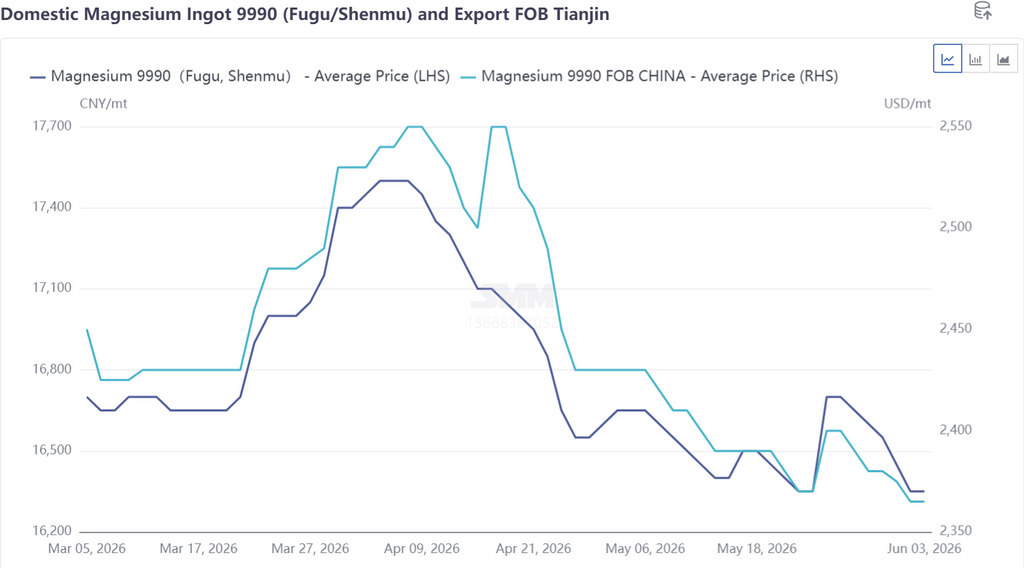

In May 2026, magnesium prices moved sideways within a price range of 16,300-16,700 yuan/mt, with the monthly average price at 16,516 yuan/mt, down 3.21% MoM. The magnitude of price changes continued to narrow in May, with the market caught in a dilemma between rises and falls, and the trend was jointly driven by two core factors: supply-demand fundamentals and cost support. Supply and demand maintained a dynamic equilibrium. Benefiting from improved semi coke production and sales, primary magnesium smelters saw marginal relief in capital pressure, and producers' willingness to sell at low prices to recover raw material funds weakened, underpinning spot quotes. Inventory structure divergence became prominent: during the price rise phase, leading smelters successfully destocked, while small and mid-sized trailing enterprises saw passive inventory accumulation; during the pullback phase, mid-sized plants shipped by offering price cuts to secure orders, while large plants flexibly adjusted quotes in line with futures, and the ebb and flow of inventory maintained market supply-demand balance. Cost side, effective bottom support was formed as spot prices approached the smelting cost line, limiting market pessimism and further compressing downside room for magnesium ingots, ultimately constraining sharp declines and resulting in the month-long sideways movement.

