After both sodium-ion battery cathodes and hard carbon anodes recorded significant increases YoY and MoM in May, the midstream and downstream segments of the industry chain—electrolytes and battery cells—also delivered impressive results, yet structural issues lurk beneath the growth. Electrolyte enterprises, facing uncertainty in sodium-ion battery demand, are hesitating in expansion decisions, with a prominent shortfall in raw material supply. While battery cell production keeps ramping up, application scenarios remain concentrated in narrow markets such as two-wheelers and behind-the-meter (BTM) energy storage, and volume uptake in utility-scale energy storage will still take time. It is noteworthy that the undersupply at the cathode end and full capacity utilization at the anode end have created upward pressure, while the lagging pace of electrolytes and battery cells means a discrepancy remains in the coordinated volume ramp-up across the entire industry chain.

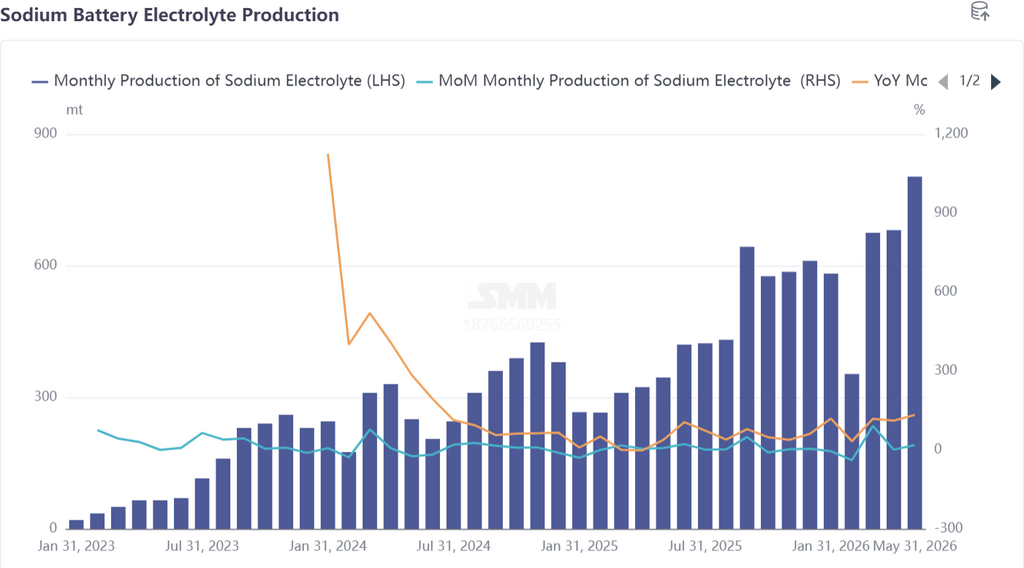

Electrolyte: High Production Growth but Insufficient Confidence; Raw Material Supply Is the Biggest Constraint on Expansion

In May, sodium-ion battery electrolyte production surged 18% MoM and 133% YoY, growth rates closely matching those of cathodes (up 17% MoM) and anodes (up 26% MoM), indicating that the ramp-up of front-end materials has effectively boosted electrolyte shipments. However, beneath the surface prosperity, electrolyte enterprises’ expansion sentiment is not buoyant.

In terms of capacity, there is no rigid bottleneck for sodium-ion battery electrolyte itself—it can be flexibly allocated using the surplus capacity of lithium battery electrolytes—but this “shared capacity” model precisely exposes enterprises’ cautiousness. Given the still substantial uncertainty in sodium-ion battery cell demand, electrolyte enterprises are hesitant about independently expanding sodium-ion battery electrolyte capacity

: lithium battery electrolyte already provides stable orders and considerable profits; shifting to sodium-ion batteries would require rebuilding matching relationships in two dimensions—upstream raw material supply stability and downstream sustained orders from battery cell manufacturers—making the risk-return ratio unappealing.

A more critical constraint lies in upstream raw materials. The capacity for core raw materials of sodium-ion battery electrolytes, such as NaPF6, NaFSI, and NaODFB, is extremely limited; only one or two enterprises in China may possess relevant supply capabilities, and their production lines are mostly at pilot or laboratory scale, far from mass production levels. This mirrors the continuous price increases of NFPP raw materials for cathodes (iron phosphate, sodium dihydrogen phosphate, etc.)—raw material supply is tightening across the entire industry chain.

Even if electrolyte enterprises have no shortage of transferable capacity, the availability of raw materials is the real shortfall. How to rationally arrange the supply pace of sodium-ion battery electrolyte amid the trend of growing capacity is a pressing question for them to address.

Looking into June, as the sodium-ion battery market continues to gain momentum—cathode production schedules are expected to rise 1% MoM and hard carbon anode schedules 9% MoM—electrolyte enterprises are likely to pay greater attention to the sodium-ion battery segment. June sodium-ion battery electrolyte production is expected to increase 17% MoM and surge 125% YoY, keeping pace with upstream materials growth.

