SMM News, June 11:

Metals market:

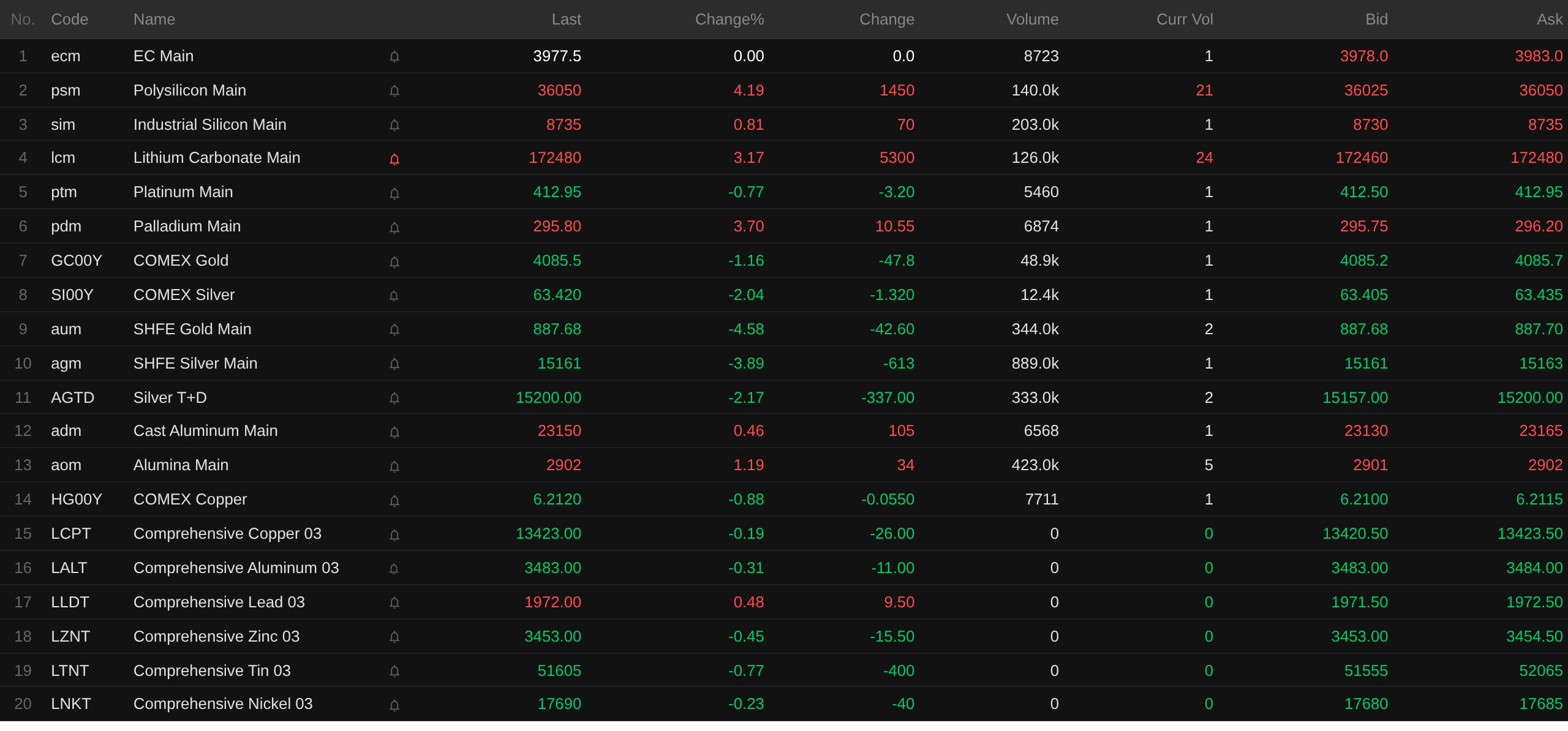

As of the midday close, base metals in the domestic market mostly fell: SHFE copper fell 1.4%, SHFE lead rose 0.68%, and SHFE tin fell 1.08%. SHFE nickel fell 1.49%. SHFE aluminum rose 0.33%. SHFE zinc fell 2.48%.

