SMM June 10 News:

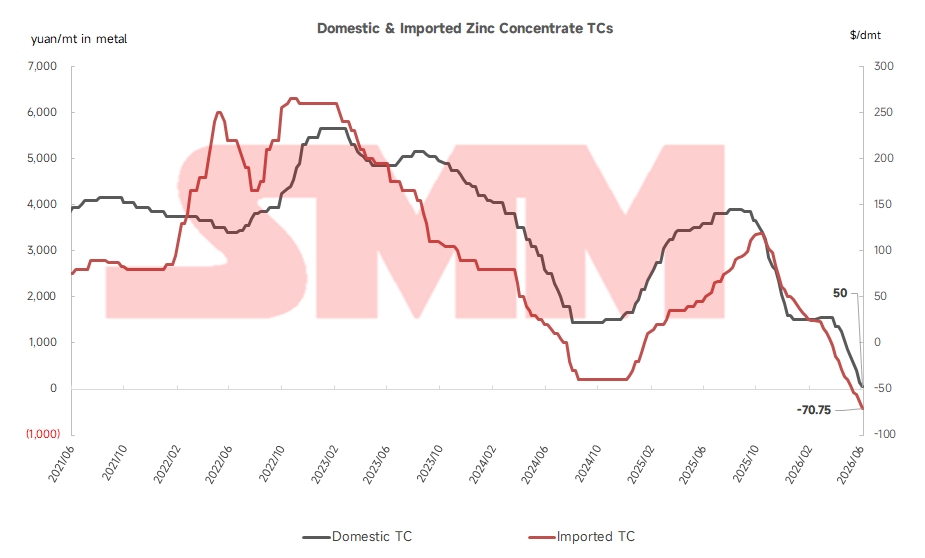

As we near the midpoint of the year, zinc concentrate treatment charges (TCs) have repeatedly tumbled to historic lows. As of June 5, the average TC for domestic zinc concentrate fell to 50 yuan per metric ton of metal content, while the TC for imported zinc concentrate dropped to -70.75 US dollars per dry metric ton. Both domestic and imported TCs continue setting new record troughs with no sign of a slowdown in the downward trend, and an increasing number of domestic concentrate transactions are now done at negative TCs. Below is an in-depth analysis of the driving factors.

Supply-side Factors

Towards the end of the second quarter, most domestic mines that suspended operations earlier have resumed full production. However, nearly all new domestic zinc mine capacity, except the Huoshaoyun project, is scheduled to come online in the second half of the year, including new mines in Gansu, Hunan, Guizhou and other provinces. Meanwhile, the Huoshaoyun mine has made limited contributions to spot market supply. In addition, output from established mines in Inner Mongolia and Yunnan has declined due to falling ore grades, resulting in subdued domestic zinc concentrate supply throughout the first half of the year.

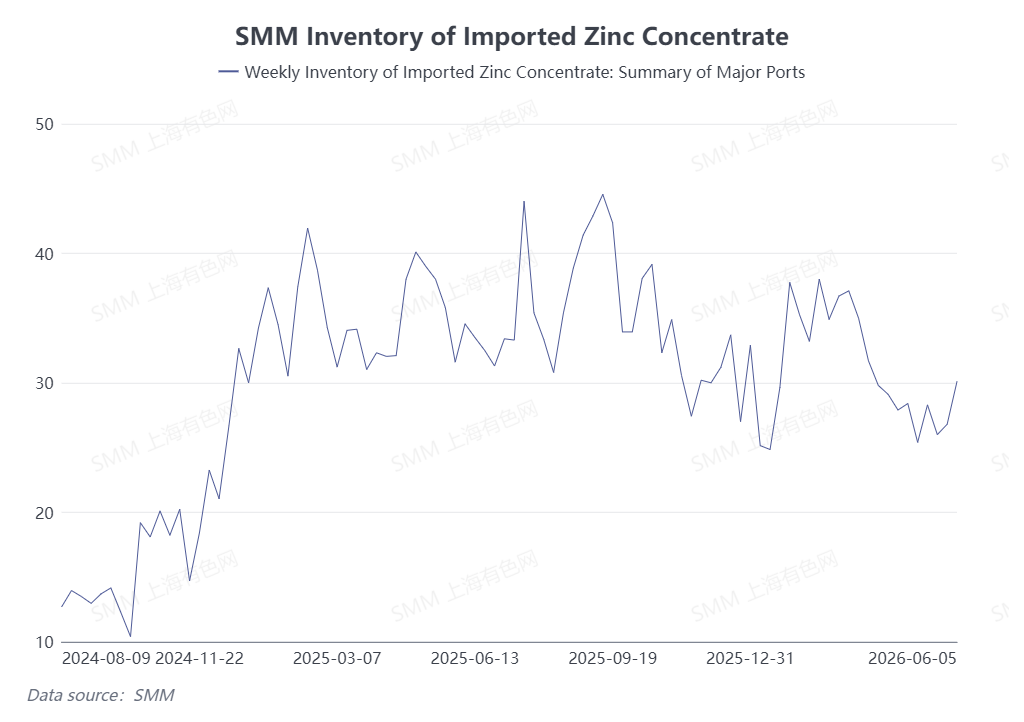

On the imported supply front, overseas zinc concentrate output faced frequent disruptions in H1 2026. Falling ore grades, unexpected earthquakes and recurrent floods in Australia in the first quarter all weighed on production. Geopolitical tensions also stoked market concerns, further tightening global zinc concentrate availability. This shortage is reflected in port inventory data: major domestic port stocks of zinc concentrate have declined from nearly 400,000 metric tons to around 300,000 metric tons since the start of Q2.