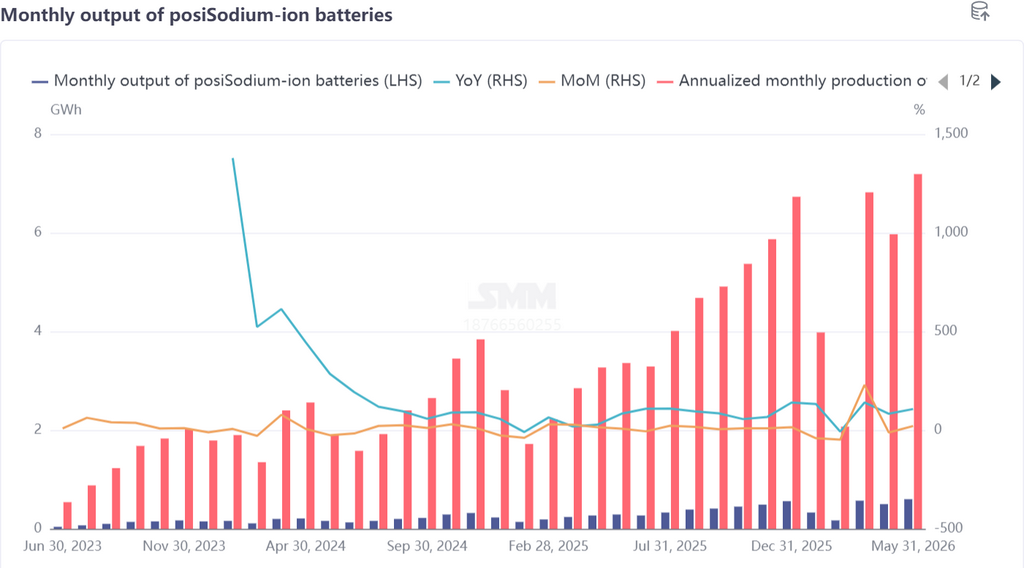

Battery cells and end-use markets: Production keeps rising; expanding application scenarios is increasingly urgent

In May, sodium-ion battery cell production rose 21% MoM and 107% YoY, the fastest growth across all industry chain segments. End-use demand structure, two-wheelers, small-scale ESS, and household ESS remain the primary application scenarios, while the large-scale volume rollout of utility-scale energy storage projects is expected to start in H2.

Product matrix, battery cell manufacturers' new product pipelines already point to a clear strategic direction: R&D focus is centered on medium- and large-capacity prismatic cells, with continuous breakthroughs in energy density and capacity, targeting utility-scale energy storage applications. This trend aligns with the rising share of NFPP in cathode materials (reaching ~87% in May) and the firm premium for high-quality hard carbon anode products—upstream and downstream are jointly building momentum for sodium-ion batteries to enter the utility-scale storage race.

The export side also shows highlights. Sodium-ion battery energy storage export orders increased, with markets outside China such as Europe showing growth potential for sodium-ion household ESS demand. Compared with the high price sensitivity of end-users in China, markets outside China are more receptive to sodium-ion battery storage, which carries higher costs but offers superior low-temperature performance—providing a differentiated competitive channel for sodium-ion battery cells.

In the Chinese market, however, the narrow range of application scenarios remains the core risk for battery cell enterprises. A business structure reliant on a few scenarios or a limited number of clients is unsustainable, and battery cell manufacturers are proactively accelerating the expansion of application scenarios and customer groups. This proactive stance reflects the collective mindset across the industry chain:

rather than passively waiting for downstream volume to materialize, it is better to actively define application scenarios. After all, cathode and anode material capacity expansion is already imminent (a significant release of cathode and anode capacity is expected in Q3). If end-use absorption capacity fails to expand in tandem, the supply-demand mismatch will spread from the midstream to the entire chain. Looking ahead to June, there is still room for growth in sodium-ion battery cell orders, with production expected to increase 20% MoM and 162% YoY, maintaining a strong expansion pace.

Summary

Looking at the entire sodium-ion battery industry chain in May, production across all four segments—cathode, anode, electrolyte, and battery cell—grew both YoY and MoM,

confirming that the industrialisation of sodium-ion batteries has entered a substantive volume ramp-up. However, the pace of operations was uneven, showing a gradient of confidence: "tight front-end, hesitant mid-end, and pioneering back-end":

Front-end (cathode/anode): capacity remained tight, with top-tier players in undersupply; raw material cost upward pressures accumulated, and capacity expansion expectations for Q3 are clear. For hard carbon anodes, a spillover effect has already emerged, with manufacturers turning to toll processing to fill supply gaps, reflecting the tightness in front-end supply.

Mid-end (electrolyte): Production grew rapidly, but confidence in capacity expansion remained insufficient. The core bottleneck was not in capacity allocation, but in the supply constraints of key raw materials such as NaPF6.

Hesitation in expanding electrolyte capacity could become a potential bottleneck for the scale-up of the entire industry chain—if upstream raw materials cannot break through mass production bottlenecks, the electrolyte could turn into an invisible ceiling constraining large-scale shipments of sodium-ion battery cells.

Back-end (battery cells): Output growth outpaced the rest of the supply chain, but application scenarios were still being explored. The two-wheeler and behind-the-meter (BTM) energy storage markets were not enough to absorb the front-end capacity about to be released. The breadth and depth of downstream application scenarios will determine whether the sodium-ion battery industry chain can achieve a genuine volume-price resonance in H2.Looking ahead to June and Q3, as cathode and hard carbon anode capacity comes online successively, new battery cell application scenarios accelerate their market introduction, and demand from outside China for residential energy storage continues to flow in, the sodium-ion battery industry chain is expected to shift from front-end-driven growth to full-chain synergy. Whether the electrolyte segment can leverage this momentum to break through raw material supply bottlenecks, and whether the battery cell segment can open up utility-scale energy storage scenarios, will be the key observation windows determining the industry's trajectory for H2.

![[CATL's Wu Kai: Sodium-ion mass production this year, lithium-air next]](https://imgqn.smm.cn/usercenter/MaxcL20251217171730.jpg)

![[Sodium Battery: Fujian Nate Energy Sodium Battery Project Receives Environmental Assessment Acceptance]](https://imgqn.smm.cn/usercenter/tKgKv20251217171725.png)