In addition, the most-traded cast aluminum futures contract rose 0.46%, and the most-traded alumina contract rose 1.19%. The most-traded lithium carbonate contract rose 3.17%. The most-traded silicon metal contract rose 0.81%. The most-traded polysilicon futures contract rose 4.19%.

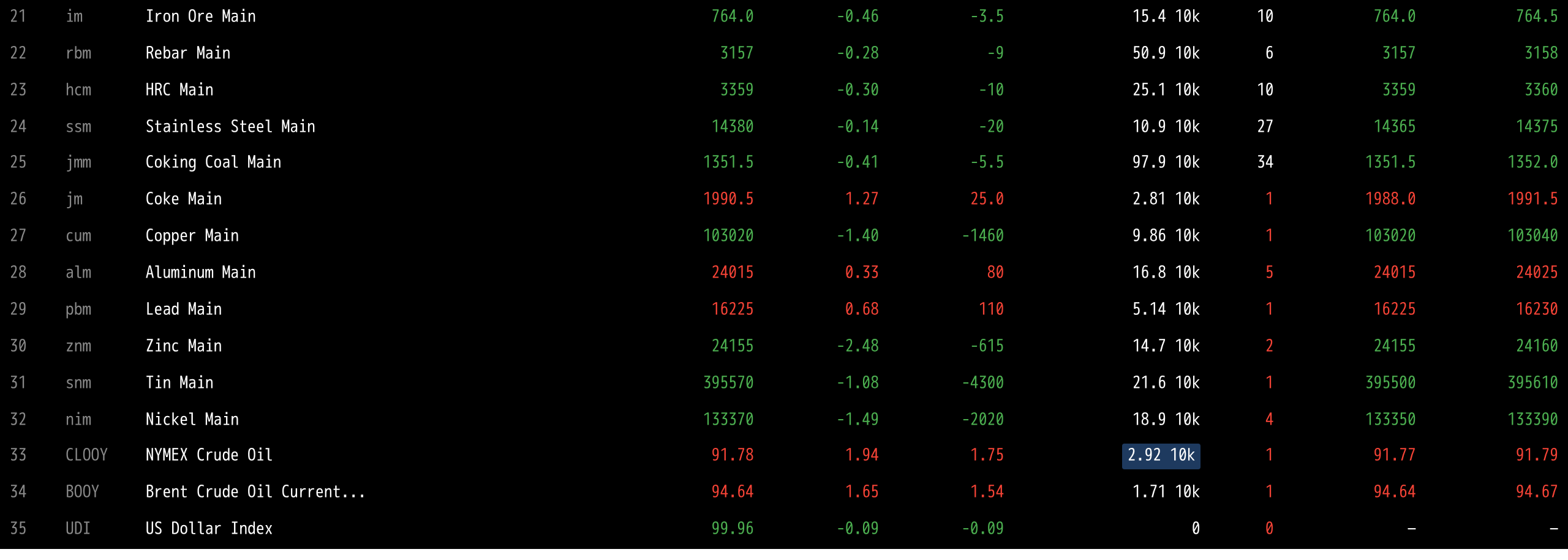

Ferrous metals mostly fell: iron ore fell 0.46%, rebar fell 0.28%, hot-rolled coil fell 0.3%, and stainless steel fell 0.14%. Coking coal and coke: the most-traded coking coal contract fell 0.41%, while the most-traded coke contract rose 1.27%.

Overseas base metals: as of 11:43, LME metals were down nearly across the board. LME copper fell 0.19%, LME aluminum fell 0.31%, and LME lead rose 0.48%. LME zinc fell 0.45%, LME tin fell 0.77%, and LME nickel fell 0.23%.