Demand-side Factors

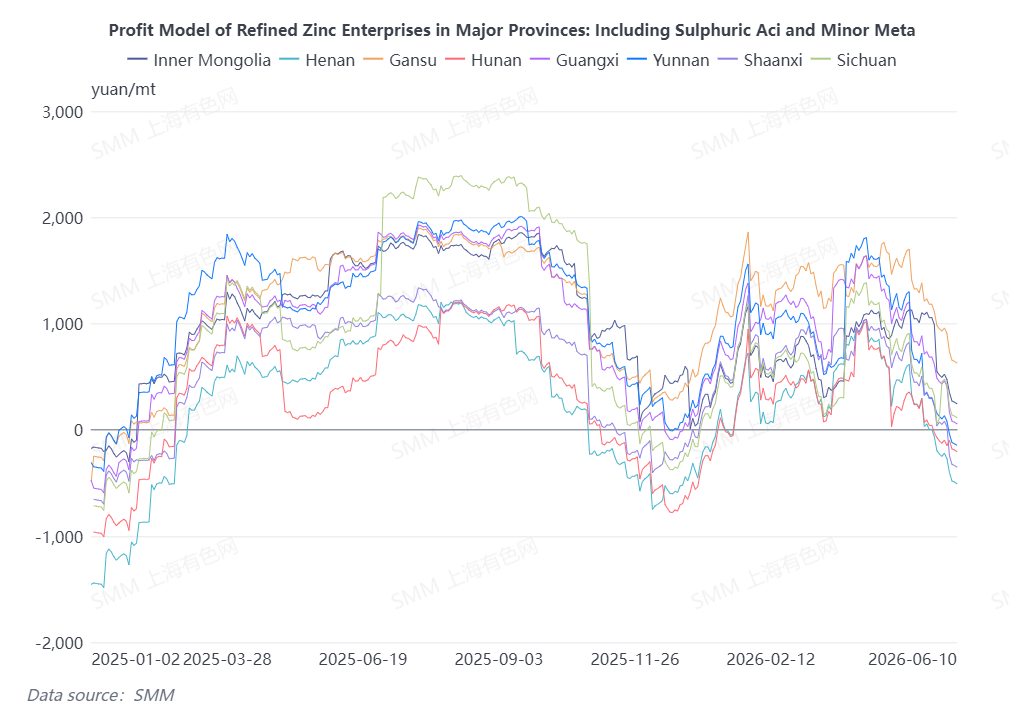

Despite the sharp plunge in domestic and imported zinc concentrate TCs, sulfuric acid prices have risen markedly from Q1, currently ranging between 1,400 and 1,800 yuan per metric ton across China. Taking by-products such as copper, silver and gold into account, data from SMM shows domestic major smelters remained profitable on an integrated basis in May. Although smelters’ profit margins have continued to narrow in June, producers in some regions still maintain decent earnings. As a result, production cuts among domestic smelters have been minimal from May to June, keeping firm demand for zinc concentrate.

Arbitrage & Price Parity Dynamics

The import arbitrage window for zinc concentrate has remained closed throughout Q2. Between April and early June, importing zinc concentrate resulted in losses of 1,500 to 2,000 yuan per metric ton of metal content. Driven by unfavorable import economics, domestic smelters ramped up purchases of local zinc concentrate, which further dragged down domestic TCs rapidly.

Market Outlook

Looking ahead, sustained margin compression will prompt some domestic smelters to launch production cuts and maintenance work. The third quarter is also the traditional maintenance season for domestic zinc smelters, which may ease the tight supply-demand balance of zinc concentrate to a certain extent. Nevertheless, the fourth quarter usually marks the seasonal stockpiling period for winter supplies. Against this backdrop, zinc concentrate TCs are unlikely to stage a notable recovery for the rest of the year.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)

![Affected by LME, SHFE zinc recorded a bearish candlestick [SMM zinc morning comment]](https://imgqn.smm.cn/usercenter/nlmjY20251217171755.jpg)

![Geopolitical Risks in Middle East Persist, LME Zinc Center Shifts Downward [SMM Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/TeRBO20251217171754.jpg)

![Slight destocking of zinc ingot in China, but price rise faces certain obstacles [SMM Zinc Futures Brief Comment]](https://imgqn.smm.cn/usercenter/PEqzX20251217171755.jpg)