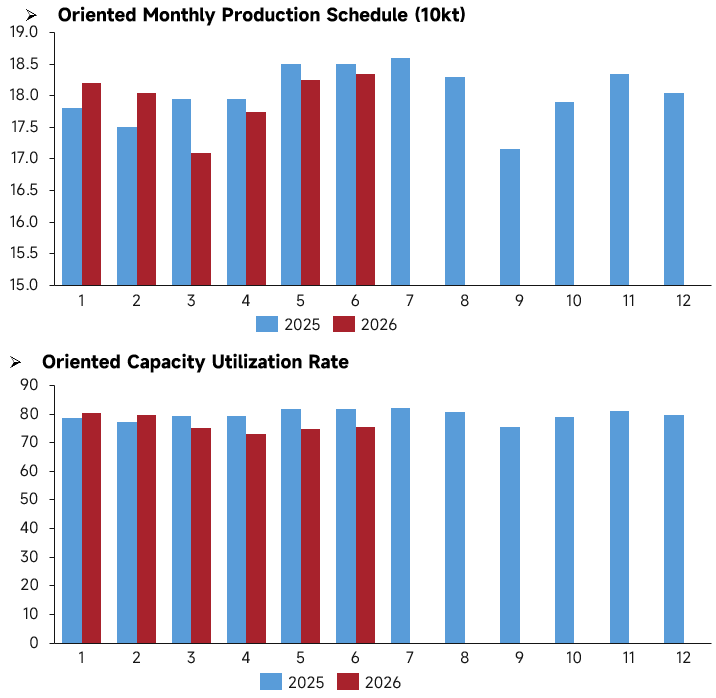

From a production perspective, the production schedule of grain-oriented silicon steel in China in H1 2026 followed a trend of rising, then falling, and then rising again. Only the January-February production schedule volume exceeded the level in the same period of 2025, while the schedule from March to June all fell short of the year-earlier level. In March, it dropped to the H1 low of about 171,000 mt, and in May-June, it recovered to around 183,000 mt as production arrangements were stepped up. However, the overall production schedule center was lower than in H1 2025, and Q2 saw a marked contraction in production activity. Over the same period, the capacity utilization rate trend was highly synchronized with the production schedule. In January-February, the utilization rate was slightly higher than last year, then declined continuously from March to April, hitting the H1 low of 74% in April, and rebounded to 76% in May-June as the schedule recovered. For each month of H1, the utilization rate was significantly lower than the same period in 2025, with the full-year range kept at 74%-81%. This diverging pattern—"slight strength at the start of the year and simultaneous weakening of production schedule and utilization rate in Q2"—indicates that downstream demand support in H1 was weaker than in 2025. Enterprises proactively lowered their Q2 production plans, and the pace of capacity commissioning slowed down. Even with moderate supplementary production in May and June, overall actual operating loads remained weaker than in the same period last year.

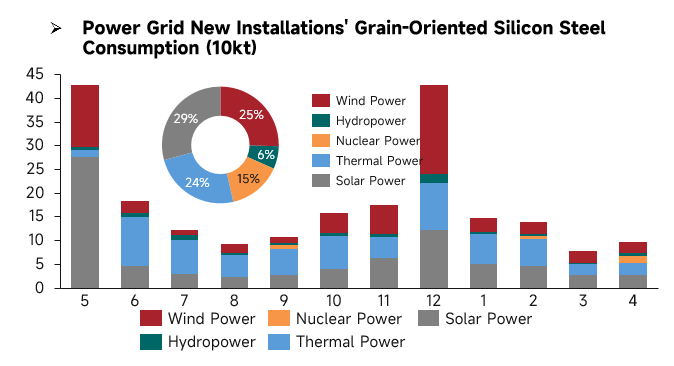

From the perspective of grain-oriented silicon steel consumption driven by power grid installations, overall demand in H1 2026 (January-April) showed a gradual weakening trend, with monthly consumption declining step by step. January marked the H1 demand peak, with total consumption of approximately 150,000 mt, supported simultaneously by PV, thermal power, and wind power. In February, total demand pulled back slightly, with consumption contracting across all sub-sectors. March fell to the H1 trough, as total monthly consumption was under 80,000 mt, and PV and thermal power installation releases slowed markedly. April saw a slight recovery in demand, but the overall volume remained low.

In terms of demand structure, solar, wind, and thermal power remained the core consumption sources in H1, together accounting for nearly 80% of consumption, with nuclear power providing a small supplement and hydropower contribution consistently low. In January, thermal power and PV provided strong boosts, while wind power, which saw concentrated year-end commissioning, had limited release in H1. PV, the largest demand segment, saw continuously declining consumption from January to April, becoming the primary factor dragging down H1 demand.

Compared with the full year, overall installation demand in H1 (January-April) was far below the two peak season highs of last May and December. The release pace of new installations was weak, with insufficient commissioning increments across all power sources. Overall, the end-use demand for grain-oriented silicon steel exhibited market characteristics of underperforming in the peak season and coming under monthly pressure.

H2 Outlook:

In H1 2026, only the Phase II 80,000 mt HIB grade grain-oriented silicon steel capacity of Angang Longdu Electromagnetic New Materials in central China came on stream in Q2, with limited new capacity additions in H1. H2 will mark a concentrated period for GO silicon steel capacity commissioning, with enterprises across multiple regions gradually starting up capacity: in east China, Baoshan Iron & Steel Co., Ltd.'s 220,000 mt HIB grade GO silicon steel capacity will simultaneously commence production in H2, Zhejiang Jinlei Soft Magnetic Materials will start up 100,000 mt CGO grade GO silicon steel capacity in Q3, and Jiangsu Zhongsheng Electromagnetic Technology (180,000 mt HIB) and Jiangxi Chongxin New Materials (80,000 mt HIB) both plan to start production in Q4; in central China, Wuhan Iron & Steel Co., Ltd. plans to launch its 200,000 mt HIB grade GO silicon steel capacity in Q3.

Looking ahead to H2, market divergence will persist. The industry’s capacity structure continues to optimize, with new capacity focusing on high-end categories. Supported by energy efficiency upgrade policies and power infrastructure projects, rigid industry demand is expected to be steadily released. Overall, ordinary grades still face downward price pressure, while high-end, high magnetic induction grain-oriented silicon steel will maintain a stable to positive trend backed by favorable demand.

![[SMM Lecong HRC Inventory] This week, Lecong inventory ended its increase and turned to a decline.](https://imgqn.smm.cn/usercenter/fvyjO20251217171715.jpg)