Precious metals: as of 11:43, COMEX gold fell 1.16%, hitting an intraday low of $4,046.2/oz; COMEX silver fell 2.04%. Domestic precious metals: the most-traded SHFE gold contract fell 4.58%, and the most-traded SHFE silver contract fell 3.89%.

In addition, as of the midday close, the most-traded platinum futures contract fell 0.77%, while the most-traded palladium futures contract rose 3.7%.

As of the midday close, the most-traded European container shipping contract was flat at 3,977.5 points.

As of 11:43 on June 11, midday moves in selected futures:

Spot and Fundamentals

Copper:Guangdong #1 copper cathode spot prices against the front-month contract today: high-quality copper was quoted at 240 yuan/mt, up 80 yuan/mt from the previous trading day; standard-quality copper was quoted at a premium of 180 yuan/mt, up 50 yuan/mt from the previous trading day; SX-EW copper was quoted at a premium of 120 yuan/mt, up 50 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 103,625 yuan/mt, down 585 yuan/mt from the previous trading day, while the average price of SX-EW copper was 103,550 yuan/mt, down 585 yuan/mt from the previous trading day. Spot market: Guangdong inventory continued to decline today, marking the eighth consecutive drop...

Macro Front

China:

[China Automotive Power Battery Industry Innovation Alliance: In May, China’s power and energy storage battery sales rose 47.4% YoY] The China Automotive Power Battery Industry Innovation Alliance released monthly power battery information for May 2026. In May, total production of power and energy storage batteries in China was 191.7 Gwh, up 4.2% MoM and up 55.2% YoY. In May, China's sales of power batteries and ESS batteries totaled 182.2 GWh, up 11.0% MoM and 47.4% YoY. Of these, power battery sales were 127.0 GWh, accounting for 69.7% of the total, up 16.6% MoM and 45.2% YoY; ESS battery sales were 55.2 GWh, representing 30.3% of the total, down 0.1% MoM but up 52.7% YoY.

[Changchun: Building a World-Class Vehicle Manufacturer Group, Supporting FAW and Huawei to Deepen Strategic Cooperation] The 15th Five-Year Plan for the Automobile Industry Development in Changchun (Draft for Comment) has been released for public comment. It mentions providing full support for vehicle enterprises to transform and upgrade, with the aim of building a world-class vehicle manufacturer group. It focuses on supporting vehicle enterprises to develop new energy and energy-efficient vehicles and to establish a clear brand system. It also supports carriers to strengthen strategic cooperation with domestic cross-industry enterprises in the field of intelligent connected vehicles. In particular, it fully supports China FAW in integrating global innovation resources and deepening strategic technological cooperation with Leap Motor, Huawei, DJI, and other enterprises in areas such as new energy vehicles and intelligent connected vehicles. The plan emphasizes the industrialization application and iterative upgrade of key technologies such as all-solid-state batteries, the 'Hongqi No.1' multi-domain fusion chip, the Sinan Intelligent Driving large model, and the Lingxi Cockpit large model. It supports China FAW in deepening strategic cooperation with leading technology enterprises such as Huawei, Baidu, and iFLYTEK, as well as internet platforms, to jointly establish innovation laboratories, focusing on tackling key technologies such as end-cloud integrated intelligent architecture, Level 3 and above autonomous driving, and multimodal interaction, thereby creating a nationally influential source of intelligent connected vehicle innovation. (From WSJ APP)

The PBOC conducted 188.5 billion yuan of 7-day reverse repo operations at an interest rate of 1.4%, unchanged from the previous operation. No reverse repos matured today.

As for the US dollar:

As of 11:43, the US dollar index fell 0.09% to 99.96. The US Labor Department said on Wednesday that the CPI rose 4.2% YoY in May, accelerating from 3.8% in the previous month. This marked the highest year-on-year increase since April 2023, indicating that high energy costs due to the conflict with Iran continue to drive up price pressures. Since the US and Israel launched attacks against Iran in late February, Americans have been feeling the pain of rising oil prices. Rising energy costs have weakened consumer confidence. Currently, there is little sign that oil tankers can obtain sustained permission to transit the Strait of Hormuz, meaning that supply pressure in the global energy market is expected to persist.