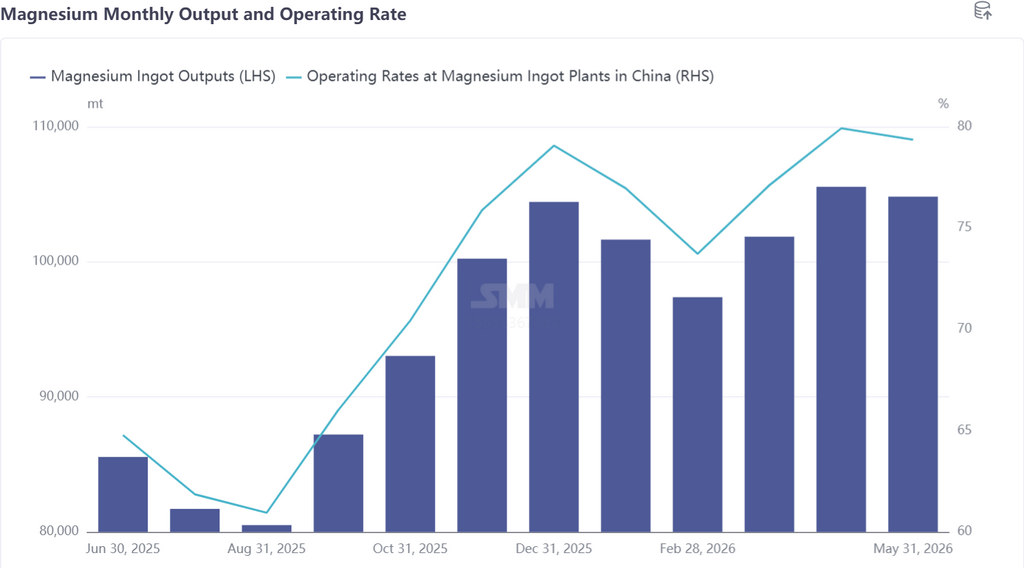

In May 2026, primary magnesium production fell 0.69% MoM. Production across regions diverged in May, with concentrated maintenance at some smelters in major producing areas dragging down total production, while enterprises in Xinjiang and Anhui increased output, narrowing the production decline to some extent. Specifically, most primary magnesium smelters maintained stable production in April. A smelter in Shaanxi shut down for maintenance at the beginning of May, while another Shaanxi enterprise slightly raised daily output. A Shanxi enterprise conducted routine maintenance at month-end, reducing output by approximately 100 mt, while another Shanxi producer slightly increased production. One enterprise each in Heilongjiang, Anhui, and Xinjiang slightly increased production, while another smelter in Xinjiang halted production for the entire month. Overall, market output reductions exceeded increases, and total primary magnesium production in May pulled back slightly.

Looking ahead to June, magnesium prices are expected to maintain a weak balance supported by production costs. Historically, export demand in June tends to pull back, which may break the current price balance and add downward pressure on magnesium prices. Weighed down by market conditions, some smelters plan to arrange maintenance at the end of June; however, new capacity continues to come on stream, and combined with production resumptions from facilities under maintenance in May, magnesium ingot production in June is expected to be basically flat MoM.

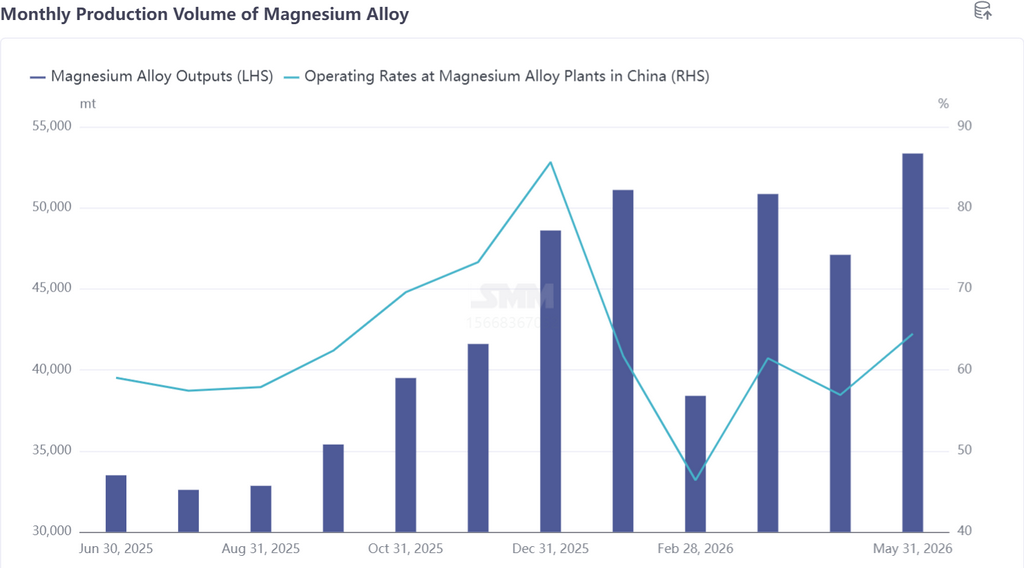

In May 2026, China's magnesium alloy production rose 13.27% MoM, as multiple magnesium alloy producers successively ramped up production during the month, driving rapid output growth. By producing region, Anhui, Shaanxi, and Shanxi led in production gains, with a primary magnesium producer in Shaanxi successfully commissioning a new magnesium alloy production line. Looking ahead to June, automotive magnesium alloy orders are steadily improving, while two-wheeler orders remain sluggish. Overall downstream demand is rising steadily, supporting continued growth in magnesium alloy production.

In June, the strong-supply-weak-demand pattern in the magnesium market is unlikely to improve. In the first ten days, magnesium prices temporarily continued the fluctuating and stagnant pattern of May. Dragged down by weakening foreign trade, the price floor gradually shifted lower, and the market overall fell into a fluctuating downward trend. Entering late June, magnesium prices continued to decline, steadily compressing smelters' profit margins. Industry production profits gradually approached the breakeven line, and production and operational pressure at most smelters climbed significantly. Against this backdrop, maintenance

expectations continued to heat up, and plans for production shutdowns to avoid risks and output cuts to support prices are likely to materialize in a concentrated manner. Supply side, rising expectations of supply contraction can effectively alleviate the current market pressure of strong supply and weak demand, forming a phased bottom support for the persistently weakening magnesium prices and limiting the downside room for further decline. In the long term, the ongoing R&D and commercialization of various magnesium alloys continue to tap downstream demand potential. The industry will enter a phase of simultaneous expansion in both supply and demand, and the current oversupply pattern may be reversed in the future.