According to the CME FedWatch tool, the probability of the US Fed holding interest rates steady through June was 98.4%, with a cumulative 25-basis-point rate cut seen at just 1.6%. The probability of the Fed maintaining the current rate through July stood at 89.1%, a cumulative 25-bp hike at 9.5%, and a cumulative 25-bp cut at 1.5%.

Art Hogan, Chief Market Strategist at B. Riley Wealth Management, described the latest CPI report as a “tale of two cities.” While the data was highly consistent with expectations, the overall trend remained negative. This did not alter the policy path for the Fed’s next meeting. However, the prevailing consensus is that the Fed will hold steady, and Fed funds futures are currently pricing in only one hike. In summary, after significant profit-taking pressure on semiconductor stocks and the broader tech sector, these factors were likely instrumental in helping the market recover some lost ground in early trading today.

A CICC research note argued that US inflation remains dominated by structural factors, such as energy shocks, with cyclical inflation not yet evident. However, it warned of the risks of a rebound in aggregate demand driven by AI capex expansion and improving employment. On monetary policy, the firm maintained its baseline call of no cuts and no hikes by the Fed this year. It expects the Fed’s stance to stay hawkish, noting that Fed Chair Warsh’s top priority upon taking office would be to rebuild policy credibility, likely demonstrating resolve by signaling stronger expectations for balance sheet reduction rather than hinting at rate hikes. A scenario of “balance sheet reduction first, delayed rate cuts” could not be ruled out, posing sustained pressure on assets that conflict with Warsh’s philosophy, those reliant on liquidity, and those benefiting from dollar over-issuance. (Jin10 Data App)

On the Data Front:

Releases due today include the Eurozone’s ECB Deposit Facility Rate and ECB Main Refinancing Rate as of June 11, US Initial Jobless Claims for the week ending June 6, and the US PPI year-over-year and month-over-month figures for May. Additionally, attention will be on the Ministry of Commerce’s second regular press briefing for June; the ECB’s interest rate decision; and the monetary policy press conference held by ECB President Christine Lagarde.

In Crude Oil:

As of 11:43, oil prices were up across both benchmarks, with WTI gaining 1.94% and Brent crude rising 1.65%. Prices climbed amid escalating military conflict between the US and Iran.

The US Department of Energy (DOE) stated on Wednesday local time that the US is seeking to lend up to 40 million barrels of crude oil from the Strategic Petroleum Reserve (SPR) to energy enterprises to help lower fuel prices. This plan is part of a previous agreement to release 172 million barrels from the SPR. To date, the US has lent approximately 133 million barrels of crude oil under that agreement. In March this year, after the US and Israel launched a war against Iran on February 28, the US reached an agreement with about 30 member countries of the International Energy Agency (IEA) to jointly release approximately 400 million barrels of strategic reserves to help stabilize the global oil market. At that time, the US SPR inventory stood at 349.2 million barrels, the lowest level since August 2023. Enterprises that borrowed crude oil had to return an equal amount and pay a premium of up to 24% in the form of additional crude oil. (Jin10 Data APP)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

►

![[Musk Elon will speak at the ASML Virtual Technology Meeting today.]](https://imgqn.smm.cn/usercenter/wDeWQ20251217171734.jpeg)

![[Xiaomi Automobile Technology Co., Ltd. increases the product variety of extended-range electric passenger vehicles]](https://imgqn.smm.cn/usercenter/gpWpd20251217171734.jpeg)

![Market Tug-of-War Between Longs and Shorts: SHFE Zinc Posts a Bearish Candlestick [SMM Zinc Futures Brief]](https://imgqn.smm.cn/usercenter/EviJV20251217171754.jpg)